TL;DR:

- Most SME owners underestimate currency risk, which can quietly erode margins through unhedged forex exposure. Implementing consistent, low-cost hedging strategies like forward contracts and natural hedging improves financial stability and reduces earnings volatility. Modern technology and automated platforms now make effective forex risk management accessible and practical for small businesses.

Most SME owners believe currency risk is someone else's problem. It isn't. Every cross-border invoice, every import order, every international supplier contract carries hidden forex exposure that can quietly drain margins before you even notice. Hedged firms show notably higher ROA (β=0.342) and lower earnings volatility compared to unhedged peers. The good news is that protecting your profits doesn't require a treasury department. It requires the right knowledge and the right tools.

Table of Contents

- What is forex risk and why SMEs are vulnerable

- Common forex risk management strategies for SMEs

- Technology and automation: leveling the playing field

- Implementing a practical forex risk management plan

- The uncomfortable truth most SMEs miss about forex risk

- How CorpHedge empowers SMEs to manage forex risk

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| SMEs are exposed | Small and midsize businesses face real profit risks from currency fluctuations. |

| Hedging boosts results | Evidence shows SMEs using hedging achieve higher profits and less volatility. |

| Accessible tools now exist | Fintech and automation make affordable forex risk management possible for all SMEs. |

| Proactive planning is vital | Implementing a step-by-step strategy is key to protecting profits against currency swings. |

What is forex risk and why SMEs are vulnerable

Building on the introduction, let's clarify what forex risk really means for smaller businesses.

Forex risk, also called currency risk or exchange rate risk, is the potential for losses when the value of one currency changes relative to another. For an SME that buys inventory from a European supplier in euros but sells in U.S. dollars, a strengthening euro means the same invoice suddenly costs more. That gap goes straight to your bottom line. Understanding forex risk basics is the first step toward protecting your business.

There are three core types of forex risk that SMEs face regularly:

- Transaction risk: Losses on specific contracts or invoices when exchange rates move between the agreement date and the payment date.

- Translation risk: The impact on financial statements when foreign currency assets or revenues are converted back to your home currency.

- Economic risk: Long-term effects on competitiveness and cash flow when sustained currency shifts make your products more or less price-competitive in foreign markets.

Most SMEs underestimate their exposure because they think in nominal terms. They see a signed contract for $500,000 and assume that's what they'll receive. What they don't account for is that a 5% adverse currency move can quietly erase $25,000 in profit with no warning.

Statistic: Smaller businesses are more vulnerable to currency swings than large firms, yet among Australian corporates studied, importers hedge 80% of their exposure and exporters hedge 86%, demonstrating that proactive hedging is already standard practice for those who understand the stakes.

Large enterprises have dedicated treasury teams, sophisticated risk systems, and natural scale advantages. They can absorb temporary currency shocks. An SME with tighter margins and fewer cash reserves cannot. That's precisely why strategic risk management matters more, not less, for smaller businesses operating internationally.

Common forex risk management strategies for SMEs

Once the risks are clear, SMEs must evaluate practical management solutions. The good news is that several well-tested strategies are available at costs that fit an SME budget.

