TL;DR:

- Market risk, especially FX exposure, affects multinational companies' financial performance daily.

- Effective risk management combines hedging instruments, strong policies, and a risk-aware organizational culture.

- Traditional metrics like VaR have limitations; stress testing and scenario analysis enhance risk assessment.

Currency swings wiped out billions in corporate earnings in recent years, and the trend shows no sign of slowing. For CFOs and risk leaders at international companies, market risk represents the constant threat of losses tied to movements in exchange rates, interest rates, equity prices, and commodity values. When a single quarter's FX move can erase months of operating margin, understanding market risk is not optional. This guide cuts through the noise, clarifies the core concepts, and walks you through practical frameworks and proven mitigation tactics that actually work in a real multinational environment.

Table of Contents

- Defining market risk: What CFOs need to know

- Major types of FX market risk and their practical examples

- Mitigation strategies and financial instruments for FX market risk

- Measuring market risk: Essential metrics and their limitations

- Best practices: Policy design and next-generation market risk management

- A fresh perspective: What most guides miss about market risk

- See how CorpHedge streamlines FX market risk management

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Market risk defined | It refers to losses from market price movements—including FX, interest rates, and commodities. |

| Three FX risk types | Transaction, translation, and economic risk each affect financials and competitiveness differently. |

| Mitigation tools | CFOs can use derivatives and natural hedges to control exposures, rarely covering 100%. |

| Measurement limits | Metrics like VaR are useful but have weaknesses, especially in rare and extreme events. |

| Policy and technology | Dynamic risk frameworks and real-time tools are now essential for effective FX market risk management. |

Defining market risk: What CFOs need to know

Market risk is not a banking problem. That is the first misconception to clear up. Many finance teams at industrial, technology, or consumer goods companies assume market risk belongs on a bank's balance sheet. It does not. Any organization with cross-border revenues, foreign currency payables, or international subsidiaries carries meaningful market risk every single day.

At its core, market risk is the risk of losses in positions arising from movements in market prices or rates. For multinational companies, this plays out across four main categories:

- Foreign exchange (FX) risk: Changes in currency rates affect revenue, costs, and the value of foreign assets.

- Interest rate risk: Shifts in rates alter borrowing costs and the value of fixed-income holdings.

- Equity price risk: Movements in stock prices impact investment portfolios and equity-linked compensation.

- Commodity price risk: Fluctuations in raw material prices squeeze margins for manufacturers and distributors.

For most international companies, FX risk dominates. When your European subsidiary earns euros but reports in dollars, every rate move creates a gap between operational performance and reported results. That gap is market risk in action.

"Market risk is not a theoretical concern. It is the daily reality of running a business across borders, and ignoring it is a strategic choice with real financial consequences."

Market risk exposure in FX positions arises the moment you sign a contract in a foreign currency, open a foreign office, or consolidate a subsidiary's financials. The exposure grows with the size and diversity of your international footprint. Explore the full range of FX risk types to see how each category connects to your specific business model. Understanding where exposure lives is the first step toward knowing how to mitigate FX volatility before it damages your results.

With an understanding of market risk's centrality, let's clarify the types specific to FX exposures.

