TL;DR:

- Currency risk impacts margins, contracts, and competitiveness across global business functions.

- Exposure varies widely; firms in the top decile can have over 28% cash-flow variance from FX.

- Effective risk management requires tailored strategies, real-time monitoring, and balancing hedge costs and coverage.

Exchange rate swings are not a finance department problem. They cut straight through to gross margins, supplier contracts, payroll costs, and competitive positioning across every function of a global business. Foreign exchange risk is the potential for financial losses from changes in exchange rates affecting international transactions, and for the most exposed firms, it can account for a striking share of cash-flow volatility. This guide walks you through what currency risk actually is, how to measure your real exposure, and which strategies give your company the most control over outcomes rather than leaving profits at the mercy of the market.

Table of Contents

- What is currency risk and why does it matter?

- How much exposure do firms really face?

- Key strategies: Hedging, coverage, and cost-benefit trade-offs

- When (and why) should firms leave currency risk unhedged?

- Steps to building a practical currency risk management program

- The real-world challenge: Why a one-size-fits-all approach fails

- Take control: Solutions for advanced currency risk management

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Three types of risk | Transaction, translation, and economic risk all impact international firms in unique ways. |

| Impact is highly concentrated | A minority of global firms absorb the majority of real currency risk and volatility. |

| Hedging reduces, but doesn’t erase risk | FX hedges typically cut cash-flow volatility by about half for the most exposed firms, but don’t eliminate it. |

| There’s no universal hedge approach | Optimal risk management balances cost, coverage, and business needs—full hedging is not always best. |

| Tailored programs drive results | The best FX risk solutions fit the firm’s sector, exposure, and objectives for profit and cash flow stability. |

What is currency risk and why does it matter?

Most finance leaders know currency risk exists. Fewer have a sharp picture of exactly how it enters their business and where it hurts most. At its core, foreign exchange risk describes the financial losses or earnings volatility that arise when exchange rates move against your open positions in international transactions.

There are three distinct types, and conflating them leads to poorly targeted risk programs:

- Transaction risk is the most visible. It occurs when your company has a contractual obligation to pay or receive a fixed amount in a foreign currency at a future date. A U.S. manufacturer that invoices a European buyer in euros faces transaction risk from invoice date to payment date. A 5% euro depreciation over 60 days directly reduces dollar-denominated revenue.

- Translation risk affects multinationals that consolidate foreign subsidiary financials into a home-currency balance sheet and income statement. Even if no cash changes hands, a strong dollar can erase the reported profits of a profitable overseas operation purely through accounting conversion.

- Economic risk is the subtlest and most strategic. It reflects how long-term exchange rate trends erode your competitive position. If a competitor's home currency weakens permanently, they can undercut your pricing in shared markets, regardless of your hedging program.

"Currency risk is often misread as a treasury problem. In reality, economic exposure reshapes product strategy, procurement decisions, and market entry timelines. The sooner operations leaders recognize this, the better."

Understanding all three types matters because each demands a different response. Strategies for mitigating FX volatility on transaction exposures will not protect you from the slow erosion of economic risk over a multi-year horizon. Mapping your exposure by type is the first serious step toward building a policy that actually works.

How much exposure do firms really face?

The answer depends almost entirely on which firm you ask. The distribution of currency risk across companies is highly unequal, and this is one of the most important and least-discussed facts in corporate FX management.

Academic research shows that firms' currency risk is concentrated: hedging via FX derivatives reduces cash-flow variance for the most exposed companies, but typically does not eliminate it fully. For the highest-exposure decile, exchange rates can explain a meaningful and significant portion of cash-flow variance.

Here is how that exposure tends to distribute across a typical population of international firms:

| Exposure decile | Exchange rate share of cash-flow variance | Effect of hedging |

|---|---|---|

| Bottom 50% | Near zero | Minimal benefit |

| 51st to 75th percentile | Low to moderate (under 5%) | Marginal reduction |

| 76th to 90th percentile | Moderate (5% to 15%) | Meaningful reduction |

| Top 10% | Up to 28% or higher | Significant, partial reduction |

What this data tells you is simple but consequential. If your firm sits in the top decile of FX exposure, exchange rate movements can single-handedly explain more than one quarter of your cash-flow variance. A 28% swing in cash-flow predictability has real consequences for investment planning, debt covenants, and dividend commitments.