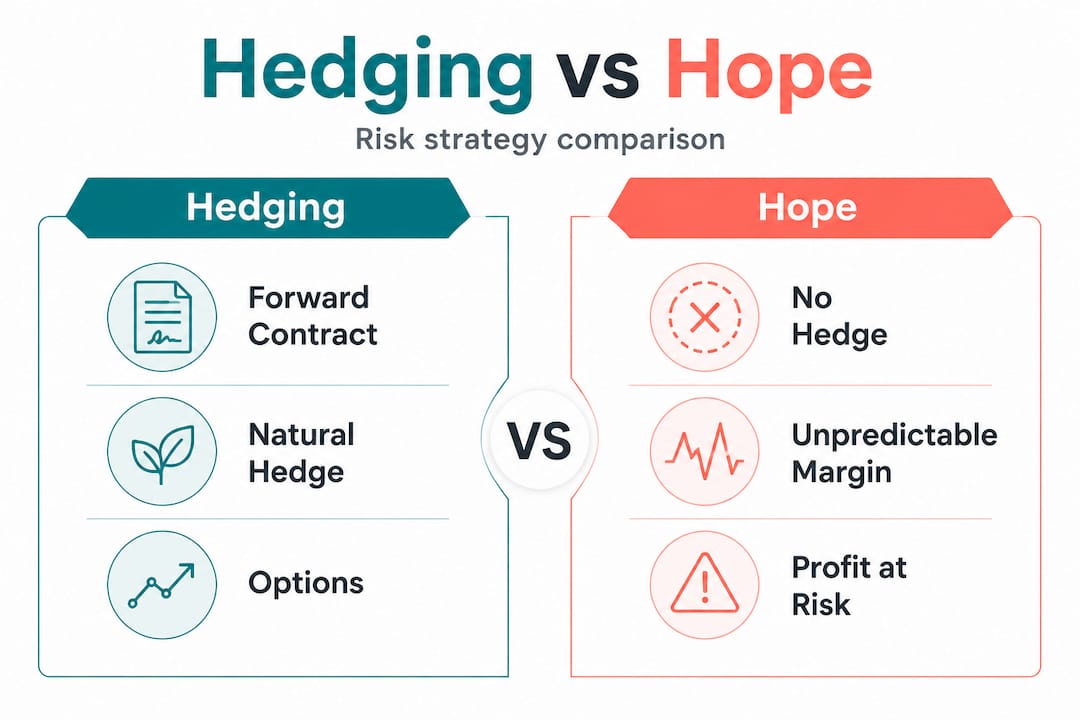

The main hedging instruments

Here is a direct comparison of the three most commonly used strategies:

| Strategy | How it works | Cost | Accessibility for SMEs | Effectiveness |

|---|---|---|---|---|

| Forward contracts | Lock in a future exchange rate today | Low (spread only) | High | High for known cash flows |

| Currency options | Right but not obligation to exchange at a set rate | Premium required | Medium | High, with upside flexibility |

| Natural hedging | Match revenues and costs in the same currency | No direct cost | High | Moderate, depends on business model |

| Money market hedges | Borrow or deposit in foreign currency to offset risk | Interest cost | Medium | High for large transactions |

Forward contracts remain the most widely adopted tool. 72% of firms use forward contracts as their primary hedging instrument in emerging market studies, and the data confirms the outcome: hedgers consistently show superior return on assets and reduced earnings volatility compared to unhedged businesses.

Natural hedging is worth highlighting because it costs nothing to implement. If your business generates revenue in euros and also pays suppliers in euros, those two flows partially cancel each other out. A manufacturing SME that sources components from Germany and sells finished goods to France is naturally hedged on a portion of its exposure. The limitation is that perfect natural hedges are rare, and any residual gap still needs to be covered with financial instruments.

Currency options offer the most flexibility. You pay a premium upfront, but if the exchange rate moves in your favor, you can let the option expire and benefit from the better rate. For SMEs with uncertain cash flows, say a business that bids on export contracts without knowing which ones will close, options are often the smarter choice over forward contracts.

How to choose the right strategy

Follow this four-step process to select the approach that fits your business:

- Quantify your exposure. List every currency pair your business touches, the amounts involved, and the timing of expected cash flows. This tells you how much you actually need to hedge.

- Assess your cash flow certainty. If you know exactly when and how much you'll receive or pay, forward contracts are efficient and affordable. If cash flows are variable or uncertain, options give you more flexibility.

- Set a hedging ratio. You don't need to hedge 100% of exposure. Many SMEs hedge 60% to 80% and leave a portion open, which reduces cost while still protecting core margins. Explore advanced forex risk strategies for guidance on setting ratios.

- Review and adjust quarterly. Market conditions change. Your hedging program should be reviewed regularly to stay aligned with your actual exposure and business objectives. Using risk mitigation frameworks helps standardize this review process.

