TL;DR:

- Currency swings can significantly impact operating margins if not properly managed.

- Effective forex risk mitigation involves assessing exposure, natural hedging, and structured financial instruments.

- Strong governance and active monitoring are essential for successful and cost-effective FX risk strategies.

Currency swings can erase months of operating margin in a single quarter, and the threat is intensifying. 63% of CFOs expect increased FX volatility in 2026, yet many finance leaders still rely on ad hoc responses rather than structured programs. This guide walks you through every layer of a best-practice mitigation framework, from mapping raw exposure to deploying dynamic hedging models, so you can protect profits, preserve cash flows, and stop letting exchange rates dictate your earnings.

Table of Contents

- Assessing your company's forex risk exposure

- Implementing natural hedging strategies

- Using financial hedging instruments

- Adapting with dynamic and advanced hedging models

- Governance, policy, and ongoing verification

- What most companies get wrong about forex volatility mitigation

- Enhance your forex risk management strategy with CorpHedge

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Start with natural hedges | Operational solutions like currency matching are zero-cost and effective for predictable cash flows. |

| Use financial instruments wisely | Deploy forwards, options, and swaps in alignment with business operations to reduce volatility efficiently. |

| Leverage dynamic strategies | Dynamic and regime-switching models offer superior risk reduction for complex or highly-volatile exposures. |

| Prioritize governance | Board-level FX policy and ongoing monitoring are critical for comprehensive risk coverage and compliance. |

| Hybrid approaches cut costs | Blending operational and financial hedges yields better cost and risk outcomes than standalone methods. |

Assessing your company's forex risk exposure

Before you hedge a single dollar, you need a clear picture of what you actually own. Forex risk sits in three places: your balance sheet (foreign-currency assets and liabilities), your income statement (revenues and costs denominated in different currencies), and your intercompany flows (loans, royalties, and trade payables between subsidiaries). Missing any one of these creates blind spots that derivatives alone cannot fix.

Start by running a currency concentration analysis. List every currency in which you receive revenue or pay costs, then calculate the net exposure per currency pair. A company that earns 40% of revenue in euros but sources only 10% of costs in euros carries a 30% unhedged net long position. That mismatch is where volatility strikes hardest, and it is usually the last place finance teams look.

| Exposure type | Where it appears | Measurement method |

|---|---|---|

| Transaction exposure | Invoices, payables, receivables | Mark-to-market per invoice |

| Translation exposure | Consolidated balance sheet | Functional currency restatement |

| Economic exposure | Future revenue streams | Scenario and sensitivity analysis |

| Intercompany exposure | Internal loans and royalties | Net intercompany flow mapping |

Diversification across currencies and operations reduces single-currency impact, and multi-currency accounts add operational flexibility that no derivative can replicate. This is structural protection, and it costs almost nothing compared to the premium you pay for options.

Common readiness gaps to address immediately:

- No documented FX policy ratified at board level (a problem for 51% of companies heading into 2026)

- Exposure data sitting in disconnected ERP systems with no central aggregation

- No defined hedging horizon or ratio, leaving treasury to improvise each quarter

- Subsidiary-level hedging that conflicts with group-level strategy, multiplying costs

Building smart forex risk management starts here, not with a Bloomberg terminal. You cannot hedge what you have not measured, and you cannot measure what you have not mapped. Dedicate the first 30 days of any new program to exposure mapping before touching a single instrument.

Pro Tip: Run a "stress test" on your top three currency pairs using the worst quarterly move of the past five years. If that scenario would breach your EBIT margin by more than 2 percentage points, your current natural hedges are insufficient and financial instruments are justified.

With the FX risk landscape defined, the next step is to select practical, cost-efficient hedging tactics.

Implementing natural hedging strategies

Natural hedging is the art of restructuring operations so that currency exposures cancel each other out before any financial instrument is needed. It is not glamorous, but it is the most cost-effective layer of any FX program, and it should always come first.

The core tactics break down as follows:

- Currency matching: Invoice customers in the same currency you use to pay suppliers. A European manufacturer selling to U.S. clients can price in USD if its raw material imports are also USD-denominated, creating a near-perfect offset.

- Netting: Instead of settling dozens of intercompany transactions individually, consolidate them into a single net payment per period. This cuts transaction volume and eliminates redundant conversions.