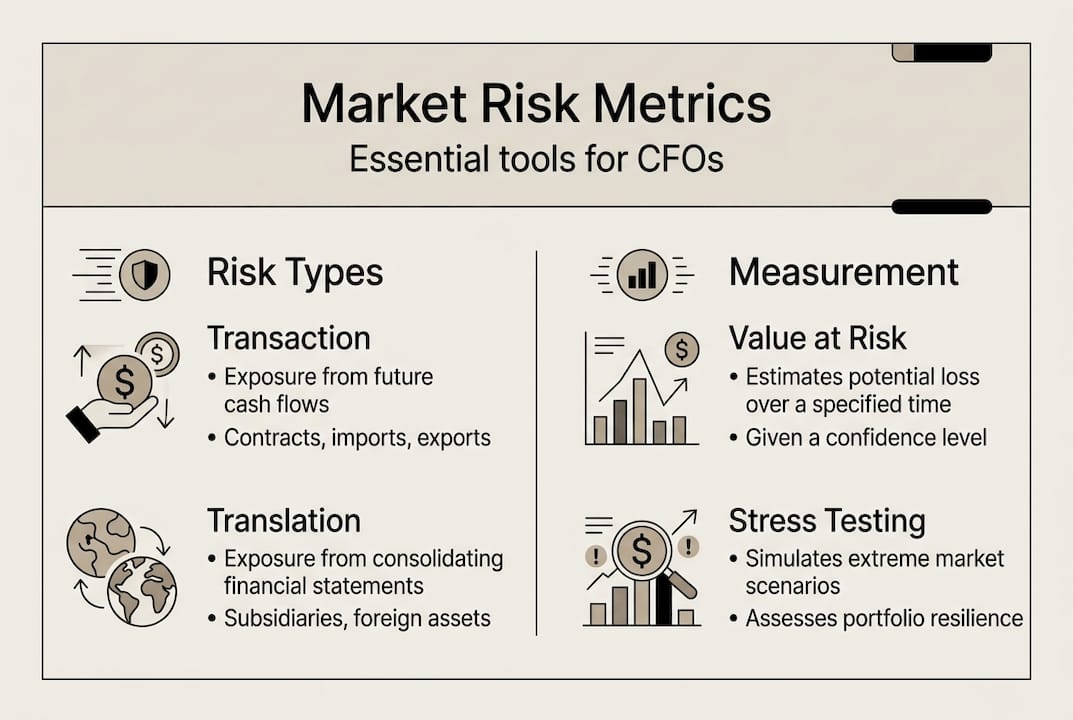

Major types of FX market risk and their practical examples

FX market risk manifests as three distinct categories: transaction risk, translation risk, and economic risk. Each affects a different part of your financial picture and demands a different response.

-

Transaction risk arises when a company has committed to a future payment or receipt in a foreign currency. A U.S. manufacturer that agrees to sell equipment to a German buyer for €5 million, payable in 90 days, is exposed to the euro/dollar rate for that entire period. If the euro weakens 5% before settlement, the company receives $275,000 less than expected.

-

Translation risk hits when you consolidate foreign subsidiaries into your reporting currency. A British subsidiary worth £100 million looks very different on your dollar balance sheet at 1.30 versus 1.20. This does not affect cash directly, but it moves reported equity, earnings per share, and debt ratios in ways that matter to investors and lenders.

-

Economic risk is the most strategic and the hardest to hedge. It reflects how sustained currency shifts alter your competitive position. If the Japanese yen weakens 20% over two years, Japanese competitors can undercut your prices in every shared market, regardless of your hedging program.

| Risk type | What it affects | Time horizon | Hedging approach |

|---|---|---|---|

| Transaction | Cash flows | Short term (days to 12 months) | Forwards, options |

| Translation | Reported financials | Quarterly/annual | Balance sheet hedging |

| Economic | Competitive position | Long term (1 to 5 years) | Strategic, operational |

Pro Tip: Not every exposure deserves equal attention. Assess materiality thresholds by currency pair and risk type. Focus hedging resources where the financial impact is largest and the probability of movement is meaningful. Small exposures in illiquid currencies often cost more to hedge than the risk they carry.

Building a solid grasp of these categories supports smarter decisions around financial risk reduction and helps you prioritize which hedging FX risk strategies deserve budget and management attention.

Mitigation strategies and financial instruments for FX market risk

Once you know where your exposure sits, the next question is how to protect against it. The toolkit for FX market risk mitigation is well established, but choosing the right instrument for the right situation requires judgment.

Derivatives are the most direct tools:

- Forward contracts lock in an exchange rate for a future date. They eliminate uncertainty but also remove the upside if rates move in your favor.

- Options give you the right, but not the obligation, to exchange currency at a set rate. They cost a premium but preserve flexibility.

- Cross-currency swaps exchange principal and interest payments in different currencies, useful for managing long-term balance sheet exposures.

Natural hedging means structuring your business so that foreign currency inflows and outflows offset each other. If your European costs roughly match your European revenues, the net FX exposure is smaller without any derivatives at all.

| Instrument | Cost | Best use case | Protection level |

|---|---|---|---|

| Forward contract | Low | Known future cash flows | High, fixed |

| FX option | Medium to high | Uncertain timing or amount | High, flexible |

| Cross-currency swap | Medium | Long-term balance sheet | High, structural |

| Natural hedge | Operational | Ongoing business flows | Moderate |

Companies typically hedge 70 to 90% of their FX exposure using a combination of these instruments. The exact ratio depends on your risk appetite, the cost of hedging, and the predictability of your cash flows.

Pro Tip: When FX hedging costs spike, as they did after the 2022 rate hike cycle, a blanket 80% hedge ratio may no longer make economic sense. Evaluate partial hedges, layered entry strategies, and dynamic policy adjustment to balance protection with cost efficiency.

Explore the FX risk management tools available to modern treasury teams and review risk management strategies that align with your company's specific exposure profile.

Measuring market risk: Essential metrics and their limitations

You cannot manage what you cannot measure. Value at Risk, or VaR, is the most widely used metric for quantifying market risk. It answers a specific question: what is the maximum loss you would expect over a given time period at a defined confidence level? A one-day 95% VaR of $2 million means there is a 5% chance of losing more than $2 million in a single day.

VaR's appeal is its simplicity. It translates complex, multi-currency exposures into a single number that boards and executives can understand. Most large banks and many multinational corporations use it as a baseline for risk reporting.

But VaR has real limits. VaR ignores tail severity, assumes historical patterns repeat, is non-subadditive in some forms, and consistently underestimates extreme events. In other words, it tells you the threshold but not how bad things get beyond it. During the 2020 COVID shock or the 2022 rate surge, many VaR models were simply wrong.

