TL;DR:

- Most companies underestimate the importance of a structured, dynamic approach to FX risk mitigation.

- Integrating FX risk management into enterprise risk frameworks improves governance, response speed, and cost efficiency.

- Static hedging often underperforms compared to flexible, signal-driven strategies that adjust for market changes.

A staggering 76% of UK and US corporates reported unhedged FX losses in 2024, yet most finance teams still operate without a structured risk mitigation framework. Currency swings can quietly erode margins, distort earnings reports, and destabilize cash flow forecasts before anyone in the boardroom notices. The gap between companies that manage FX risk well and those that don't isn't about access to information. It's about having a clear, repeatable process. This article breaks down what FX risk mitigation actually means, which strategies deliver real results, and how to integrate them into a framework your organization can act on.

Table of Contents

- What is risk mitigation in the context of FX?

- Core strategies and tools for mitigating FX risk

- Integrating risk mitigation with enterprise risk management (ERM)

- Advanced considerations: Dynamic vs static mitigation and best practices

- The uncomfortable truth about risk mitigation: What most companies miss

- Explore smarter FX risk mitigation with CorpHedge

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Integrate ERM with FX | Combining enterprise risk management and FX hedging creates stronger and more adaptive risk reduction. |

| Dynamic strategies outperform | Dynamic and hybrid approaches typically deliver better results than static models for international companies. |

| No one-size-fits-all | Optimal risk mitigation depends on each firm’s exposures, economics, and operating realities. |

| Practical tools matter | Using advanced hedging tools, operational tactics, and data helps maximize profit protection and minimize volatility. |

What is risk mitigation in the context of FX?

Risk mitigation, in the FX context, means identifying your company's exposure to currency movements and taking deliberate steps to reduce the financial damage those movements can cause. It's not about eliminating risk entirely. That's neither possible nor desirable. It's about controlling how much of that risk reaches your bottom line.

FX risk shows up in three distinct forms that every corporate finance professional should know:

- Transaction risk: The risk that exchange rate changes will affect the value of a specific cross-border payment or receivable before it settles.

- Translation risk: The risk that consolidating foreign subsidiary financials into your reporting currency will produce distorted results.

- Economic risk: The longer-term risk that currency shifts will erode your competitive position in global markets, affecting pricing power and future revenue streams.

Each type requires a different mitigation response. Transaction risk is typically handled with short-dated instruments. Economic risk demands a more strategic, structural approach.

"The goal of FX risk mitigation isn't to predict where currencies go. It's to make sure that wherever they go, your business stays on track."

Why does this matter so much? Because unmanaged FX exposure creates cash flow unpredictability, which cascades into lower market valuations, weaker investor confidence, and reduced capacity to plan capital allocation. Companies with formal hedging programs see 23% less earnings volatility, which translates directly into more reliable forecasting and stronger stakeholder trust.

For a deeper look at how volatility connects to profitability, mitigating volatility in FX is a useful starting point. And if you're still building the foundation, FX risk management basics covers the essential building blocks before you layer in more advanced tools.

The bottom line is that risk mitigation is not a one-time fix. It's an ongoing discipline that requires clear policy, defined exposure thresholds, and regular review cycles. Companies that treat it as a checkbox exercise consistently underperform those that embed it into their financial planning process.

Core strategies and tools for mitigating FX risk

Once you understand what you're protecting against, the next question is how. The toolkit for FX risk mitigation is broad, and choosing the right combination depends on your firm's size, currency mix, and risk appetite.

The main categories of mitigation tools include:

- Forward contracts: Lock in an exchange rate for a future transaction. Simple, predictable, and widely used for transaction risk.

- Options: Buy the right, but not the obligation, to exchange at a set rate. More flexible than forwards, but carry a premium cost.

- Cross-currency swaps: Exchange principal and interest in different currencies over a set period. Useful for managing long-term economic exposure.

- Natural hedges: Structure operations so that revenues and costs occur in the same currency, reducing net exposure without derivatives.

- Netting: Consolidate offsetting payables and receivables across subsidiaries to reduce the gross volume of FX transactions.

Financial hedging with derivatives consistently outperforms purely operational approaches. FX derivatives reduce cash-flow variance by 8 to 12% for exposed firms, a meaningful improvement when you're managing multi-currency portfolios at scale.