The dangerous assumption is that industry averages apply to your firm. They almost never do. A company with 70% of revenues in foreign currencies but domestic-currency cost structures faces a fundamentally different risk profile than a firm with matched revenues and costs across regions. Understanding which firms are impacted most requires a granular breakdown of your own revenue, cost, and balance-sheet currency mix, not a benchmark from a peer report.

The takeaway: Before designing any hedging program, your team needs a current-state exposure map. Without one, you are either under-hedging or paying for protection you do not need.

Key strategies: Hedging, coverage, and cost-benefit trade-offs

Once you know your exposure, the next question is what to do about it. The toolkit for currency risk management is well established, but the choices within it carry significant trade-offs that are easy to get wrong.

The three core hedging instruments are:

Forward contracts lock in a specific exchange rate for a future transaction date. They are simple, widely available, and eliminate uncertainty on a specific payment or receipt. The cost is opportunity cost: if the rate moves in your favor, you do not benefit.

Currency options give you the right but not the obligation to transact at a set rate. They protect against adverse moves while allowing you to benefit from favorable ones. The trade-off is the premium you pay upfront, which can be significant for longer tenors or volatile currency pairs.

Cross-currency swaps are suited to multi-year exposures, often used to hedge the currency risk on foreign-currency debt or long-term intercompany arrangements. They involve exchanging both principal and interest payments in different currencies over the contract life.

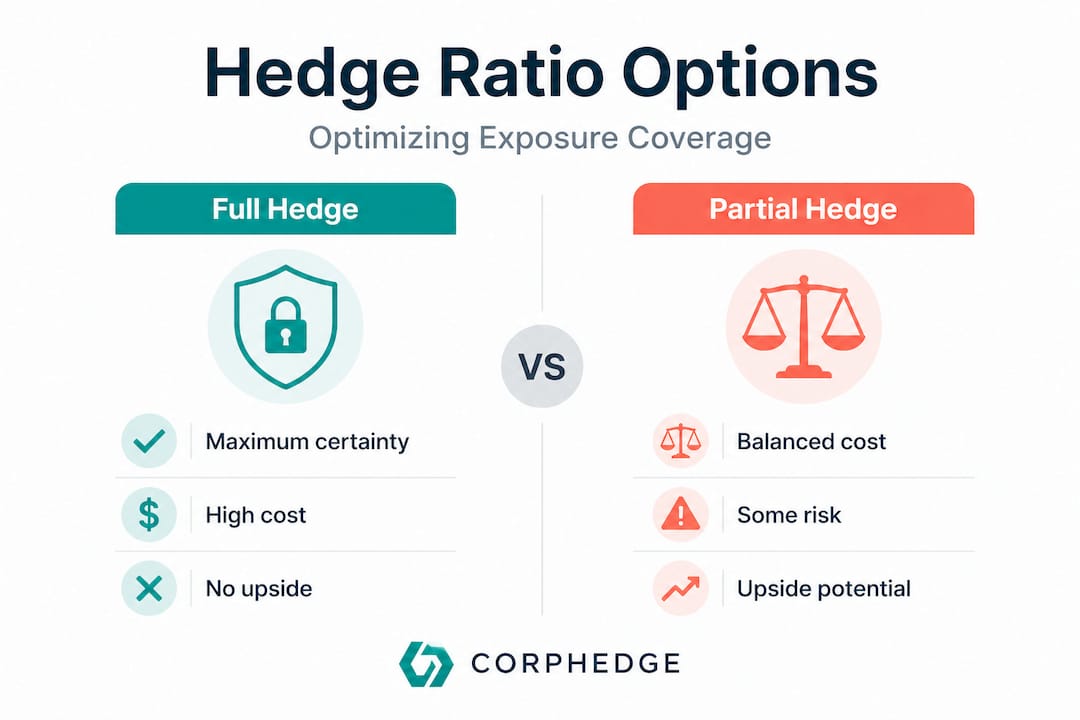

Choosing among these tools requires clarity on your hedge ratio: the proportion of your identified exposure you actually hedge. A 100% hedge ratio on every exposure sounds safe, but FX hedging programs are best framed as optimizing the trade-off among hedge cost, coverage ratio, and the risk-return role of the exposure, rather than defaulting to maximum coverage at all times.

| Hedge approach | Pros | Cons |

|---|---|---|

| Full hedge (100%) | Maximum certainty, clean P&L | High cost, no upside participation, complex to maintain |

| Partial hedge (40% to 80%) | Balanced cost and protection | Residual volatility remains |

| No hedge (0%) | Zero hedging cost | Full exposure to rate movements |

Explore FX hedging strategies and advanced risk reduction techniques to match the right tool to your specific exposure profile.

