TL;DR:

- Misapplying IAS 21 and IFRS 9 creates reporting errors, compliance risks, and earnings volatility that can erode investor confidence.

- Separating translation and hedge accounting standards and maintaining proper documentation is crucial for accurate financial reporting and strategic decision-making.

Misapplying IAS 21 and IFRS 9 is not a theoretical risk. It is a live one. When international finance teams conflate translation accounting with hedge accounting, the result shows up as reporting errors, compliance gaps, and earnings volatility that erodes investor confidence. The accounting framework governing foreign exchange is precise by design, yet the boundary between these two standards trips up even experienced CFOs. This guide cuts through the confusion, gives you a clear map of where each standard applies, and shows how to connect accounting discipline to real FX risk outcomes.

Table of Contents

- Understanding the essentials of FX accounting standards

- Comparing translation vs. hedge accounting: Where do most companies go wrong?

- Net investment hedges and complex scenarios: Getting beyond the basics

- Integrating hedge accounting with modern FX risk solutions

- Non-GAAP performance measures and the impact of FX: Navigating SEC scrutiny

- A practitioner's perspective: Why getting FX accounting right delivers real strategic value

- Discover advanced FX risk management with CorpHedge

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Distinguish standards | Accurately separate the use of IAS 21 for FX transactions/translation and IFRS 9 for hedge accounting. |

| Prevent common errors | Avoid mixing translation and hedge accounting rules to reduce misstatements and compliance risks. |

| Address advanced scenarios | Apply the right approaches for net investment hedges and hyperinflationary economies. |

| Enhance transparency | Disclose FX impacts clearly in non-GAAP reporting for regulator and investor confidence. |

| Leverage technology | Use tools and analytics to optimize hedge effectiveness and FX risk reporting at scale. |

