TL;DR:

- Global FX daily turnover reaches 9.5 trillion dollars, increasing currency risk for companies.

- Effective FX management involves understanding transaction, translation, and economic risks, and choosing proper hedging tools.

- Flexible, continuous reassessment using technology is crucial for resilient FX programs in volatile markets.

Global FX turnover hits $9.5 trillion daily, yet many international companies still treat currency risk as a back-office nuisance rather than a board-level priority. That gap is expensive. A single unhedged quarter can erase months of operating margin, distort earnings reports, and rattle investor confidence. With geopolitical shocks, central bank divergence, and USD weakness reshaping currency markets in 2026, the stakes are higher than ever. This guide walks financial executives through the core FX risk concepts, compares the most effective hedging strategies, and outlines a practical path to building a program that actually holds up under pressure.

Table of Contents

- Why FX risk management matters for global companies

- Core FX risk concepts: Definitions and frameworks

- Key FX risk management strategies: Direct, hybrid, and dynamic

- Implementing and optimizing an FX risk management program

- The real edge: Flexibility and continuous reassessment beat static FX playbooks

- Take FX risk management further with CorpHedge

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| FX risk is significant | Currency volatility can sharply impact global companies’ earnings and financial stability. |

| Multiple hedging methods | Direct, hybrid, and dynamic strategies each offer unique cost and risk profiles. |

| Action beats passivity | Continuous reassessment and flexible programs outperform a set-and-forget approach. |

| Technology is a game-changer | AI and treasury platforms now enable better monitoring and adaptive FX risk strategies. |

Why FX risk management matters for global companies

Currency markets never sleep, and neither does the risk they generate. The FX market reached $9.5 trillion in daily turnover in 2025, creating both enormous opportunity and serious exposure for corporates operating across borders. Even a 2% swing in a major currency pair can translate into millions of dollars of unexpected cost or revenue shortfall for a mid-size multinational. That is not a rounding error. That is a strategic problem.

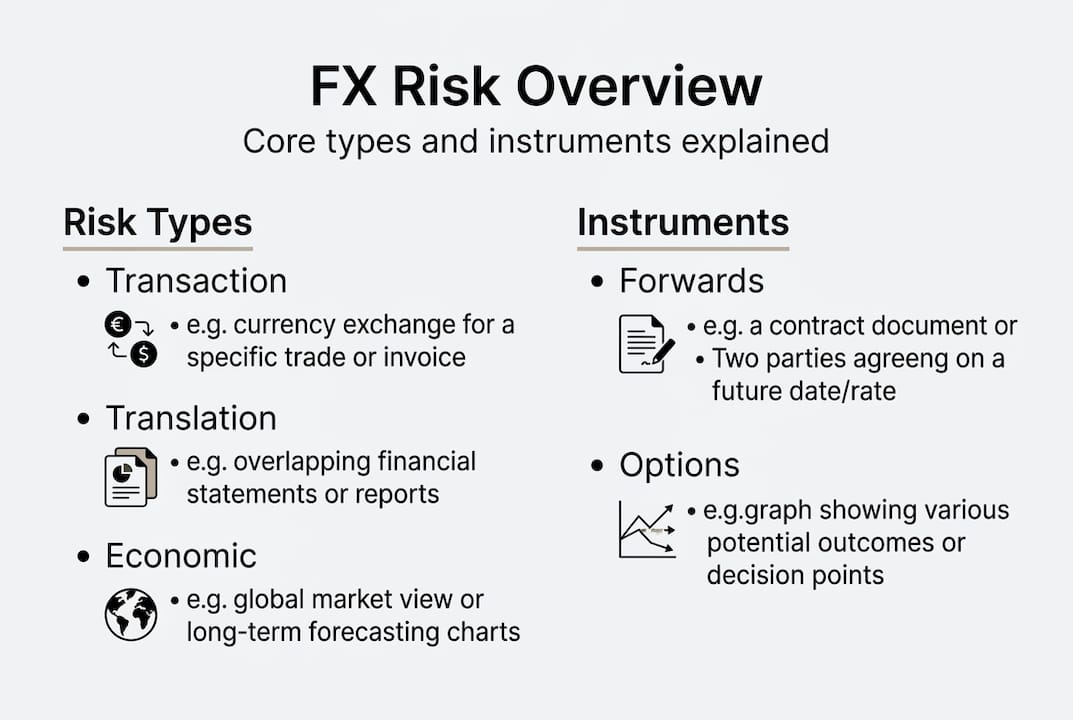

Currency swings hit companies in three distinct ways. First, they affect transaction risk, which is the direct impact on payables and receivables denominated in foreign currencies. Second, they create translation risk, distorting the reported value of overseas assets and earnings when consolidated into the parent company's home currency. Third, and most underappreciated, is economic risk, the long-term shift in competitive position when a currency move makes your products more or less attractive relative to foreign rivals. Understanding all three is the foundation of solid key FX risk types management.