A practical prioritization sequence for deciding what to hedge first:

- Identify all foreign currency cash flows expected in the next 12 months by currency pair and settlement date.

- Rank exposures by size and volatility of the relevant currency pair.

- Assess natural offsets: revenues and costs in the same foreign currency net against each other.

- Calculate the cost of hedging each net position relative to the projected cash-flow impact of a 1-standard-deviation rate move.

- Apply hedges to exposures where the cost-benefit ratio is clearly favorable, and revisit the rest quarterly.

Pro Tip: One of the most common hedging mistakes is ignoring the carry cost of your hedge relative to the actual volatility of the currency pair. Paying a 2.5% annualized forward premium to hedge a currency that historically moves less than 1% per year is not risk management. It is an expense masquerading as prudence. Run the numbers before you commit.

When (and why) should firms leave currency risk unhedged?

This is where most corporate FX guides go quiet. The assumption is that more hedging is always better. The reality is more nuanced, and getting it wrong in either direction is costly.

Research from institutional asset managers argues that currencies are hard to forecast, and that firms and investors can easily end up taking unintended currency bets through permanently unhedged positions. At the same time, that same research advocates for leaving room for dynamic hedging strategies rather than locking into a static, always-hedged posture.

Situations where leaving some exposure unhedged can be the right call:

- Natural hedging exists. If you earn and spend in the same foreign currency, the net exposure may be small enough that hedging costs exceed the risk reduction benefit.

- The hedge cost is prohibitive. For currencies in high-inflation economies, forward premiums can reach 10% to 20% annually. Paying that to hedge a margin-thin business line destroys value faster than exchange rate volatility would.

- You have diversification across currency pairs. If your exposure is spread across many currencies with low correlation, your portfolio-level FX risk may be far lower than the sum of individual exposures suggests.

- Your pricing is flexible and responsive. Some businesses can reprice contracts or renegotiate terms faster than FX moves develop into losses. Hedging a repriced exposure double-counts the protection.

The risks of unintended currency bets are equally real:

- Consistently unhedged positions can look like speculative currency trading from a governance perspective.

- A multi-quarter adverse move in an unhedged exposure can create earnings surprises that damage investor confidence far more than a modest hedge cost would have.

- Unhedged translation exposure in a high-volatility currency can create balance sheet swings that breach debt covenant ratios.

Pro Tip: Consider combining a static core hedge (covering your most predictable, highest-volume exposures at a fixed ratio) with a dynamic overlay that adjusts the hedge ratio quarterly based on market conditions and your company's near-term cash-flow certainty. This approach lets you manage currency fluctuations without locking your entire book into costly positions regardless of conditions.

Steps to building a practical currency risk management program

Theory only matters if it translates into an operational process your team can run consistently. Here is a step-by-step framework for standing up or strengthening a currency risk management program:

- Map your exposures. Document all foreign currency revenues, costs, assets, and liabilities by currency pair, amount, and timing. Include intercompany flows, which are often overlooked. The Foreign Exchange Risk framework categorizes these into transaction, translation, and economic buckets.

- Quantify the risk. Use Value at Risk (VaR) or cash-flow-at-risk models to translate your exposure map into potential dollar impacts under different market scenarios. This converts abstract exposure into board-digestible numbers.

- Define your risk appetite. Set a clear policy: how much cash-flow variance from FX is acceptable? What is the maximum tolerable loss on any single currency pair in a quarter? This must have executive and board sign-off.

- Select your instruments. Based on the exposure type and your risk appetite, choose the appropriate hedging instruments and counterparties. Validate that your banking relationships and credit lines support the instruments you plan to use.

- Execute and document. Implement hedges with clear documentation linking each position to the underlying exposure. This matters for both accounting treatment and audit purposes.

