Forex volatility can erode your company's profit margins and destabilize cash flow faster than any operational inefficiency. For financial managers at international companies, currency swings represent a persistent threat that demands proactive risk management. This guide walks you through identifying your exposures, selecting the right hedging instruments, executing your strategy, and continuously refining your approach to maintain financial stability and competitive advantage in global markets.

Table of Contents

- Key takeaways

- Understanding your forex exposures and risks

- Preparing your hedging strategy and selecting instruments

- Executing your hedge and monitoring performance

- Evaluating results and refining your forex risk management approach

- Explore CorpHedge's advanced forex risk management solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Protects profits | Effective forex hedging shields the bottom line from unpredictable currency movements. |

| Identify exposures | Understanding transaction translation and economic exposures is the foundation for choosing hedging strategies. |

| Choose right instruments | Selecting forwards, options, and swaps depends on risk tolerance and business objectives. |

| Monitor and adjust | Ongoing monitoring keeps hedges aligned with market changes and company needs. |

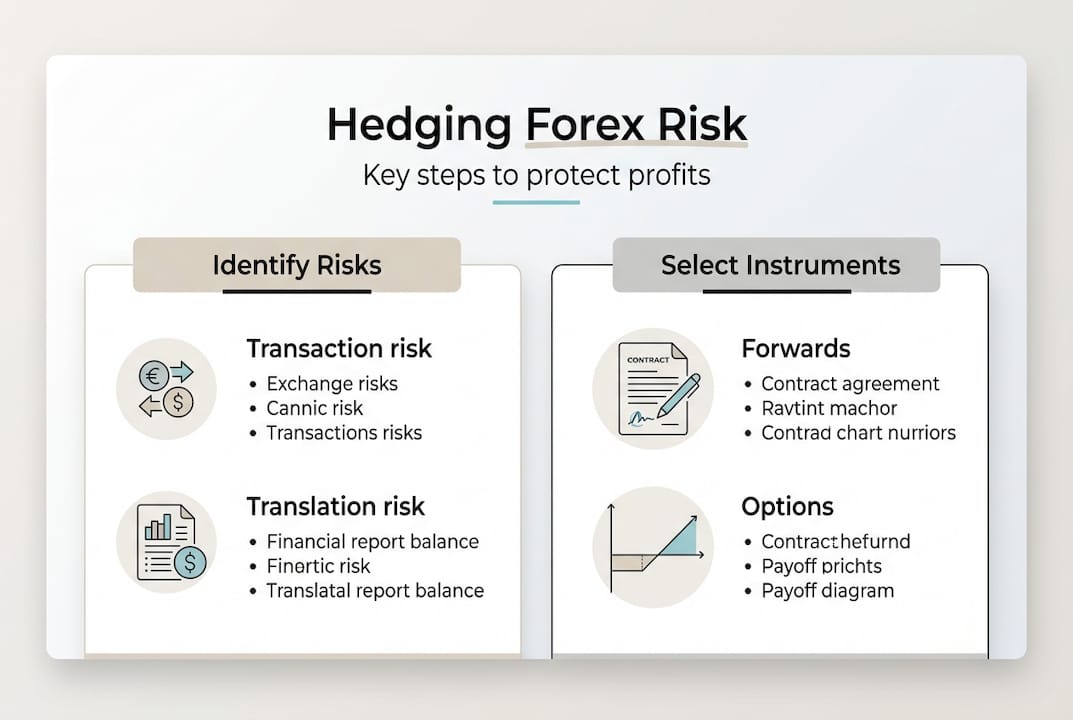

Understanding your forex exposures and risks

Before you can hedge effectively, you need a clear map of where currency risk lives in your organization. Transaction exposure is the most direct threat, arising from actual payments and receipts denominated in foreign currencies. When you invoice a European client in euros but report in dollars, the value of that receivable fluctuates until payment clears. A 5% currency swing can eliminate your entire margin on that sale.