Common pitfalls in market risk measurement include:

- Relying solely on historical data that does not include recent regime changes

- Using short lookback windows that miss low-frequency, high-severity events

- Treating correlations as stable when they break down exactly when you need them most

- Ignoring liquidity risk, which can make a theoretically hedged position impossible to unwind

Expected Shortfall (ES), also called Conditional VaR, addresses some of these gaps by measuring the average loss beyond the VaR threshold. Stress testing and scenario analysis add further depth, asking "what if" rather than "what is likely."

ESMA data on UCITS funds using absolute VaR approaches shows significant leverage and FX risk concentrations that standard models frequently understate, a warning that applies equally to corporate treasury.

Review hedging best practices to see how leading teams combine VaR with stress testing for a more complete risk picture.

Best practices: Policy design and next-generation market risk management

A strong hedging instrument means nothing without a policy framework that governs when and how you use it. Policy is what separates reactive, ad hoc hedging from a disciplined, repeatable risk management function.

Effective FX risk policy defines hedge ratios by currency and exposure type, sets materiality thresholds, specifies approved instruments, and establishes governance and reporting cadences. It also assigns accountability, making clear who owns the decision to hedge, adjust, or accept risk.

Policy-driven hedging combined with AI and ERP integration enables real-time exposure visibility and dynamic adjustment, a capability that manual spreadsheet processes simply cannot match. Modern treasury platforms connect ERP data, bank feeds, and market rates into a single dashboard, giving your team the information to act before a rate move becomes a loss.

FX hedging costs rose sharply following the post-2022 rate hikes, leading many companies to lower their hedge ratios. That is a rational response, but only if the policy framework explicitly allows for it with clear triggers and limits.

Here is a practical sequence for staying agile:

- Review your hedge policy at least quarterly, not just annually.

- Integrate exposure data from ERP systems to eliminate manual reporting gaps.

- Run scenario analysis on your top three currency pairs before each board cycle.

- Align treasury, accounting, and business unit leaders on materiality and risk appetite.

- Document every policy exception so you can learn from it.

Pro Tip: Treat your FX policy as a living document. As rates, costs, and business priorities shift, a static policy becomes a liability. Build in a formal review trigger tied to market volatility thresholds.

See how leading companies approach corporate FX risk management and apply hedging best practices that scale with your organization.

A fresh perspective: What most guides miss about market risk

Here is the uncomfortable truth: most CFOs who suffer significant FX losses were not undone by a lack of hedging tools. They were undone by organizational blind spots.

The real risk is not in the instruments you chose or the hedge ratio you set. It is in the assumptions your team never questioned, the scenario that nobody modeled because it seemed too unlikely, and the cross-functional communication that broke down between treasury and the business units that actually generate the exposures.

World-class derivatives programs have failed because the people running them stopped asking hard questions. Static strategies, no matter how technically sound, decay as markets evolve. The companies that consistently manage market risk well invest as much in building a risk-aware culture as they do in technology and derivatives. They run regular scenario workshops, challenge their own assumptions, and treat treasury as a strategic partner rather than a back-office function.

Adaptive leadership consistently outperforms static strategy. The ability to mitigate FX volatility over time comes from people who stay curious, not just from platforms that stay current.

Pro Tip: Invest as much in people and cross-team collaboration as in technology and derivatives. A well-informed business unit leader who flags an emerging exposure early is worth more than any single hedging instrument.

See how CorpHedge streamlines FX market risk management

For leaders ready to move from frameworks to action, CorpHedge provides the technology infrastructure that makes disciplined FX risk management practical at scale. The platform delivers real-time exposure visibility, VaR-based strategy modeling, and dynamic hedging tools built specifically for the needs of international treasury teams.

Explore the full product tour to see how CorpHedge connects your exposure data, hedging instruments, and reporting in one place. Book a CorpHedge demo tour to walk through live scenarios with your own numbers. You can also review the complete set of FX risk features to match platform capabilities to your specific risk management priorities.

Frequently asked questions

What are the three main types of FX market risk?

Transaction, translation, and economic risk are the three main FX market risks for international firms, each affecting a different part of the financial picture.

How do companies typically mitigate market risk?

Companies use forwards, options, swaps, and natural hedging strategies, with hedge ratios typically 70 to 90% of total FX exposure depending on risk appetite and cost.

What are the weaknesses of Value at Risk (VaR)?

VaR underestimates extreme losses, assumes historical patterns hold, and fails to capture the severity of tail events or black swan scenarios.

How are FX hedge ratios determined?

Hedge ratios balance risk reduction with cost and opportunity, and are often adjusted downward when hedging costs rise sharply, as seen after the post-2022 rate hike cycle.

Recommended

- Corporate FX risk explained: Mitigate volatility and boost profits

- FX risk types: Key exposures and mitigation strategies

- Corporate risk governance: Currency risk strategies 2026

- Effective financial risk reduction strategies for currency exposure

- Top crypto risk management tips: AI insights for safer trading