TL;DR:

- Foreign exchange volatility now poses a direct threat to corporate earnings, requiring proactive risk management strategies.

- Most CFOs underestimate the complexity of FX exposures, which include transactional, translational, and economic risks that demand tailored responses.

- Effective governance, adaptable hedging approaches, and strategic instrument selection enable firms to protect margins and turn FX risk into a competitive advantage.

Foreign exchange volatility is no longer a background noise problem. It is a direct threat to earnings, and the firms still treating it as secondary are paying a steep price. Unhedged FX losses are pushing companies back to the hedging table, with US corporates reporting average losses of $9.85 million in 2025 alone. This guide cuts through the noise and delivers a structured, practical roadmap for CFOs who want to move from reactive damage control to a proactive, intelligent FX risk framework that actually protects margins.

Table of Contents

- Understanding your company's FX risk profile

- Choosing between static and dynamic hedging strategies

- Instrument selection: forwards vs. options and hybrid approaches

- Establishing effective governance and performance monitoring

- Why most CFOs underestimate the complexity—and opportunity—of FX risk management

- Take your FX risk strategy to the next level

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Partial hedging is risky | Most international firms hedge less than half of their FX exposure, leading to significant losses when markets move. |

| Dynamic strategies prevail | Layered and adaptive hedging is increasingly used over static approaches, especially as central bank policies diverge. |

| Instrument fit is crucial | Match hedging tools—like forwards or options—to your firm’s exposures and risk appetite to optimize results. |

| Monitor and adapt policies | Strong governance and regular performance review ensure FX risk management remains effective as markets shift. |

| FX risk can be an asset | CFOs who proactively manage FX risk gain both protection and potential competitive advantage. |

Understanding your company's FX risk profile

Now that we've set the context for just how real and costly FX risk can be, let's break down the building blocks: the types of FX exposures every CFO must understand.

Most CFOs can name transactional risk without hesitation. But stopping there is exactly where things go wrong. There are three distinct layers of key FX risk types that your organization is exposed to, and each demands a different response.

Transactional risk arises from foreign currency receivables and payables. If you invoice a European client in euros and the dollar strengthens before payment, the value you receive in your functional currency shrinks. This is the most visible exposure and the one most teams try to hedge first.

Translational risk affects companies with overseas subsidiaries. When you consolidate financial statements, fluctuating exchange rates distort the reported value of foreign assets, liabilities, and earnings, even if no actual cash changes hands. Many CFOs underestimate how badly translational losses erode balance sheet strength and investor confidence.

Economic risk is the most subtle and the most dangerous long-term. It reflects how currency movements shift your competitive position relative to foreign rivals. If a competitor manufactures in a country with a weakening currency, their export prices fall in your target market even if your own costs hold steady. You lose ground without doing anything wrong.

Here's where the data gets sobering. Survey evidence shows that average hedge ratios remain below 50% for many corporates, meaning that most firms are knowingly leaving substantial exposure on the table. Some do this intentionally to preserve upside. Many others simply lack the tools or governance to measure their full exposure accurately.

Key questions to ask when building your FX risk profile:

- What percentage of revenues and costs are denominated in foreign currencies?

- Do you have subsidiaries reporting in non-functional currencies?

- How much of your competitive pricing is affected by competitors' home currency movements?

- What is your current hedge ratio, and how was that number chosen?

- Are you tracking indirect exposures, such as commodity inputs priced in USD?

Understanding market risk essentials is not optional for modern CFOs. Without a complete picture of exposure, any hedging program is essentially a guess, and expensive guesses have real consequences for shareholders.

Pro Tip: Run a currency sensitivity analysis annually or after major business model shifts. Map each revenue and cost stream to its currency, then stress-test what a 10% move in your three largest currency pairs would do to operating income. That single exercise will reveal gaps most treasury teams overlook.

Choosing between static and dynamic hedging strategies

Once exposure is assessed, the next challenge is designing a hedging approach. This is where choosing between static and dynamic strategies becomes pivotal.

Static hedging, sometimes called "set-and-forget," involves locking in a fixed hedge ratio, say 75% of forecasted exposure, for a defined period using rolling forward contracts. It's simple to implement, easy to audit, and works reasonably well in stable macro environments. For smaller treasury teams without dedicated FX analysts, static programs offer predictability and lower operational overhead.