Translation exposure affects how you consolidate financial statements from foreign subsidiaries. Even if no cash changes hands, converting overseas assets and liabilities into your reporting currency creates paper gains or losses that impact shareholder equity. This matters for public companies facing analyst scrutiny and private firms seeking financing. Economic exposure is subtler but potentially more damaging, as it influences your competitive position and future cash flows. If your competitor sources materials in a currency that weakens against yours, they gain a pricing advantage you must counter.

Common currency pairs like EUR/USD, GBP/USD, and USD/JPY each carry distinct volatility profiles driven by interest rate differentials, trade balances, and geopolitical events. Emerging market currencies often exhibit higher volatility, amplifying risk for companies operating in those regions. Proper identification of transaction, translation, and economic exposures is critical to effective hedging, as each type requires tailored strategies and instruments.

Your internal financial reporting systems must capture exposure data with precision. This means tracking every foreign currency invoice, intercompany loan, and committed contract in a centralized database. Many companies discover hidden exposures in supply chain commitments or planned capital expenditures only after suffering unexpected losses. Regular exposure reporting to treasury and senior management creates accountability and enables timely hedging decisions.

Pro Tip: Build a rolling 12 month exposure forecast that updates monthly. This forward visibility lets you hedge strategically rather than reactively, often securing better pricing and avoiding panic decisions during volatility spikes.

Key steps to map your exposures:

- Catalog all foreign currency receivables, payables, and committed contracts

- Identify subsidiaries reporting in different currencies and their net asset positions

- Assess how currency movements affect your pricing power versus competitors

- Quantify exposure by currency pair and time horizon

- Review forex currency hedging use cases to see how similar companies structure their analysis

Preparing your hedging strategy and selecting instruments

With exposures identified, you face a menu of hedging instruments, each offering different trade-offs between cost, flexibility, and protection. Currency forwards are the workhorse of corporate hedging, obligating both parties to exchange currencies at a predetermined rate on a future date. They lock in certainty but eliminate the ability to benefit if rates move in your favor. Options provide the right but not the obligation to exchange currency, preserving upside potential while capping downside risk. This flexibility comes at a premium cost that can be substantial for volatile currency pairs.

Swaps involve exchanging principal and interest payments in different currencies, useful for companies with ongoing foreign currency debt or revenue streams. They can be structured to match specific cash flow patterns but require more sophisticated treasury capabilities to manage. Selecting the right combination of forwards, options, and swaps helps tailor risk management to business needs, balancing protection with cost efficiency.

| Instrument | Best for | Pros | Cons |

|---|---|---|---|

| Currency forwards | Known future payments | Low cost, full protection | No upside participation |

| Currency options | Uncertain exposures | Flexibility, upside potential | Premium cost, complexity |

| Currency swaps | Long term debt or revenue | Matches cash flow patterns | Requires sophisticated management |

Your hedge ratio determines what percentage of exposure you protect. A 100% hedge eliminates currency risk but also removes any potential gains. Many companies hedge 50 to 75% of near term exposures, leaving some upside participation while still providing meaningful protection. The appropriate ratio depends on your risk appetite, margin structure, and competitive dynamics. Companies with thin margins typically hedge more aggressively than those with pricing power.

Matching hedge terms to exposure timing is critical. Hedging a 90 day receivable with a 180 day forward creates basis risk if you need to unwind early. Rolling short term hedges can be more flexible but generates transaction costs and requires active management. Consider these factors when structuring your program:

- Cost of hedging relative to potential loss exposure

- Degree of flexibility needed for uncertain timing or amounts

- Level of protection required based on margin sensitivity

- Internal capabilities and systems for managing different instruments

- Counterparty credit quality and relationship pricing

Involving stakeholders from sales, procurement, and operations ensures your hedging strategy aligns with business realities. A hedge that protects treasury might inadvertently constrain sales flexibility if not coordinated. Document your approach in a formal policy that specifies hedge ratios, approved instruments, tenor limits, and approval authorities. This creates consistency and supports audit requirements.

Pro Tip: Start simple with plain vanilla forwards for your largest, most certain exposures. Add complexity only as your team gains experience and your systems can support more sophisticated structures. Explore FX exposure management features that automate instrument selection based on your exposure profile.