- Leading and lagging: Accelerate (lead) or defer (lag) payments depending on expected currency direction. If the euro is expected to strengthen, a eurozone subsidiary should pay USD-denominated invoices early while the rate is favorable.

- Internal invoicing: Centralize procurement through a treasury center that invoices subsidiaries in their local currency, concentrating FX exposure in one entity with a dedicated risk management mandate.

| Natural hedge tactic | Best suited for | Estimated cost | Limitation |

|---|---|---|---|

| Currency matching | Exporters with matched supply chains | Zero | Requires supplier flexibility |

| Netting | Multinationals with dense intercompany flows | Near zero | Needs netting center setup |

| Leading/lagging | Short-term payables management | Minimal | Cash flow timing constraints |

| Internal invoicing | Centralized treasury structures | Low setup cost | Regulatory complexity |

Natural hedging through currency matching, netting, leading and lagging payments, and internal invoicing eliminates exposure at zero cost for predictable cash flows. The critical qualifier is "predictable." When cash flows are seasonal, contract-driven, or tied to long project cycles, natural hedges cover the baseline, but unpredictable spikes will still require financial instruments.

Pro Tip: Synchronize cash inflows and outflows in the same currency where possible by negotiating payment terms with both customers and suppliers simultaneously. Aligning a 60-day receivable in GBP with a 60-day payable in GBP removes the exchange rate from the equation entirely.

Explore additional currency volatility prevention methods to build out your operational toolkit before layering on derivative products. And when you are ready to protect profits through instruments, the guide on how to hedge forex risk provides the logical next step.

Operational levers are foundational, but often require supplementing with financial instruments when exposures are unpredictable.

Using financial hedging instruments

Financial instruments exist to cover what operational tactics cannot. The three workhorses are forward contracts, options, and cross-currency swaps. Each serves a distinct purpose, and choosing the wrong one wastes premium while leaving real risk uncovered.

-

Forward contracts lock in an exchange rate for a future date. They are ideal for predictable cash flows where you know both the amount and the timing. A forward is free of upfront premium, which makes it the default choice for most treasury teams, but it eliminates upside potential as well as downside risk.

-

Currency options provide the right, but not the obligation, to exchange at a set rate. They suit situations where cash flow amounts are uncertain, for example a bid that may or may not be won. Options structured correctly can reduce premium costs by 68% through collar strategies that trade away some upside in exchange for a lower premium outlay.

-

Cross-currency swaps exchange both principal and interest payments in different currencies over a defined period. They are the right tool for long-term financing exposures, and they deliver roughly a 41% volatility reduction for multi-year commitments compared to leaving the exposure unhedged.

-

Hybrid combinations are the highest-ROI approach. Layering a forward over a naturally hedged baseline produces results that neither instrument achieves alone. Hybrid strategies combining natural and financial hedges reduce FX beta by 30.5% and total hedging costs by 29% compared to standalone derivative approaches. That is a meaningful efficiency gain for any treasury function under budget pressure.

When integrating financial instruments, think in layers. Cover your natural hedge baseline first, then apply forwards to confirmed exposures, then use options for contingent or uncertain flows. This sequence avoids overhedging, which is a real and costly error that inflates accounting complexity without reducing risk.

Review advanced FX risk strategies to understand how leading treasury functions sequence these instruments across different exposure horizons.

Pro Tip: Avoid over-relying on derivatives without supporting operational tactics. A company that hedges 100% of its transaction exposure with forwards but ignores its translation exposure is spending premium on a partial solution. Map all three exposure types first, then allocate instruments where operational hedges fall short.