Here is what makes this urgent right now. Geopolitical fragmentation, trade policy reversals, and diverging central bank paths have compressed the window between a macro event and a market-moving currency reaction. What used to take weeks now happens in hours. That speed punishes companies with slow or static hedge programs.

"Volatility is no longer episodic. It is structural. Companies that treat FX risk as a periodic concern rather than a continuous management discipline are systematically underpricing their exposure."

Up to 82% of North American corporates hedge currency risk, yet even sophisticated players face losses from underestimating exposure. The problem is rarely the hedging instrument. It is the governance structure around it. Weak risk governance for currencies leaves gaps between what the policy says and what the treasury team actually does.

Common exposure types at a glance:

- Transaction risk: invoices, contracts, and payments in foreign currency

- Translation risk: consolidation of foreign subsidiary financials

- Economic risk: competitive positioning and long-term cash flow impact

- Contingent risk: exposure tied to bids or contracts not yet awarded

Core FX risk concepts: Definitions and frameworks

Before you can manage FX risk, you need a shared language across your finance team. Misaligned definitions lead to misaligned hedges, and misaligned hedges cost money.

| Risk type | Definition | Primary impact |

|---|---|---|

| Transaction risk | Currency exposure on known future cash flows | P&L, cash flow |

| Translation risk | Restatement of foreign assets/liabilities | Balance sheet, EPS |

| Economic risk | Long-term competitive and cash flow shift | Strategic positioning |

Once you have mapped your exposure types, the next step is choosing the right instrument. The four main tools are forwards, futures, options, and swaps. Each has a distinct risk/reward profile.

| Instrument | Advantage | Drawback |

|---|---|---|

| Forward contract | Simple, customizable, locks in rate | No upside if rates move favorably |

| Futures | Standardized, liquid, exchange-traded | Basis risk, margin calls |

| Options | Flexibility, capped downside | Premium cost, complexity |

| Cross-currency swap | Effective for long-term debt hedging | Counterparty credit exposure |

The FX risk types and exposures you face should directly determine which instruments you use. Matching instrument to exposure is not optional. It is the core discipline.

There are also hidden risks that catch even experienced teams off guard. Basis risk, over-hedging, and counterparty exposure are three of the most common sources of unexpected loss. Basis risk occurs when the hedging instrument does not move in perfect sync with the underlying exposure, creating a gap. Over-hedging locks in costs on exposures that never materialize. Counterparty risk in swaps becomes critical when credit conditions tighten.

Pro Tip: Align your hedge horizon with your actual exposure duration. Hedging a 12-month receivable with a 3-month forward creates a rollover gap that adds cost and basis risk. Map the timeline first, then select the instrument.

Key FX risk management strategies: Direct, hybrid, and dynamic

Not all hedging strategies are created equal. The right approach depends on your exposure profile, risk tolerance, cash flow predictability, and the cost of capital. Three broad strategies dominate corporate practice.

Direct (static) hedging uses a fixed hedge ratio, typically 80 to 100%, applied consistently to all forecasted exposures. It is simple to administer and easy to audit. The downside is inflexibility. When your forecast is wrong, you are either over-hedged or under-hedged, and both outcomes cost money.

Hybrid hedging combines short-term instruments for near-term cash flows with longer-term structures for strategic exposures. This layered approach smooths the cost curve and reduces the binary risk of a single large hedge position.

Dynamic hedging adjusts the hedge ratio in response to market signals, model outputs, or predefined trigger points. It requires more analytical infrastructure but delivers better outcomes when markets move sharply.

| Strategy | Cost | Complexity | Volatility reduction |

|---|---|---|---|

| Static (direct) | Low | Low | Moderate |

| Hybrid | Medium | Medium | High |

| Dynamic | Medium-high | High | Very high |

Real-world results confirm the value of more sophisticated approaches. SolarTech's hybrid program cut volatility 41%, Disney's cross-currency swap saved $105 billion in interest costs, and HCL Tech shifted to hedge accounting after incurring losses from inconsistent practices. These are not edge cases. They are the direct result of strategy selection.