Understanding the essentials of FX accounting standards

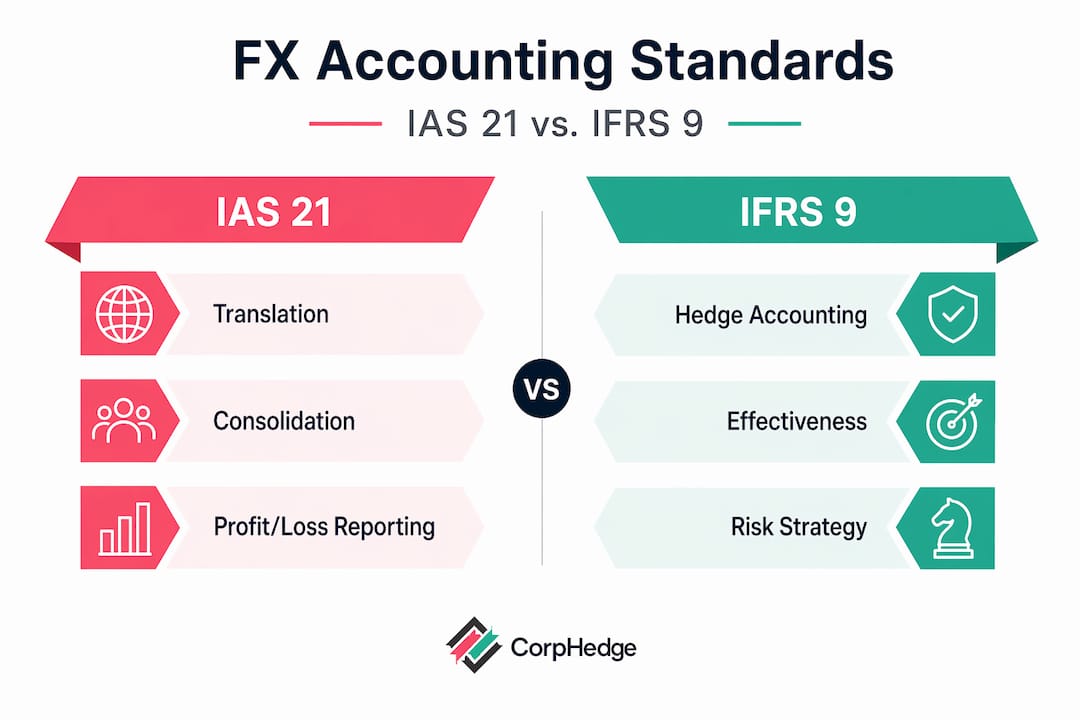

Two standards govern most of what international companies do with foreign currencies, and they do not overlap. IAS 21 covers the translation of individual foreign-currency transactions and the consolidation of foreign operations into a group's presentation currency. IFRS 9 handles hedge accounting. Knowing which engine to use for which job is the first discipline of sound FX accounting.

Under IAS 21, transactions are recorded at the spot rate on the transaction date. At settlement, any exchange difference lands in profit or loss. That is clean and mechanical. Where it gets complicated is in consolidated financial statements, where exchange differences from translating foreign operations sit in other comprehensive income (OCI) rather than flowing through earnings.

The critical boundary: IAS 21 does not apply to hedge accounting of foreign currency items. IFRS 9 does. Companies that attempt to apply IAS 21 logic to hedging relationships create errors that auditors and regulators will find.

"IAS 21 does not apply to hedge accounting of foreign currency items (including hedging a net investment); IFRS 9 applies to hedge accounting."

Key distinctions at a glance:

| Area | IAS 21 | IFRS 9 |

|---|---|---|

| Scope | Transaction translation, foreign operations | Hedge accounting relationships |

| FX gain/loss location | Profit or loss (transactions); OCI (consolidation) | OCI or P&L depending on hedge type |

| Documentation required | No | Yes, at inception |

| Derivatives covered | No | Yes |

- IAS 21 applies from the moment a foreign-currency invoice is raised to the point of settlement.

- IFRS 9 kicks in when you formally designate a hedging relationship with a qualifying instrument.

- Confusing the two is the most common source of FX reporting restatements in multinational groups.

Pro Tip: Map every FX exposure in your group to either IAS 21 or IFRS 9 before your next close cycle. If a team member cannot answer which standard governs a specific exposure, that is a training gap with real financial reporting risk attached to it. Understanding global FX accounting basics is the prerequisite for everything that follows.

Comparing translation vs. hedge accounting: Where do most companies go wrong?

Translation and hedge accounting serve different purposes. Translation under IAS 21 is about presenting foreign operations in a common currency for consolidated reporting. Hedge accounting under IFRS 9 is about reducing earnings volatility by matching the timing of gains and losses on a hedging instrument with the exposure it is protecting.

Translation of foreign operations uses the closing rate for balance sheet items and average or transaction-date rates for income and expenses. Exchange differences go to OCI and accumulate in a separate equity reserve until the foreign operation is disposed of. No designation. No documentation. It is automatic.

Hedge accounting is the opposite of automatic. Under IFRS 9, you must formally designate the hedge, document the relationship at inception, identify the risk being hedged, and demonstrate ongoing effectiveness. Many groups try to shortcut this by relying on translation mechanics to "absorb" FX volatility. It does not work, and it creates strategic risk management blind spots.

"Treat translation accounting (IAS 21) and hedge accounting (IFRS 9) as separate 'engines'; many implementation errors arise when FX hedges are mistakenly accounted for under IAS 21 instead of designating qualifying hedge relationships under IFRS 9."

Side-by-side comparison:

| Feature | Translation (IAS 21) | Hedge accounting (IFRS 9) |

|---|---|---|

| Purpose | Consolidation presentation | Earnings volatility reduction |

| Designation needed | No | Yes |

| Instruments used | N/A | Derivatives, some non-derivatives |

| OCI treatment | Automatic translation reserve | Designated cash flow or net investment hedge |

| Disposal impact | Reclassify to P&L | Reclassify per IFRS 9 rules |

The most frequent implementation errors:

- Booking forward contract gains and losses under IAS 21 rules instead of designating them as IFRS 9 hedges.

