TL;DR:

- Many companies underestimate currency risk, leading to significant margin erosion.

- Proper differentiation between currency and market risk is essential for effective mitigation.

- Combining quantitative risk measurement with operational strategies enhances currency risk management.

Global corporations lose billions annually to currency volatility, yet many finance teams still treat FX exposure as a footnote rather than a strategic threat. When Volkswagen reported a €1.5 billion FX loss in a single fiscal year, it wasn't ignorance of risk that caused the damage. It was the failure to distinguish currency risk from broader market risk and apply the right mitigation tools to each. This guide clarifies the definitions, shows how each risk materializes across international operations, and gives you actionable frameworks to protect margins and cash flows.

Table of Contents

- Understanding currency risk and market risk

- Types, exposures, and how risks materialize

- Risk measurement: frameworks and methodologies

- Mitigation strategies: hedging, diversification, and beyond

- Nuances, challenges, and expert insights

- What most guides overlook about currency and market risk

- How CorpHedge helps CFOs mitigate currency and market risk

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Currency vs market risk | Currency risk is a specific category within market risk, demanding tailored management for global companies. |

| Diverse risk exposures | Transaction, translation, and economic exposures each present unique challenges for international firms. |

| Measuring risk effectively | Robust frameworks like VaR help quantify potential losses but must be paired with scenario planning. |

| Strategic risk mitigation | A combination of hedging, diversification, and operational tactics best reduces overall risk. |

| Nuance in real-world execution | Unexpected events and cost-benefit tradeoffs require flexibility and ongoing risk awareness. |

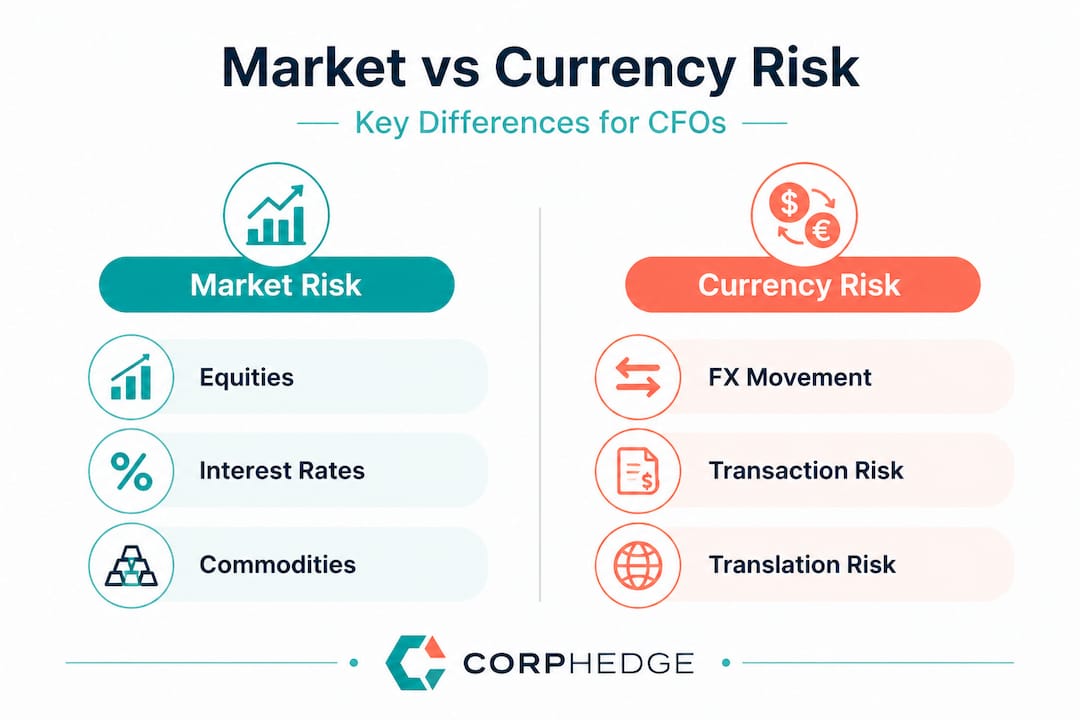

Understanding currency risk and market risk

These two terms get used interchangeably, but treating them as identical is a costly mistake. Currency risk is the risk of losses due to adverse changes in exchange rates affecting transactions, translations, or economic value in international operations. It is specific, measurable, and directly tied to the currencies your company earns, pays, or reports in.

Market risk, by contrast, is the risk of losses from adverse movements in market prices or rates, including equities, interest rates, commodities, and currency as a sub-component. Currency risk lives inside market risk, but it has its own exposure profile and demands dedicated management.

| Dimension | Currency risk | Market risk |

|---|---|---|

| Scope | Exchange rate movements | All financial market price movements |

| Sources | FX rates, cross-border flows | Equities, rates, commodities, FX |

| Typical impact | Revenue, margins, balance sheet translation | Portfolio value, cost of capital |

| Examples | EUR/USD shift hurts USD revenues | Rising rates increase debt costs |

Key exposures to track across both categories:

- Currency risk: transactional (contractual cash flows), translational (financial statement restatement), economic (competitive position over time)

- Market risk: equity price volatility, interest rate shifts, commodity price swings, and FX movements

"Currency risk is a subset of market risk, but it demands dedicated strategies. Lumping them together means your hedging program will have dangerous blind spots."