| Strategy | Best for | Cost | Flexibility |

|---|---|---|---|

| Forward contracts | Transaction risk | Low | Low |

| FX options | Uncertain exposures | Medium | High |

| Cross-currency swaps | Long-term economic risk | Medium | Medium |

| Natural hedges | Structural exposure | None | Low |

| Netting | Intercompany flows | Low | Medium |

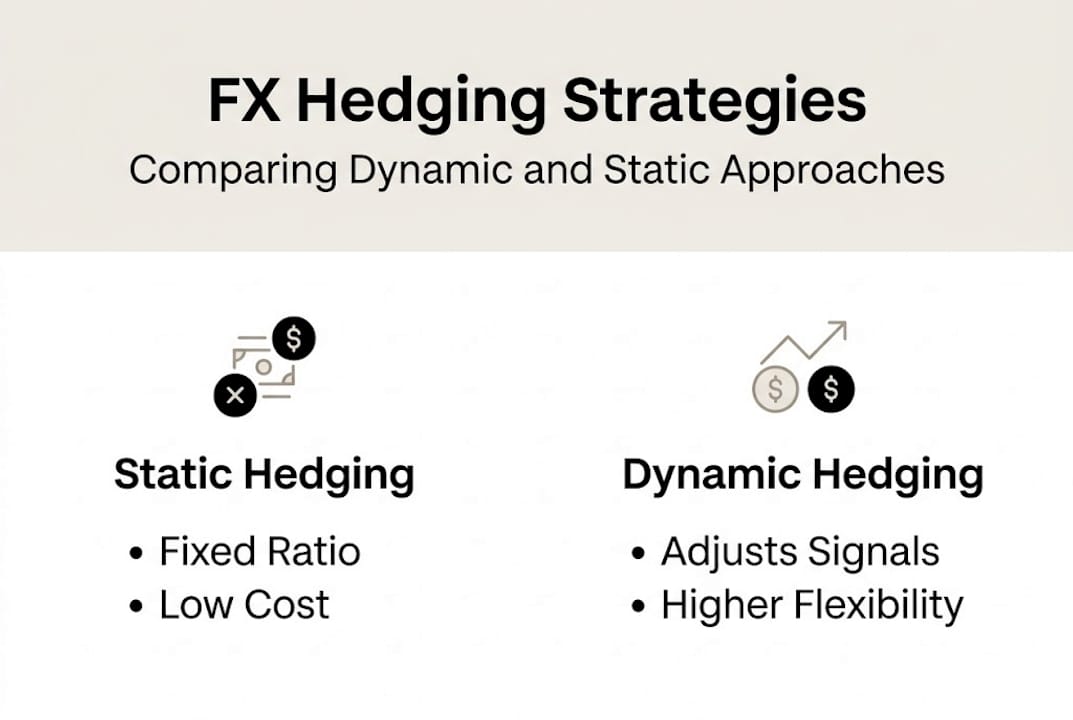

Static hedging, where you set a fixed hedge ratio and leave it, is easy to implement but often misses the mark when market conditions shift. Dynamic strategies that incorporate volatility signals, carry differentials, and momentum factors tend to outperform over time. Research on hybrid FX hedging tools from the BIS confirms that combining short-term and long-term instruments can smooth out both cost and protection gaps.

For a structured overview of instrument selection, FX hedging strategies walks through the decision logic in detail. If you want to connect hedging choices to your broader risk governance, ERM in currency risk is worth reading alongside it.

Pro Tip: Dynamic strategies that incorporate volatility, carry, and momentum signals can significantly outperform static hedges in developed markets. Start with a rules-based dynamic overlay on top of your core static hedge before committing to a full dynamic program.

Integrating risk mitigation with enterprise risk management (ERM)

FX risk doesn't exist in isolation. It intersects with credit risk, operational risk, and market risk in ways that a siloed hedging program will never fully capture. That's why embedding FX mitigation within your enterprise risk management (ERM) framework isn't optional. It's where the real efficiency gains live.

A unified ERM approach delivers three concrete benefits:

- Better governance: Risk policies are consistent across business units, reducing the chance of conflicting hedge positions.

- Coordinated response: When a market shock hits, an integrated framework allows faster, more coherent action across treasury, finance, and operations.

- Stronger risk culture: When FX is treated as part of enterprise risk rather than a treasury silo, senior leadership engages more meaningfully with exposure decisions.

The contrast between siloed and integrated approaches is stark:

| Dimension | Siloed FX management | Integrated ERM approach |

|---|---|---|

| Visibility | Limited to treasury | Company-wide |

| Response speed | Slow, fragmented | Fast, coordinated |

| Cost efficiency | Higher transaction costs | Netting and pooling benefits |

| Governance | Inconsistent | Policy-driven |

| Adaptability | Reactive | Proactive |

Research on ERM and dynamic FX hedging confirms that in international firms, integrating ERM with FX hedging and applying dynamic strategies using carry and momentum signals produces measurably better outcomes than either approach alone.

For practical guidance on how to structure this integration, ERM integration best practices covers governance frameworks and policy design. If you're managing exposure across multiple entities, enterprise currency risk management addresses the coordination challenges specific to multinational structures.

The key is to make FX exposure a standing agenda item in your enterprise risk committee, not just a quarterly treasury report. That shift in cadence alone changes how proactively your organization responds to currency developments.