Executing your hedge and monitoring performance

Execution transforms strategy into protection. For currency forwards, you contact your bank or trading platform, specify the currency pair, amount, and settlement date, then confirm the locked in rate. Most corporate treasury teams maintain relationships with multiple banks to ensure competitive pricing and backup capacity. Electronic trading platforms have made execution faster and more transparent, with real time pricing and automated confirmation.

Options require additional decisions around strike price and expiration. An at the money option with a strike at current spot rate costs more but provides immediate protection. Out of the money options are cheaper but only protect against larger moves. Your choice depends on budget constraints and the degree of protection needed. Once executed, both forwards and options must be documented in your treasury management system with details on notional amount, rates, counterparty, and settlement instructions.

Real time monitoring is non negotiable in today's volatile markets. You need systems that show current mark to market values of all hedges, remaining open exposures, and aggregate risk metrics. Continuous monitoring and timely adjustments are essential to optimize hedging outcomes and avoid unexpected losses, especially when business conditions shift unexpectedly. A major customer delaying payment or a supplier demanding early settlement can instantly change your exposure profile.

Integrating hedge accounting into financial reporting requires careful documentation to qualify for hedge accounting treatment under accounting standards. This allows you to defer gains and losses on effective hedges, matching them with the underlying exposure. Without proper hedge accounting, mark to market swings create artificial earnings volatility that obscures actual business performance. Work closely with your accounting team to establish documentation at hedge inception and perform ongoing effectiveness testing.

Common execution mistakes can undermine even well designed strategies:

- Overhedging beyond actual exposure creates speculative positions that increase rather than reduce risk

- Ignoring changes in exposure amounts or timing as business conditions evolve

- Failing to diversify counterparties, concentrating credit risk with one or two banks

- Neglecting to train finance staff on hedge mechanics, leading to operational errors

- Poor communication between treasury and business units about hedge status and constraints

Transparency with senior management about hedge performance prevents surprises. Regular reporting should show protected versus unprotected exposures, realized gains or losses on settled hedges, and mark to market impact on open positions. This visibility enables informed decisions about adjusting hedge ratios or instruments as market conditions change.

"The biggest hedging failures come not from wrong market calls but from mismatches between hedge structures and actual business exposures. Operational discipline matters more than market timing."

Pro Tip: Schedule quarterly hedge reviews with business unit leaders to validate exposure forecasts and adjust hedge coverage. Markets move fast, but business plans change faster. A product tour of risk management solutions shows how integrated platforms streamline this coordination.

Evaluating results and refining your forex risk management approach

Measuring hedge effectiveness separates successful programs from expensive failures. The hedge effectiveness ratio compares the change in hedge value to the change in exposure value, with ratios between 80% and 125% generally qualifying for hedge accounting. Calculate this quarterly to confirm your hedges are performing as designed. A ratio outside this range signals a mismatch requiring investigation and potential restructuring.

Cost benefit analysis quantifies whether hedging expenses are justified by risk reduction. Sum your hedging costs including premiums, bid ask spreads, and internal management expenses, then compare against the volatility reduction achieved. If you spent $500,000 to eliminate $2 million of potential loss exposure, that represents strong value. But if hedging costs approach potential losses, you might be overhedging or using inefficient instruments.

| Evaluation method | What it measures | When to use |

|---|---|---|

| Hedge effectiveness ratio | How well hedge offsets exposure | Quarterly for accounting compliance |

| Value at Risk analysis | Maximum potential loss at confidence level | Risk committee reporting and limit setting |

| Realized P&L review | Actual gains and losses on settled hedges | Monthly performance assessment |

| Volatility reduction | Decrease in earnings or cash flow variance | Annual strategy evaluation |

Value at Risk analysis estimates the maximum loss you could experience over a specified period at a given confidence level. A 95% VaR of $1 million means you have a 5% chance of losing more than $1 million in the measurement period. This metric helps set appropriate hedge coverage and communicate risk exposure to boards and executives in intuitive terms. Compare VaR before and after hedging to quantify risk reduction.