- Monitor in real time. Currency positions change daily. Set up dashboards that show live mark-to-market positions relative to your policy limits. Refer to your transaction hedging guide for granular transaction-level monitoring approaches.

- Review and adjust. Conduct quarterly hedge effectiveness reviews. Assess whether the risk reduction achieved justified the cost. Adjust the hedge ratio and instrument mix as your business evolves.

The ongoing data-driven adjustment piece is frequently where programs fail. A policy set once and never revisited becomes irrelevant within 18 months as your revenue mix, market footprint, and rate environment shift.

The real-world challenge: Why a one-size-fits-all approach fails

Here is an uncomfortable truth that most FX hedging discussions sidestep. Maximum hedging is not best practice. It is a risk-management posture that happens to be easy to defend in a board meeting, but it is not necessarily right for your company.

Consider a technology firm with 40% of revenue in euros and a largely USD-denominated cost base. A full hedge on every euro exposure removes the translation benefit that would naturally occur when the dollar weakens, a period when that same company's USD costs fall in real terms and their euro revenue becomes more competitive globally. Hedging away 100% of that exposure in all environments is not neutral. It is taking a position that volatility is always harmful, which is demonstrably false for some business models.

FX hedging programs are most effective when framed as optimizing a trade-off among hedge cost, coverage ratio, and the strategic role that currency exposure plays in your total risk-return profile. A commodity exporter with thin margins and highly correlated FX and commodity pricing needs a completely different approach than a services firm with sticky long-term contracts.

Sector matters enormously. Manufacturers, commodity traders, and retailers with global supply chains face very different exposure profiles from financial services firms or SaaS companies. Regional concentration matters. A firm heavily exposed to emerging market currencies faces liquidity constraints and hedge costs that a firm managing only G10 pairs does not encounter.

What is changing the game for agile firms is the availability of advanced analytics. Real-time exposure aggregation, scenario modeling, and VaR-based strategy frameworks allow treasury teams to make decisions with a level of precision that was reserved for large multinationals a decade ago. Firms that invest in financial risk reduction best practices and modern platforms are moving away from static quarterly hedging reviews toward continuous risk monitoring that responds to market conditions as they develop.

The standard cookie-cutter approach of "hedge 75% of the next 12 months of exposure with forwards" works for no firm in particular. Context, objectives, and data need to drive every program design.

Take control: Solutions for advanced currency risk management

Understanding currency risk theory is valuable, but translating it into an operational program is where most companies struggle. The gap between knowing you have exposure and having real-time visibility into your positions, a clear policy, and the right instruments in place is where profit leaks.

CorpHedge is built specifically for international companies that need to move beyond spreadsheet-based FX tracking. The platform gives your team live visibility into currency positions, supports hedging based on value at risk so your hedge decisions are grounded in quantified risk rather than guesswork, and integrates with your existing systems to eliminate manual data gaps. Take a risk management product tour to see how the platform maps exposures and models hedge outcomes. Explore the full suite of FX risk management features designed to give finance teams the control and confidence they need to protect margins across every market they operate in.

Frequently asked questions

What are the three main types of currency risk?

The three types are transaction risk (on specific foreign currency payments or receipts), translation risk (on consolidation of foreign subsidiary financials), and economic risk (on long-term competitive positioning). Each requires a different management approach.

How much can currency fluctuations affect a company's cash flow?

For the most exposed firms, exchange rates can explain up to 28% of cash-flow variance, and even partial hedging with FX derivatives can meaningfully reduce that volatility without eliminating it entirely.

Should all currency risk be fully hedged?

Not necessarily. FX hedging programs are better framed as an optimization of cost, coverage ratio, and risk-return objectives, meaning partial or selective hedging often delivers better outcomes than a blanket maximum-hedge policy.

What tools do companies use to hedge currency risk?

The primary tools are forward contracts, currency options, and cross-currency swaps. Forwards provide certainty on a known future payment, options add flexibility at a premium cost, and swaps suit long-duration or debt-related exposures.

What is a hedge ratio?

A hedge ratio is the percentage of a company's total identified currency exposure that it chooses to hedge through financial instruments, ranging from zero (no hedging) to 100% (full hedge), with most firms finding that a partial ratio optimizes cost versus protection.