For a deeper breakdown of exposure categories, the types of currency risk framework provides a practical starting point.

Types, exposures, and how risks materialize

Now that we've established definitions and broad categories, let's go deeper into exactly how these risks take root in an international enterprise.

Currency risk types break into three distinct forms: transactional risk (contractual cash flows exposed to rate changes before settlement), translational risk (consolidating foreign subsidiary financials into the parent's reporting currency), and economic risk (long-term competitive position affected by sustained exchange rate shifts). Each hits the P&L differently.

Market risk components include equity volatility, interest rate changes, commodity prices, and FX movements, all of which are interconnected in global operations. A spike in commodity prices can simultaneously compress margins and trigger currency outflows in procurement-heavy industries.

| Risk scenario | Industry example | Financial impact |

|---|---|---|

| Transactional: USD weakens post-contract | US exporter with EUR receivables | Revenue shortfall on settlement |

| Translational: GBP depreciates | UK subsidiary of US parent | Lower consolidated revenue in USD |

| Economic: JPY strengthens long-term | Japanese auto exporter | Lost price competitiveness vs. rivals |

| Interest rate spike | Capital-intensive manufacturer | Higher refinancing costs |

| Commodity price surge | Airline or chemical company | Input cost overrun |

Here is the threat path from exposure to P&L damage:

- A cross-border contract is signed in a foreign currency.

- The exchange rate moves adversely before settlement.

- The realized cash flow falls short of the projected amount.

- The shortfall flows directly into operating income.

- Repeated across multiple contracts, it becomes a structural margin problem.

Pro Tip: Transactional risk is the most common exposure CFOs underestimate because it hides in individual contracts. By the time the aggregate effect appears in quarterly results, months of margin erosion have already occurred. Build a forward-looking contract register that flags FX exposure at the point of deal origination, not at settlement.

Implementing risk reduction strategies early in the contract lifecycle is far cheaper than hedging reactively after exposure has accumulated.

Risk measurement: frameworks and methodologies

Understanding exactly how to measure and quantify these risks is critical before you can effectively manage or mitigate them.

The three standard measurement approaches for both currency and market risk are VaR methodologies: parametric (assumes normal distribution, fast but sensitive to assumptions), historical simulation (uses actual past data, more realistic but backward-looking), and Monte Carlo simulation (generates thousands of scenarios, most flexible but computationally intensive).

Here is when each approach fits best:

- Parametric VaR: Best for liquid, normally distributed exposures where speed matters. Common in daily treasury reporting.

- Historical simulation VaR: Best when you have rich historical data and want to capture real market behavior, including past crises.

- Monte Carlo simulation: Best for complex, nonlinear portfolios with options or structured instruments where scenario breadth matters most.

Every model has limits. VaR tells you the loss threshold you won't exceed 95% or 99% of the time. It says nothing about the severity of losses in that remaining 1% to 5%, which is precisely where catastrophic events live. Black swan events, sudden regime changes, and correlated asset collapses all fall outside standard VaR assumptions.

Pro Tip: Historical simulation can give you false confidence during stable periods. If your lookback window doesn't include a major crisis or a sudden currency regime shift, your model will systematically underestimate tail risk. Supplement historical VaR with scenario analysis built around plausible but extreme events, not just what has happened before.

Hedging based on VaR allows you to set exposure limits that are grounded in quantitative evidence rather than intuition, making the case to the board far more defensible.

Mitigation strategies: hedging, diversification, and beyond

With the ability to gauge risk exposure quantitatively, the next step is deploying practical strategies to contain it.

Core mitigation tools available to international finance teams:

- Forward contracts: Lock in exchange rates for future transactions, eliminating uncertainty but also capping upside.

- Currency options: Provide asymmetric protection. You pay a premium but retain the ability to benefit if rates move favorably.

- Cross-currency swaps: Exchange principal and interest payments in different currencies, ideal for long-term debt or intercompany funding structures.

- Natural hedging: Match revenue and cost currencies operationally. A US company manufacturing in Europe and selling in Europe naturally offsets EUR exposure.

- Netting: Consolidate intercompany payables and receivables to reduce gross FX flows before hedging the net position.

- Diversification: Spread market risk across asset classes, geographies, and instruments to reduce correlated losses.

Empirical data supports the value of these tools. Hedging instruments research shows futures basis risk at 5.9%, options delivering a 68% reduction in premium costs under optimized structures, swaps cutting volatility by 41%, and dynamic loan hedging reducing FX beta by 30.5% in documented cases like SolarTech.

Statistic callout: Dynamic hedging strategies reduced FX-driven earnings volatility by up to 41% in recent empirical studies, with options-based programs outperforming static forward-only approaches in volatile markets.