Here is how to assess and implement a dynamic or hybrid approach:

- Quantify your total currency exposure by type, currency pair, and time horizon

- Identify which exposures are highly predictable versus contingent

- Set a baseline static hedge for predictable flows (50% is a common starting point)

- Layer dynamic hedges on top for contingent or volatile exposures

- Define trigger rules for adjusting ratios based on market conditions

- Review currency risk best practices to benchmark your approach

Pro Tip: Layer dynamic (50%) and static (50%) hedges to balance cost and flexibility. This split gives you a stable baseline while preserving room to respond to market shifts without blowing up your hedge budget.

For a deeper look at what is working in 2026, the 2026 hedging strategies landscape has shifted toward more scenario-based and AI-assisted approaches. And if volatility is your primary concern, the mitigating FX volatility framework offers a structured path to reducing earnings swings.

Implementing and optimizing an FX risk management program

Strategy without execution is just a document. Building a functioning FX risk program requires clear steps, defined ownership, and the right technology.

Start by quantifying your exposures. Pull data from ERP systems, contract databases, and intercompany flows. Many companies discover exposures they did not know existed at this stage. Then select instruments matched to each exposure type and set a formal hedging policy that defines ratios, approved instruments, and escalation thresholds. Assign accountability to a named treasury owner, not a committee.

AI and treasury management systems now play a central role in streamlining dynamic and real-time FX monitoring. These tools can flag exposure breaches, model scenario outcomes, and automate hedge execution, reducing both latency and human error. The gap between companies using these tools and those relying on spreadsheets is widening fast.

"A static hedge policy designed in 2022 is not built for 2026 markets. The macro environment has changed structurally, and your program needs to reflect that."

Must-have success metrics for your FX program:

- Cash flow at risk (CFaR): measures potential shortfall from currency moves

- Volatility reduction percentage: compares hedged vs. unhedged earnings variance

- Hedge effectiveness ratio: tracks how closely hedges offset actual exposures

- Cost of hedging as a percentage of revenue: keeps program economics visible

- Counterparty credit exposure: monitors concentration risk in swap portfolios

For companies building from scratch, the risk reduction strategies framework provides a solid starting point. If you are refining an existing program, the forex hedging steps guide offers a practical checklist for closing gaps.

Pro Tip: Review and stress-test your hedge program quarterly. Run at least two macro shock scenarios, such as a 15% USD move or a sudden rate divergence between the Fed and ECB. A set-and-forget approach no longer works in 2026 conditions.

The real edge: Flexibility and continuous reassessment beat static FX playbooks

Here is the uncomfortable truth most FX consultants will not say out loud: the majority of corporate hedging programs are designed for the world as it was, not the world as it is. Companies build a policy, get sign-off, and then run it on autopilot for 18 months. By the time the next review comes around, the macro environment has shifted, the exposure profile has changed, and the hedge ratios are misaligned.

2025-26 volatility and USD weakness require a fundamental reassessment of FX management in light of geopolitical events. The companies winning in this environment are not necessarily using more sophisticated instruments. They are reviewing more frequently, adjusting faster, and using technology to close the gap between signal and action.

The so-called "random walk" baseline, where you start with a 50% dynamic hedge and adjust from there, is gaining traction precisely because it avoids the overconfidence trap. It acknowledges uncertainty and builds in room to respond. That is not a weakness. That is intellectual honesty about how currency markets actually work.

For a real-world look at how hedge accounting real-world results translate into financial statement outcomes, the evidence strongly favors programs built around flexibility and continuous review over rigid, policy-bound approaches.

Take FX risk management further with CorpHedge

Building a resilient FX risk program is not a one-time project. It is an ongoing discipline that requires the right tools, real-time data, and a platform that scales with your exposure complexity.

CorpHedge is built specifically for international companies that need end-to-end FX program design, live position monitoring, Value at Risk modeling, and seamless integration with platforms like Corpay. Whether you are starting from scratch or optimizing an existing program, our platform gives your treasury team the visibility and control to act faster and smarter. Explore what a structured approach looks like with a product tour, or dive into the full capability set when you explore features to see how CorpHedge fits your specific exposure profile.

Frequently asked questions

What are the main types of FX risk in international business?

The three primary FX risk types are transaction, translation, and economic risk, each affecting a different dimension of your financials, from cash flow to balance sheet to long-term competitive position.

How do companies typically hedge FX exposure?

Most use a combination of forwards, options, swaps, and increasingly hybrid or dynamic programs that adjust hedge ratios based on market conditions and exposure predictability.

Why has FX risk management evolved recently?

Rising volatility and geopolitical risk in 2025 and 2026 have made static programs obsolete, pushing companies toward more flexible, technology-driven, and data-informed FX strategies.

How often should FX risk programs be reviewed?

Best practice is at least quarterly, with scenario testing and reviews triggered by major market events such as central bank policy shifts or geopolitical shocks.