Advanced considerations: Dynamic vs static mitigation and best practices

Most companies start with static hedging because it's simple. Set a hedge ratio, execute the instruments, review quarterly. That works well enough in stable markets. But when volatility spikes or carry dynamics shift, static programs can leave significant value on the table or, worse, lock in unfavorable rates at exactly the wrong moment.

Dynamic approaches adjust hedge ratios based on real-time signals: volatility levels, interest rate differentials (carry), and price momentum. Static strategies miss upside; dynamic hedges can yield returns approximately 100 basis points higher, though they add complexity and operational cost. That tradeoff is worth it for firms with large, diversified FX exposures. For smaller or less complex books, a hybrid approach often makes more sense.

"The most dangerous assumption in FX hedging is that what worked last year will work this year. Markets evolve. Your strategy should too."

Here are the steps for applying best practices in your mitigation program:

- Map all exposures across transaction, translation, and economic dimensions before selecting any instruments.

- Define your hedge ratio range rather than a fixed number. A range of 50 to 80% gives you flexibility without leaving you fully exposed.

- Incorporate volatility signals into your review triggers. Don't just review on a calendar schedule. Review when market conditions cross defined thresholds.

- Avoid binary decisions. Partial hedges are almost always better than all-or-nothing positions, especially in currencies with high carry or strong momentum trends.

- Monitor Asian trading hours separately if you have significant Asia-Pacific exposure. Volatility patterns during those sessions differ materially from European and US hours.

For a current look at what's working, hedging best practices covers the 2026 landscape in detail. And for the technology side of execution, FX risk management tools reviews the platforms and analytics that make dynamic programs operationally feasible.

Pro Tip: Never approach FX hedging as all or nothing. Optimal hedge ratios and covariance-aware strategies that account for correlations across your currency pairs will consistently outperform both unhedged and fully hedged positions over a full market cycle.

The uncomfortable truth about risk mitigation: What most companies miss

Here's what we see consistently: companies invest in hedging programs, build governance frameworks, and still underperform. The reason is almost never the instruments they chose. It's the assumptions they never questioned.

The biggest myth in corporate FX management is that more hedging equals more safety. A full hedge is rarely optimal for multinational companies because their cash flows are naturally multi-currency and carry considerations create real costs. Locking in 100% of exposure can actually increase risk when your economic exposure diverges from your accounting exposure.

We've seen this play out in recent market cycles where companies with rigid, fully hedged programs took losses when their operational revenues shifted currency mix mid-year but their hedge book didn't adjust. The hedge became the problem.

What actually drives better outcomes is a willingness to treat FX risk as dynamic by nature. That means challenging your hedge ratios at least quarterly, using ERM data to inform posture changes, and accepting that the right answer in January may be wrong by June. It also means being honest about economic exposure, not just what shows up in your accounting statements.

For firms ready to move beyond conventional approaches, advanced FX risk strategies covers the analytical frameworks that support more adaptive programs.

Explore smarter FX risk mitigation with CorpHedge

Understanding the frameworks is one thing. Executing them at scale, across multiple currencies, entities, and time horizons, is where most teams hit operational limits. That's exactly the gap CorpHedge is built to close.

CorpHedge gives corporate finance and treasury teams a single platform to monitor real-time currency positions, apply Value at Risk-based strategy logic, and manage hedge execution without the spreadsheet overhead. Whether you're implementing a dynamic overlay or building out your first formal ERM integration, the FX exposure management features are designed for the complexity that international firms actually face. Take a product tour to see how it works in practice, or visit CorpHedge to learn how leading finance teams are using the platform to protect margins and reduce earnings volatility.

Frequently asked questions

What is the best method to mitigate foreign exchange risk?

Combining financial hedging with dynamic strategy adjustments delivers the strongest results. Dynamic strategies using carry and momentum outperform static approaches in most developed markets, especially when integrated with a broader ERM framework.

Is a full hedge always the safest choice for corporates?

No. A full hedge reduces flexibility and can increase net risk for multinationals with complex, multi-currency cash flows. A full hedge is rarely optimal once carry costs and economic exposure mismatches are factored in.

How do static and dynamic FX hedging compare in results?

Static hedging is simpler and cheaper to run, but dynamic models that adjust on volatility, trend, and carry signals can generate returns roughly 100bps higher with better risk-adjusted performance when managed well.

What is the role of ERM in FX risk mitigation?

ERM provides the governance structure and cross-functional visibility that makes FX hedging more effective. Integrating ERM with FX hedging centralizes risk oversight and enables faster, more coordinated responses to market events.

Why do many companies still suffer FX losses despite using hedges?

Most rely on static or incomplete strategies and fail to adjust dynamically as conditions change. 76% of UK and US corporates still faced unhedged losses in 2024, reflecting how widespread the gap between having a hedge and having an effective one remains.