Pro Tip: Never hedge based on hope. Your hedge ratio should reflect your actual gross margin. If a 4% currency move would wipe out your entire margin on a contract, you need near-complete coverage on that position regardless of what you expect rates to do.

Technology and automation: leveling the playing field

With strategy options in mind, innovative technologies are expanding accessibility for SME risk management.

For years, the biggest obstacle for SMEs wasn't knowledge. It was access. Sophisticated hedging tools, real-time rate monitoring, and Value at Risk (VaR) modeling were locked behind enterprise pricing and complex systems that required specialist staff to operate. That barrier is now collapsing rapidly.

Research confirms the challenge but also points to the solution: SMEs lag large firms in tool access and capabilities, but technology and AI are actively emerging to fill that gap through forecasting automation and accessible platforms.

Here's how modern technology is changing the equation for SMEs:

- Automated rate alerts: Platforms now let you set rate thresholds and receive instant notifications when your target rate is reached, so you execute at the right moment without watching screens all day.

- AI-driven forecasting: Machine learning models process macroeconomic data, central bank announcements, and historical volatility patterns to generate currency forecasts that would have required a full analyst team five years ago.

- Real-time exposure tracking: Cloud-based dashboards aggregate all your open positions, upcoming payments, and current hedge coverage in one place, giving you a live view of your net exposure.

- Integrated execution: Modern platforms connect directly with banking and payment infrastructure, so you can execute a forward contract or currency option without leaving the system.

Here is a snapshot of how technology features compare across SME needs:

| Business need | Manual approach | Technology-enabled approach |

|---|---|---|

| Rate monitoring | Check rates daily on banking portal | Automated alerts at target rate |

| Exposure calculation | Spreadsheet updated weekly | Real-time dashboard with live data |

| Strategy execution | Call relationship manager | Click-to-execute through platform |

| Reporting | Manual export and formatting | Automated reports for finance team |

| Risk modeling | Hire specialist or consultant | Built-in VaR and scenario analysis |

Pro Tip: When evaluating any risk management platform, check whether it integrates with your existing accounting or ERP system. Platforms that pull invoice data automatically save hours of manual input every week and dramatically reduce the risk of hedging the wrong amount. Start by reviewing risk management tools to understand what a good integration looks like.

The shift toward smart forex risk management tools means that a finance manager at a 50-person manufacturing company now has access to the same quality of analytics that a multinational treasury team uses. The cost difference is dramatic, and the learning curve is far shorter.

Implementing a practical forex risk management plan

Technology and tools alone aren't enough. SMEs need a step-by-step plan to turn strategy into consistent, repeatable execution.

Here is a practical six-step framework that any SME can implement regardless of size or complexity:

-

Map your currency exposures. Identify every transaction, contract, or recurring flow involving a foreign currency. Include accounts payable, accounts receivable, intercompany transfers, and any foreign currency debt. Document the currency pair, the amount, and the expected payment date.

-

Prioritize by impact. Not all exposures are equal. Focus your hedging resources on positions large enough to materially affect your margin. A $2,000 purchase in a foreign currency probably doesn't justify a forward contract. A $200,000 quarterly supplier payment absolutely does.

-

Set your hedging policy. Write a one-page policy that specifies your target hedge ratio, the instruments you're authorized to use, who has approval authority, and how frequently you review your positions. This document removes emotion from hedging decisions and keeps your program consistent. Enterprise currency risk management frameworks can guide your policy structure.

-

Execute your initial hedges. Use the tools and instruments you selected to hedge your priority exposures. Start simple. A forward contract on your three largest upcoming foreign currency payments is a meaningful, low-complexity starting point.

-

Monitor positions and market conditions. Review your open hedges monthly at minimum. Compare your hedged rates to market rates to assess effectiveness. Adjust your coverage if your business volumes or timing expectations change significantly.

-

Iterate based on outcomes. After each hedging period, measure what the hedge saved or cost relative to the open market rate. Use this data to refine your approach. Financial risk reduction strategies and proven steps for currency risk can help you benchmark your program against industry practice.