Dynamic hedging, by contrast, adapts continuously. Layered or rolling structures allow treasuries to build hedges incrementally over time, adjusting the ratio and tenor based on market conditions, rate differentials, and updated cash flow forecasts. When interest-rate differentials diverge sharply across central banks, as they have in 2025 and 2026, the carry cost of a static hedge can erode significant value. Dynamic approaches let you manage both entry timing and P&L volatility more precisely.

| Feature | Static hedging | Dynamic hedging |

|---|---|---|

| Complexity | Low | Medium to high |

| Cost | Predictable | Variable, often lower carry cost |

| Flexibility | Low | High |

| Best for | Stable, predictable cash flows | Volatile markets, complex exposures |

| Governance requirement | Moderate | High |

| Accounting treatment | Simpler | Requires careful documentation |

The choice between these approaches is not purely a technical one. It is deeply tied to your accounting framework, your board's risk appetite, and the sophistication of your treasury team. Hedge accounting under IFRS 9 or ASC 815 requires rigorous documentation regardless of approach, but dynamic strategies demand more frequent reassessment of hedge effectiveness.

"Treasury teams moving away from set-and-forget hedging toward layering and rolling structures are doing so to manage entry timing and carry or P&L volatility more effectively, especially when macroeconomic conditions are shifting fast." This reflects a broader recognition that currency vs market risk cannot be managed with one-size-fits-all tools.

Consider these factors when deciding between approaches:

- Forecast reliability: If your cash flows are highly predictable, static hedging works well. If revenues are seasonal or contract-dependent, dynamic layering gives more control.

- Carry cost sensitivity: In high-rate-differential environments, static forwards can lock in unfavorable carry. Dynamic structures let you time entries more strategically.

- Team capacity: Dynamic programs require more monitoring and decision-making bandwidth. Ensure your treasury team or external platform can handle the cadence.

Pro Tip: A layered approach doesn't mean constant trading. Even dividing your hedge into three tranches, placed one month apart, smooths entry timing and reduces the risk of locking in at a single adverse rate. This small structural change can meaningfully reduce carry costs over a year while maintaining strong coverage. Explore mitigating forex volatility techniques to refine this further.

Instrument selection: forwards vs. options and hybrid approaches

Having compared strategic approaches, let's examine specific hedging instruments and how to tailor them to your company's needs.

The instrument question is where theory meets reality fast. Two companies with identical FX exposure can reasonably choose completely different instruments based on their cash flow certainty, premium budget, and risk tolerance.