Realized profit and loss review on settled hedges reveals whether your timing and instrument choices delivered value. Some hedges will show losses when rates move favorably, but that is the cost of insurance. The question is whether aggregate results justify the program expense. Regular evaluation against benchmarks allows companies to refine tactics and improve financial stability, turning hedging from a cost center into a strategic advantage.

Areas requiring ongoing refinement:

- Hedge ratios that prove too conservative or aggressive based on actual volatility

- Instrument mix that is overly expensive or insufficiently flexible

- Counterparty relationships that do not provide competitive pricing or adequate capacity

- Forecast accuracy that creates mismatches between hedges and actual exposures

- Documentation processes that fail to support hedge accounting qualification

Best practices for continuous improvement include maintaining detailed records of all hedging decisions with rationale, conducting post mortems on significant gains or losses to extract lessons, benchmarking your program against industry peers through surveys or consultants, and staying current on new instruments and market developments. Compliance checks verify adherence to your hedging policy and regulatory requirements, protecting against unauthorized trading or excessive risk taking.

Your hedging approach should evolve as your company grows and market conditions shift. A startup with limited forex exposure might rely on simple forwards, while a multinational with complex supply chains needs sophisticated multi currency strategies. Regular strategy reviews with treasury, finance, and business leaders ensure alignment with corporate objectives and risk tolerance. Review your corporate fx risk management use case annually to incorporate new capabilities and market insights.

Explore CorpHedge's advanced forex risk management solutions

Implementing these strategies requires robust tools that integrate exposure analysis, hedge execution, and performance tracking. CorpHedge provides a comprehensive platform designed specifically for corporate financial managers facing forex risk. Our system automatically aggregates exposures from your ERP and financial systems, recommends optimal hedge structures based on your policy parameters, and monitors effectiveness in real time.

You gain visibility into every currency position across your organization, with drill down capability to individual transactions. Scenario analysis shows how different hedging approaches would perform under various market conditions, supporting informed decisions. Integration with major banks and trading platforms enables seamless execution without leaving the system. Explore our foreign exchange risk management solutions product tour to see how leading companies automate their hedging workflows. Review detailed FX exposure management features that eliminate manual processes and reduce errors. See real world examples in our corporate fx risk management use case library showing measurable results from companies like yours.

Frequently asked questions

What is the difference between transaction and translation exposure?

Transaction exposure arises from actual foreign currency cash flows like receivables, payables, or committed contracts that will settle at future dates. Translation exposure affects consolidated financial statements when you convert foreign subsidiary assets and liabilities into your reporting currency, creating accounting gains or losses without immediate cash impact. Transaction exposure directly threatens cash flow and margins, while translation exposure impacts reported equity and financial ratios.

How do currency options differ from forwards in hedging?

Currency options give you the right but not the obligation to exchange currency at a predetermined rate, allowing you to benefit if rates move favorably while limiting downside risk. Forwards obligate both parties to exchange currency at the agreed rate regardless of market movements, providing certainty but eliminating upside potential. Options cost more due to the premium you pay for flexibility, while forwards typically have minimal upfront cost but lock you into the rate.

What are common mistakes to avoid when hedging forex risk?

Overhedging beyond your actual exposure transforms risk management into speculation, potentially amplifying losses rather than reducing them. Ignoring ongoing changes in business conditions creates mismatches when forecasted exposures do not materialize or timing shifts unexpectedly. Failing to document your hedging strategy and maintain proper records jeopardizes hedge accounting treatment and creates compliance risks. Poor communication between treasury and business units leads to operational errors and missed hedging opportunities.

How often should I review and adjust my hedging strategy?

Review your hedging strategy quarterly at minimum, with monthly monitoring of exposure forecasts and hedge performance. Major business changes like new contracts, market entries, or strategic shifts require immediate review regardless of schedule. Market volatility spikes or significant currency moves may warrant interim adjustments to hedge ratios or instruments. Annual comprehensive reviews should reassess your entire approach including policy parameters, approved instruments, and risk tolerance alignment with corporate objectives.