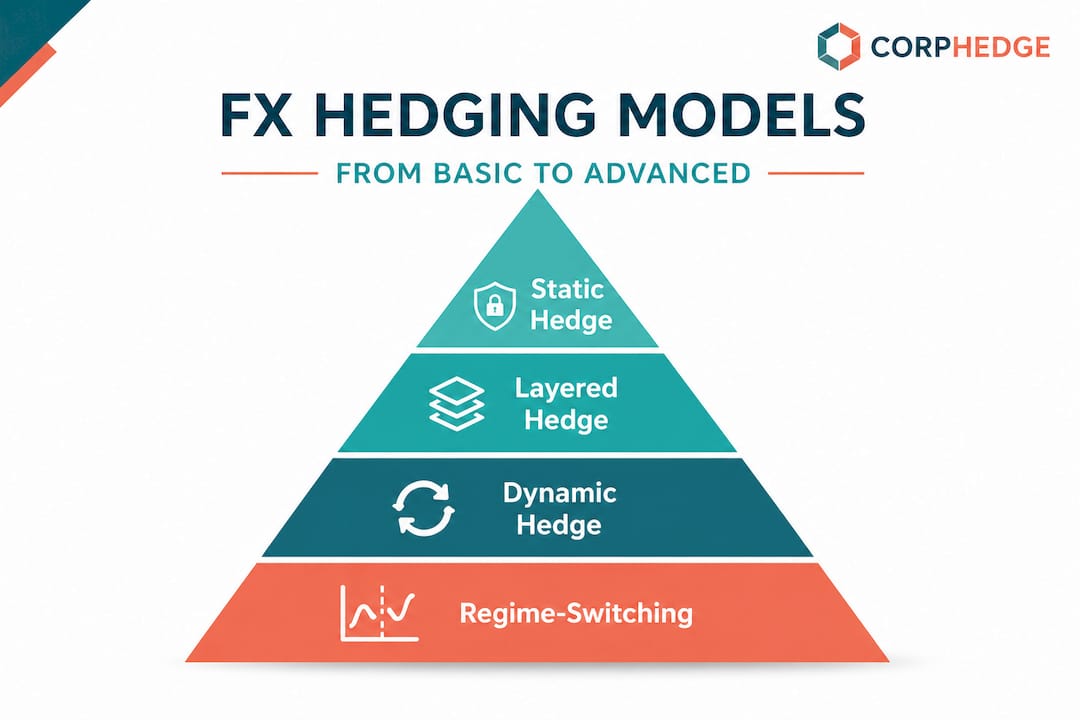

As market conditions shift, static hedges can falter, which brings us to advanced and adaptive hedging approaches.

Adapting with dynamic and advanced hedging models

Static hedging programs, where you set a ratio and roll it forward every quarter, work well in stable markets. They fail badly when volatility regimes change suddenly, which is exactly what happened during the 2022 dollar surge, the 2023 yen collapse, and the ongoing turbulence in emerging market currencies.

Dynamic hedging adjusts the hedge ratio continuously based on observed market conditions, currency correlations, and realized volatility. Dynamic hedging adjusts ratios based on these inputs and is superior for volatile currencies because it explicitly captures fat tails, the rare but catastrophic moves that static models systematically underestimate.

The most sophisticated version is regime-switching hedging, which uses statistical models to identify which market "state" you are in (low volatility, high volatility, trending, mean-reverting) and adjusts the hedge accordingly. Regime-switching models using four states outperform both static and standard dynamic benchmarks, with the highest risk reduction achieved on USD, EUR, JPY, and TRY pairs.

Here is a practical workflow for implementing a dynamic model:

| Step | Action | Output |

|---|---|---|

| 1. Classify exposures | Segment by currency, horizon, and certainty | Exposure map by regime sensitivity |

| 2. Define regime indicators | Select volatility index triggers (e.g., VIX, implied vol) | Regime detection rules |

| 3. Set ratio bands | Establish minimum and maximum hedge ratios per regime | Dynamic hedge ratio schedule |

| 4. Automate monitoring | Connect to real-time data feeds | Alerts when regime thresholds cross |

| 5. Review and recalibrate | Quarterly effectiveness audit | Updated model parameters |

"The biggest mistake companies make with dynamic hedging is treating it as a set-and-forget upgrade from static models. Dynamic strategies require active monitoring, model recalibration, and clear escalation rules when market signals conflict. Without governance, a dynamic model can generate more churn than protection."

This connects directly to dynamic and advanced FX strategies and explains why strategic risk management approaches must underpin every technical model you deploy.

Implementing these strategies effectively depends enormously on comprehensive governance and clear board-level policy.

Governance, policy, and ongoing verification

You can have the best hedging model in the world and still lose money if the governance structure around it is broken. Policy is not a compliance checkbox. It is the mechanism that prevents a single treasury analyst from making a $50 million directional bet without board awareness.