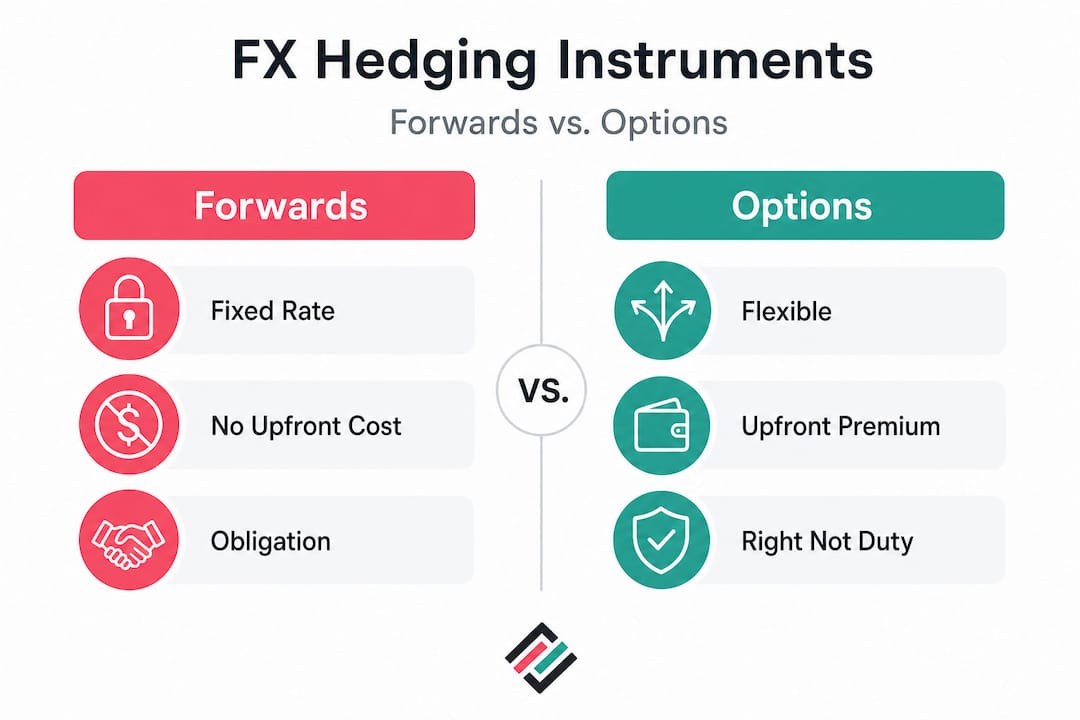

Forward contracts are the workhorse of corporate FX hedging. You agree today to exchange a set amount of currency at a set rate on a future date. There's no premium to pay upfront. The rate is locked in, and the uncertainty disappears from your income statement. For companies with highly predictable, contractually fixed foreign currency flows, forwards are often the most cost-effective and operationally simple choice.

Options give you the right, but not the obligation, to exchange currency at a specified rate. If the market moves in your favor, you let the option expire and transact at the better market rate. If the market moves against you, you exercise the option and limit your loss. That flexibility has a price: the premium you pay upfront, which goes to the counterparty regardless of outcome.

As a general rule, hedging instruments should be matched to your exposure timing and risk preferences. Forwards suit known cash flows. Options suit environments where you want to preserve upside or protect against asymmetric outcomes without completely surrendering your ability to benefit from favorable moves.

| Instrument | Upside potential | Downside protection | Upfront cost | Complexity |

|---|---|---|---|---|

| Forward contract | None | Full | None | Low |

| Vanilla option | Full | Full | Premium | Medium |

| Participating forward | Partial | Full | Low/none | Medium |

| Collar | Partial (capped) | Full | Low/none | Medium-high |

| Range accrual | Conditional | Conditional | Variable | High |

Hybrid structures like participating forwards and collars sit between forwards and plain options. A collar, for example, caps your downside while giving up gains beyond a defined level. A participating forward lets you benefit from a portion of favorable moves while still providing protection. These structures can be built to have zero net premium, making them attractive for cost-conscious organizations.

Here's a sequential process for matching instruments to exposure:

- Identify the nature of the exposure: is it fixed, forecast-based, or contingent?

- Assess your premium budget: how much can you allocate to option costs this quarter?

- Define your primary objective: certainty of rate, upside preservation, or cost minimization?

- Review accounting implications: will the structure qualify for hedge accounting treatment?

- Compare at least three instrument structures with your bank or platform before committing.

Pro Tip: For contingent exposures, such as a deal that may or may not close, never use a forward. You'd be obligated to deliver currency on a transaction that might not materialize. A vanilla option or a structured contingent forward protects you without creating a synthetic liability. Learn more about international transaction hedging for deal-specific guidance. Also review currency fluctuation best practices to build institutional knowledge across your finance team.

Establishing effective governance and performance monitoring

Selecting instruments is crucial, but without strong oversight and continuous adaptation, even the best-laid plans can fall short. Let's see what effective governance looks like.

A hedging program without a policy is not a program. It's a collection of individual decisions made under pressure, and that's where costly inconsistencies creep in. A board-approved FX risk policy is the foundation of everything else.

Your policy should define: the scope of currencies and exposures covered, minimum and maximum hedge ratios, approved instruments and counterparties, delegated authority levels, hedge accounting election and documentation requirements, and review frequency. Without these parameters, your treasury team has no clear mandate and no protection when markets move against them.

Key elements of a robust governance framework:

- Clear ownership: Assign a named individual or committee accountable for FX risk decisions. In most organizations this is the treasurer or CFO, with board oversight for decisions above a defined threshold.

- Tiered authorization: Smaller hedges might be executed at the treasurer level; larger or more complex structures require CFO sign-off or audit committee awareness.

- Performance benchmarking: Compare actual hedge outcomes against a defined benchmark, such as the unhedged rate or a systematic hedging baseline, not just against "did we make money?"