A critical lesson from businesses that struggle with forex management is inconsistency. They hedge aggressively when rates move against them and then abandon the program when rates stabilize. This behavior creates a false sense of security and typically results in losses during the next adverse move.

"The businesses that benefit most from hedging are not the ones that hedge when they're scared. They're the ones that hedge consistently, regardless of their short-term market view."

Importers hedge 80% of exposure and exporters 86% according to CommBank research among Australian corporates. That consistency is the key takeaway, not the percentage itself. Build the habit before you build the complexity.

Key success factors from SMEs with effective programs include:

- Assigning one person as the owner of the forex risk policy

- Connecting hedging activity directly to the monthly close process

- Using automated platforms to reduce manual workload and errors

- Reviewing the policy annually as the business grows and exposures evolve

The uncomfortable truth most SMEs miss about forex risk

Most conversations about forex risk focus on mechanics, which instruments to use, how to price a forward, what a VaR model outputs. But the real reason most SMEs remain dangerously unhedged has nothing to do with complexity or cost. It comes down to a belief that hedging is something you do when you're big enough to justify it.

That belief is expensive. Unhedged SMEs suffer measurable performance deterioration, including lower return on assets and higher earnings volatility, compared to peers who hedge even modestly. This isn't theoretical. It shows up in financial statements, in cash flow shortfalls, and ultimately in the ability to invest and grow.

The second misconception is that hedging is expensive. For most SMEs, a basic forward contract program covering your top three or four currency exposures costs almost nothing beyond the bid-ask spread embedded in the contract rate. The cost of not hedging, which shows up as margin erosion in the wrong quarter, is almost always higher.

What actually changes results for SMEs isn't accessing sophisticated instruments. It's consistency and discipline. A business that follows currency fluctuation best practices with a simple, well-maintained forward contract program will outperform a business that occasionally buys complex options but has no underlying policy or process.

The platforms available today eliminate the last genuine barrier, which was operational complexity. Real-time dashboards, automated alerts, one-click execution, and built-in reporting mean that an SME finance manager can run a professional-grade hedging program in a fraction of the time it once required. The question is no longer whether you can afford to hedge. It's whether you can afford not to.

How CorpHedge empowers SMEs to manage forex risk

The gap between knowing you need forex risk management and actually having a working program is where most SMEs get stuck. CorpHedge was built specifically to close that gap, giving SME finance teams the tools to assess, execute, and monitor currency hedging without needing a full treasury department.

CorpHedge offers real-time visibility into your FX positions, Value at Risk-based hedging to size your hedges accurately, and seamless integrations that reduce manual workload. Whether you're just starting to map your exposure or looking to automate an existing program, the full platform features are designed around what SMEs actually need: clarity, speed, and lower costs. Take a closer look at all available risk management solutions to see how they apply to your specific business model.

Pro Tip: Start your CorpHedge onboarding by importing your last 90 days of foreign currency transactions. This gives the platform a real baseline to model your exposure and recommend an appropriate hedging ratio from day one.

Frequently asked questions

What is the main currency risk facing SMEs?

SMEs are exposed to exchange rate fluctuations that can unexpectedly reduce profits from international sales or purchases, with smaller businesses particularly vulnerable because they have fewer financial reserves to absorb sudden rate moves.

Can small businesses implement forex hedging strategies affordably?

Yes, newer fintech solutions and automated platforms now offer affordable, accessible hedging tools for SMEs, closing the gap that once left SMEs behind larger firms in access to risk management technology.

How do forward contracts help SMEs protect profits?

Forward contracts lock in an exchange rate in advance, and firms that use them consistently show higher return on assets (β=0.342) and significantly reduced earnings volatility compared to unhedged peers.

Are there policy incentives for SMEs to access hedging tools?

Some jurisdictions advocate policies and incentives for broader SME access to hedging instruments, and technology is actively helping bridge the access gap that has historically disadvantaged smaller firms compared to large corporates.