- Assuming that because a subsidiary is translated at closing rates, the FX risk is "hedged" for accounting purposes.

- Failing to document hedge effectiveness testing methods at inception, which disqualifies the entire relationship.

- Applying average rates to balance sheet items, which is an IAS 21 error that distorts net assets.

For mitigating FX volatility in practice, the separation of these two frameworks is not just a compliance requirement. It is the foundation of accurate performance measurement. Companies operating across Poland, Sweden, and other markets with distinct functional currencies face this challenge at every reporting cycle. You can also review foreign subsidiary translation practices for regional context.

Net investment hedges and complex scenarios: Getting beyond the basics

Net investment hedges are where the two standards intersect most directly, and where the accounting gets genuinely difficult. A net investment hedge protects the group's equity exposure in a foreign subsidiary against exchange rate movements. The mechanics are governed by both IAS 21 and IFRS 9, which is exactly what makes them complex.

IFRIC 16 clarifies the key mechanics: the hedged risk is the exchange difference arising from a subsidiary with a different functional currency, the hedging instrument can be held anywhere in the group, and on disposal, reclassification adjustments follow IAS 21 for the hedged item and IFRS 9 for the hedging instrument. That split responsibility is not intuitive, and it requires coordination between treasury and accounting teams that many groups do not have.

Scenarios that require advanced handling:

- Group structures where an intermediate holding company holds the hedging instrument rather than the parent.

- Partial disposals where only a portion of the net investment is sold, triggering partial reclassification.

- Hyperinflationary subsidiaries, where KPMG notes that the closing rate applies to all amounts including comparatives, eliminating prior reserve patterns entirely.

- Functional currency changes triggered by shifts in the primary economic environment of a subsidiary.

Pro Tip: For net investment hedges in group structures, assign explicit ownership of the IAS 21 reclassification calculation to the consolidation team and the IFRS 9 instrument accounting to treasury. When one team handles both without a clear protocol, errors compound at disposal. Your risk governance strategies should formalize this split in writing.

You can also reference partner accounting approaches for practical structural guidance in Nordic and Central European group contexts.

Integrating hedge accounting with modern FX risk solutions

Qualifying for hedge accounting under IFRS 9 is not just a documentation exercise. It is a system design challenge. Your accounting software, treasury management system, and risk analytics platform all need to support the ongoing effectiveness testing and documentation that IFRS 9 requires.

Non-derivative financial instruments can qualify as hedging instruments for foreign currency risk under IFRS 9, which opens options beyond plain forward contracts. Foreign-currency denominated borrowings, for example, can hedge a net investment. But eligibility rules are strict, and the OCI election for equity investments creates additional constraints.

Steps to integrate hedge accounting with your FX risk infrastructure:

- Identify all qualifying exposures and map them to eligible hedging instruments before designation.

- Build effectiveness testing into your monthly close process, not as a separate annual exercise.

- Ensure your accounting software captures the hedge documentation at inception and stores it in an auditable format.

- Connect your live FX position data to your hedge accounting records so that changes in exposure trigger timely reassessment.

| Requirement | Manual approach | Technology-supported approach |

|---|---|---|

| Inception documentation | Word/PDF templates | Automated at designation |

| Effectiveness testing | Spreadsheet regression | Real-time analytics |

| Rebalancing decisions | Periodic review | Exposure-triggered alerts |

| Audit trail | Manual filing | System-generated logs |

Understanding how to manage currency risk at the operational level means connecting your accounting requirements to your live exposure data. The FX risk types your group faces, whether transaction, translation, or economic, determine which instruments qualify and how you structure the hedge relationship.

Non-GAAP performance measures and the impact of FX: Navigating SEC scrutiny

For companies with SEC reporting obligations, FX accounting does not end with IFRS. How you present FX impacts in non-GAAP metrics is a separate discipline with its own compliance requirements.