- Regular policy reviews: Survey data shows that reported losses and preparedness perceptions are directly influencing planned changes in hedge ratios and tenors. Build a formal annual policy review into your calendar, and trigger an ad hoc review after any material loss event.

Must-have metrics for senior management reporting:

- Current hedge ratio by currency pair and tenor bucket

- Mark-to-market value of open hedge positions

- Hedge effectiveness ratio under IFRS 9 or ASC 815

- FX impact on reported EBIT vs. prior period

- Variance between forecasted and actual hedged exposure

Pro Tip: Don't benchmark your hedging program purely on whether it "made money." A hedge that cost you $2 million in foregone upside but prevented a $15 million downside loss was a success. Frame performance reporting around risk reduction relative to your policy objectives, not trading P&L. Explore FX risk reduction strategies and review FX risk management basics to build reporting templates your board will actually understand.

Why most CFOs underestimate the complexity—and opportunity—of FX risk management

With the mechanics in place, it's time for a hard-won perspective on what really separates leading FX risk managers from the rest.

Here's something most finance publications won't say plainly: most CFOs treat FX hedging as a defensive chore, something you do to avoid getting called out on an earnings call. That framing keeps them permanently behind the curve.

The firms we see consistently outperform on FX are not the ones with the most elaborate models. They are the ones that have internalized FX risk as a strategic variable, not a treasury nuisance. When currency dynamics are integrated into pricing strategy, supplier negotiations, market entry decisions, and capital allocation, the treasury function stops being a cost center and starts generating real competitive advantage.

Consider what happens when a CFO proactively extends hedge tenor during a period of favorable rates and low implied volatility. They lock in cost certainty for 18 to 24 months. That certainty allows the commercial team to offer more competitive pricing in foreign markets, win contracts that less-hedged competitors cannot afford to price aggressively, and grow market share during exactly the periods when rivals are most exposed. That's not risk management. That's offense.

The uncomfortable truth is that overly rigid programs are almost as dangerous as having no program at all. We've seen companies with 100% static hedge ratios get burned by accounting mismatches when underlying exposures changed and hedges couldn't be unwound economically. Rigidity creates its own form of risk.

Adaptability, honest post-loss reviews, and a willingness to challenge your own policy assumptions annually separate the firms that lead from those that just react. And the firms that truly lead use advanced profit protection strategies not as a last resort, but as a systematic part of how they plan and compete globally.

Take your FX risk strategy to the next level

For CFOs inspired to turn insights into outcomes, CorpHedge offers powerful resources and expert support to build and execute world-class FX risk programs.

Managing FX risk at the level this guide describes requires more than spreadsheets and bank calls. It requires real-time visibility into your currency positions, systematic application of Value at Risk methodologies, and the ability to model and execute hedging strategies without friction. That's exactly what CorpHedge was built to deliver.

With CorpHedge, you can apply Value at Risk hedging frameworks directly to your exposure data, giving your team a quantified, defensible basis for every hedging decision you bring to the board. The platform's FX exposure management features give you live position monitoring, strategy execution tools, and integration capabilities designed for international finance teams. Ready to see it in action? Take a FX risk product tour and discover how leading CFOs are building smarter, more adaptive hedging programs today.

Frequently asked questions

What is the typical hedge ratio CFOs use for FX risk?

Surveys show average hedge ratios were approximately 49% in Q4 2025, meaning most firms only partially cover their foreign currency exposure and carry meaningful unhedged risk.

How do static and dynamic hedging differ in practice?

Static hedging sets fixed ratios and tenors in advance, while dynamic or layered approaches continuously adjust strategy based on evolving market conditions, carry costs, and updated exposure forecasts.

When should a CFO choose options over forwards for FX hedging?

CFOs use options when they want to preserve upside potential or limit downside within defined bands. As noted, options vs. forwards differ primarily in that options carry a premium cost but offer asymmetric protection that forwards cannot provide.

Why do so many companies still suffer major FX losses?

Most firms underhedge or rely on static programs that cannot adapt to shifting macro conditions. Reported average losses of $9.85 million for US corporates in 2025 reflect the real cost of leaving exposure unmanaged or undermanaged.