A complete FX governance framework includes:

- A formal written FX policy ratified by the board, specifying objectives, permitted instruments, maximum exposures, and hedging horizons

- Clear roles: who proposes hedges, who approves them, who executes them, and who audits the outcomes

- Hedge accounting compliance under IFRS 9 or ASC 815, which requires formal designation, effectiveness testing, and documentation at inception

- Defined KPIs: hedge effectiveness ratio, cost of hedging as percentage of exposure, P&L variance attributable to FX, and unhedged exposure as a percentage of revenue

- Quarterly effectiveness audits that compare actual FX impact against the hedged baseline

"Many firms are aware of the governance gap but have not acted. Board-level policy, clear approvals, and hedge accounting compliance are the foundation of every effective FX program, yet they remain the most commonly skipped step."

The reason governance fails is usually organizational, not technical. Treasury teams operate in silos, subsidiaries hedge independently, and the CFO sees aggregated results without visibility into the component exposures. Fixing this requires governance for currency risk that crosses business unit boundaries and reports directly to the board at least quarterly.

Effectiveness audits deserve special attention. A hedge that tests as "highly effective" at inception can drift out of compliance if the underlying exposure changes shape. Reviewing your designated hedging relationships every quarter, not annually, catches these mismatches before they create accounting restatements or tax complications.

What most companies get wrong about forex volatility mitigation

Here is an uncomfortable truth: most corporate FX programs are built backwards. Finance teams reach for derivatives first because they are visible, measurable, and easy to present in a board deck. Operational restructuring is slower, messier, and harder to quantify in a single slide, so it gets deferred indefinitely.

The result is companies that spend heavily on forward and option premiums while leaving large natural hedging opportunities completely untapped. We have seen treasury functions paying six-figure annual hedging costs on exposures that a renegotiated supplier contract would have eliminated at zero cost. The derivative was solving a problem that should not have existed.

The second major error is treating post-trade verification as an administrative burden rather than a source of insight. When a hedge underperforms, most teams close it out and move on without asking why. That lost learning compounds over time. The firms that consistently outperform on FX risk management run post-trade reviews as seriously as pre-trade analysis, using them to recalibrate both models and operational assumptions.

The third mistake is cultural. Currency risk awareness tends to live exclusively in treasury, while the people who actually generate the exposure, salespeople quoting in foreign currencies, procurement teams negotiating overseas contracts, are completely disconnected from the FX consequences of their decisions. Building a culture where commercial teams understand that a price concession in a weak currency is also an FX event is one of the highest-leverage interventions a CFO can make.

Following risk management best practices consistently, and embedding them across the commercial organization rather than keeping them inside treasury, is what separates companies that manage FX risk from those that merely hedge it.

Enhance your forex risk management strategy with CorpHedge

Every framework in this guide requires real-time data, clear exposure visibility, and the ability to model scenarios instantly. That is exactly what CorpHedge is built to deliver.

CorpHedge gives financial managers and CFOs a centralized platform for monitoring live currency positions, running hedging based on Value at Risk models, and executing hedging strategies with full audit trails for governance compliance. Whether you are managing a straightforward forward program or a dynamic regime-switching approach across multiple subsidiaries, the platform adapts to your complexity. Take a product tour to see how the tools map to the strategies outlined above, or explore specific guidance on how to reduce EUR/USD volatility for one of the most actively traded pairs in corporate hedging programs.

Frequently asked questions

What is the most cost-effective way to mitigate forex volatility?

Natural hedging through currency matching, netting, leading and lagging payments, and internal invoicing eliminates exposure at zero cost for predictable cash flows, making it the highest-ROI starting point before any financial instrument is deployed.

How do dynamic hedging strategies improve FX risk management?

Dynamic hedging adjusts ratios continuously based on market conditions, correlations, and realized volatility, outperforming static models especially for unpredictable or volatile currency pairs where fat-tail events are most likely.

Why is governance important in forex volatility mitigation?

Board-level policy, clear approvals, and ongoing hedge accounting compliance ensure that all exposures are identified, approved, and monitored, preventing individual-level decisions from creating uncontrolled directional risk.

When should financial hedges be prioritized over operational hedges?

Financial hedges are most justified for unpredictable, long-duration, or contract-specific exposures where operational restructuring is not feasible. Prioritize natural hedges first at zero cost, then layer financial instruments only where operational alignment cannot close the exposure gap.