The cost and tradeoff reality matters here. Forwards and swaps eliminate downside but also eliminate upside. Options preserve upside but carry premium costs that compound across a large hedging portfolio. Diversification and VaR limits reduce market risk broadly but don't substitute for instrument-level FX hedging.

Pro Tip: Hybrid hedging works best for companies with both short-term transactional exposure and long-term economic exposure. Use forwards to lock near-term cash flows, and layer options on top for medium-term exposures where rate direction is uncertain. This avoids over-hedging while keeping downside contained.

Explore currency risk management strategies and hedging international transactions to build a program that matches your exposure profile.

Nuances, challenges, and expert insights

Despite robust frameworks and tools, experienced organizations know that the real world rarely follows the script.

Advanced pitfalls and considerations that catch even sophisticated teams off guard:

- Hedging costs vs. upside: Over-hedging locks in losses when rates move favorably, creating opportunity cost that boards increasingly scrutinize.

- Options flexibility vs. premium drag: Options are theoretically ideal but can become expensive in high-volatility environments, precisely when you need them most.

- Regime change risk: Sudden FX moves, like the Swiss franc unpeg in 2015, can instantly invalidate hedges structured around stable rate assumptions. Options provide more flexibility than forwards in these scenarios.

- Natural hedging operational complexity: Matching currency inflows and outflows requires coordination across procurement, sales, and treasury, which is harder than it sounds in decentralized organizations.

- Model over-reliance: Teams that trust VaR outputs without stress testing them against non-historical scenarios are building risk programs on fragile foundations.

"Some argue currency risk is fully diversifiable across a global portfolio. In practice, correlated FX moves during crises mean diversification provides far less protection than models predict. Dedicated hedging programs remain essential."

The most resilient companies reduce currency risk by combining instrument-level hedging with operational flexibility, giving them multiple levers to pull when markets move unexpectedly. A strategic risk management mindset treats hedging as a continuous process, not a quarterly exercise.

What most guides overlook about currency and market risk

Pulling together these frameworks and tactics, here is what years at the sharp end of international finance have proven matters most.

Most risk guides present currency and market risk as parallel problems requiring parallel solutions. The reality is messier. Currency risk has operational roots that pure market risk does not. A shift in EUR/USD doesn't just change portfolio values. It changes competitive dynamics, customer pricing power, and supplier relationships simultaneously. Treating it as just another market variable misses the strategic dimension entirely.

The second overlooked truth is that model precision is often the enemy of practical flexibility. Organizations that invest heavily in refining their VaR models to four decimal points sometimes neglect the far more valuable work of building scenario-based contingency plans. When the Swiss franc unpegged in 2015, no model predicted it. Companies with pre-built response playbooks recovered faster than those relying solely on quantitative precision.

Hybrid hedging and continuous re-evaluation aren't just best practices. They are the difference between a hedging program that protects the business and one that creates a false sense of security. Advanced FX hedging strategies that incorporate dynamic rebalancing consistently outperform static programs over multi-year horizons.

Pro Tip: Build organization-wide risk awareness by including commercial and operational teams in FX exposure reviews. Sales teams signing contracts in foreign currencies and procurement teams sourcing internationally are creating exposure daily. Catching it at the source is always cheaper than hedging it downstream.

How CorpHedge helps CFOs mitigate currency and market risk

For CFOs determined to operationalize these best practices and protect international margins, specialized expertise and platforms can provide a critical edge.

CorpHedge is built specifically for finance professionals managing real FX exposure in global operations. The platform combines hedging based on value at risk with real-time currency position monitoring, giving your team the quantitative foundation to make defensible hedging decisions fast.

Beyond the tools, CorpHedge offers a demo tour that walks your team through the full risk management workflow, from exposure identification to instrument selection and reporting. For teams building internal capability, the FX hedging course at the Learning Academy provides structured training grounded in real-world scenarios. Whether you are refining an existing program or building one from scratch, CorpHedge gives you the infrastructure to act on what you've learned here.

Frequently asked questions

What is the main difference between currency risk and market risk?

Currency risk is specific to fluctuations in exchange rates, while market risk covers all financial market movements including equities, interest rates, commodities, and currencies together.

How do companies typically hedge currency risk?

Companies use forwards, options, swaps, netting, and natural hedging to reduce exposure, with the right mix depending on the duration and nature of the underlying exposure.

What is Value at Risk (VaR) and why is it important?

VaR measures the potential loss in value of a portfolio over a defined period, and VaR methodologies like parametric, historical, and Monte Carlo simulation help quantify both currency and broader market risk for hedging decisions.

Are natural hedges always cost-free?

Natural hedging avoids direct financial cost, but matching inflows and outflows operationally often requires significant coordination across business units and may constrain commercial flexibility.

Can currency risk be completely eliminated?

Currency risk can be substantially reduced but not fully eliminated, because sudden FX regime shifts like the Swiss franc unpeg can override even well-structured hedging programs.