SEC rules under Regulation G and Item 10(e) of Regulation S-K govern how non-GAAP measures are presented, reconciled, and explained. When a company excludes FX gains or losses from an adjusted earnings metric, it must reconcile that metric to the nearest GAAP equivalent and give it no greater prominence than the GAAP figure. SEC officials have signaled that scrutiny on these measures is ongoing and intensifying.

What SEC reviewers focus on in FX-related non-GAAP disclosures:

- Whether the excluded FX item is presented consistently across periods.

- Whether the reconciliation is clear and uses the most directly comparable GAAP measure.

- Whether the company explains why the metric is useful to investors, not just what it excludes.

- Whether foreign private issuers apply the same prominence rules as domestic registrants.

Pro Tip: If your currency management strategies produce FX adjustments that appear in non-GAAP metrics, have your legal and accounting teams review the disclosure language before each filing. A vague explanation of why FX is excluded is one of the fastest ways to attract an SEC comment letter.

A practitioner's perspective: Why getting FX accounting right delivers real strategic value

Most guidance on FX accounting focuses on compliance. What it rarely says is that the discipline of separating translation from hedge accounting, and maintaining rigorous documentation, creates a measurable competitive advantage.

When translation and hedge accounting are muddled, performance measurement breaks down. A subsidiary that looks profitable in local currency can appear to underperform at group level purely because of inconsistent rate application. Leadership makes resource allocation decisions on flawed data. That is not a technical accounting problem. It is a strategic one.

Overreliance on ERP automation without trained staff is a silent risk we see repeatedly. Systems can automate the mechanics of translation. They cannot make the judgment call about whether a hedging relationship qualifies under IFRS 9, or whether a functional currency change has occurred. When those calls are wrong and automated at scale, the errors are large and expensive to unwind.

The companies that get this right treat FX accounting as a board-level discipline, not a back-office function. They model their exposures before hedging, not after. They document hedges at inception because they understand that retroactive documentation is not permitted, not because an auditor asked for it. And they build investor confidence by explaining FX impacts clearly, whether in IFRS financial statements or SEC filings.

Proactive exposure modeling, combined with advanced forex risk strategies, turns accounting accuracy into earnings stability. That is the real return on getting this right.

Discover advanced FX risk management with CorpHedge

For international finance teams ready to move from accounting clarity to execution, the gap between knowing the rules and operationalizing them is where value is won or lost. CorpHedge is built for exactly that gap.

CorpHedge gives financial decision-makers real-time visibility into currency positions, effectiveness testing support, and hedging based on Value at Risk methodology that aligns with IFRS 9 requirements. Whether you are managing net investment hedges across a European group structure or building a defensible non-GAAP disclosure framework, the platform connects your live exposure data to your accounting and reporting needs. Explore the full FX risk management solutions to see how CorpHedge supports compliance, accuracy, and earnings stability in one place.

Frequently asked questions

What determines whether IAS 21 or IFRS 9 applies for FX accounting?

IAS 21 applies to transaction translation and foreign operations consolidation. IFRS 9 covers hedge accounting, and IAS 21 explicitly excludes hedge accounting from its scope.

How are foreign exchange differences presented in financial statements?

Transaction FX differences go to profit or loss at settlement. Translation differences from consolidating foreign operations are captured in OCI and held in a separate equity reserve.

What are the key documentation requirements for hedge accounting under IFRS 9?

You must document the hedged item, the risk, the hedging strategy, and the effectiveness assessment method at inception. Non-derivative instruments can qualify, but eligibility rules are strict and must be confirmed before designation.

How do you handle accounting when operating in hyperinflationary economies?

All amounts, including comparatives, may need translation at the closing rate. KPMG's guidance on hyperinflationary presentation currencies describes how this eliminates prior reserve patterns and requires new controls.

What disclosures are required for FX impacts in non-GAAP measures for SEC reporting?

SEC rules require reconciliation to the nearest GAAP measure, equal or lesser prominence, and a clear explanation of why the metric is useful. Regulation G and Item 10(e) set the specific requirements that apply to FX-related adjustments.