TL;DR:

- Most finance teams wrongly treat VaR as a complete risk measure, but it only estimates maximum losses under normal market conditions. Effective FX hedging requires selecting the appropriate VaR method, calibrating it for specific horizons, and maintaining operational governance to prevent miscalibration and misuse. Incorporating Expected Shortfall alongside VaR offers a more comprehensive view of tail risks and enhances overall risk management effectiveness.

Most finance teams treat VaR as a complete risk picture. It isn't. Value at risk estimates the maximum loss not expected to be exceeded over a specified time horizon at a chosen confidence level under normal market conditions. That definition carries a critical qualifier: "normal." For international companies managing multi-currency FX exposures, that qualifier is where the trouble starts. VaR hedging, when understood and applied correctly, gives treasury teams a disciplined framework for quantifying exposure and sizing hedges. Used blindly, it creates a false sense of security precisely when markets behave abnormally.

Table of Contents

- Understanding value at risk and its role in currency hedging

- A practical VaR hedging workflow for managing FX exposure

- Choosing and calibrating VaR models for varying hedging horizons

- Limitations of VaR in hedging and the rise of expected shortfall

- Best practices and governance for effective VaR-based FX hedging

- Rethinking VaR hedging: beyond a singular risk metric

- Explore CorpHedge solutions for advanced VaR-based FX risk management

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| VaR basics | Value at Risk estimates potential losses within set horizons and confidence levels for FX exposure. |

| Practical workflow | Defining exposure and applying VaR over short horizons guides hedge limits and prioritization. |

| Model selection | Tailoring VaR models to hedging horizon improves forecast accuracy and risk mitigation. |

| VaR limitations | VaR misses tail risk severity, prompting regulatory shifts to Expected Shortfall. |

| Governance matters | Aligning hedge instruments and real-time data ensures effective VaR-based hedging. |

Understanding value at risk and its role in currency hedging

VaR starts with a simple question: how much can we lose? The answer always comes with three parameters attached: a time horizon, a confidence level, and an assumption about market behavior. A 95% one-day VaR of $500,000 means there is a 5% probability the portfolio loses more than $500,000 in a single day. That residual 5% is where every serious risk professional should be paying close attention.

Understanding the value at risk basics before applying them operationally matters more than most firms acknowledge. For FX exposures specifically, VaR formulations convert modeled currency rate moves into home-currency P&L impacts for hedging limits. A EUR/USD rate shift modeled at 95% confidence translates directly into a euro-denominated loss figure your treasury can act on.

Three primary methods drive most VaR calculations:

- Historical simulation: Uses actual past price moves to simulate the portfolio's P&L distribution. No distribution assumptions required, but heavily dependent on the sample window chosen.

- Variance-covariance (parametric): Assumes returns follow a normal distribution. Fast and analytically clean, but structurally underestimates fat-tail events in FX markets.

- Monte Carlo simulation: Generates thousands of random price paths based on modeled correlations and volatilities. Computationally intensive but handles complex portfolios and non-linear instruments well.

Three main VaR methods exist: historical, variance-covariance, and Monte Carlo simulation. Each serves different risk management needs, and choosing the wrong one for your FX book can produce systematically misleading hedge sizing.

For practical corporate currency risk management, the method choice is rarely just a technical decision. It reflects how your team interprets market stress, how often you recalibrate, and what instruments sit in your hedging portfolio. Options positions require Monte Carlo. Clean forward books can often work with historical simulation. The point is to match method to reality, not to default to what the last consultant recommended.

Key VaR inputs for FX risk quantification:

- Net currency exposure by pair (e.g., USD/PLN, EUR/SEK)

- Historical or implied volatility of each pair

- Correlation matrix across currency pairs

- Time horizon tied to your hedging cycle

- Confidence level aligned with your risk appetite

Exploring hedging strategies in forex reveals that most firms under-invest in building consistent volatility inputs, which is often the single biggest source of VaR inaccuracy in practice.

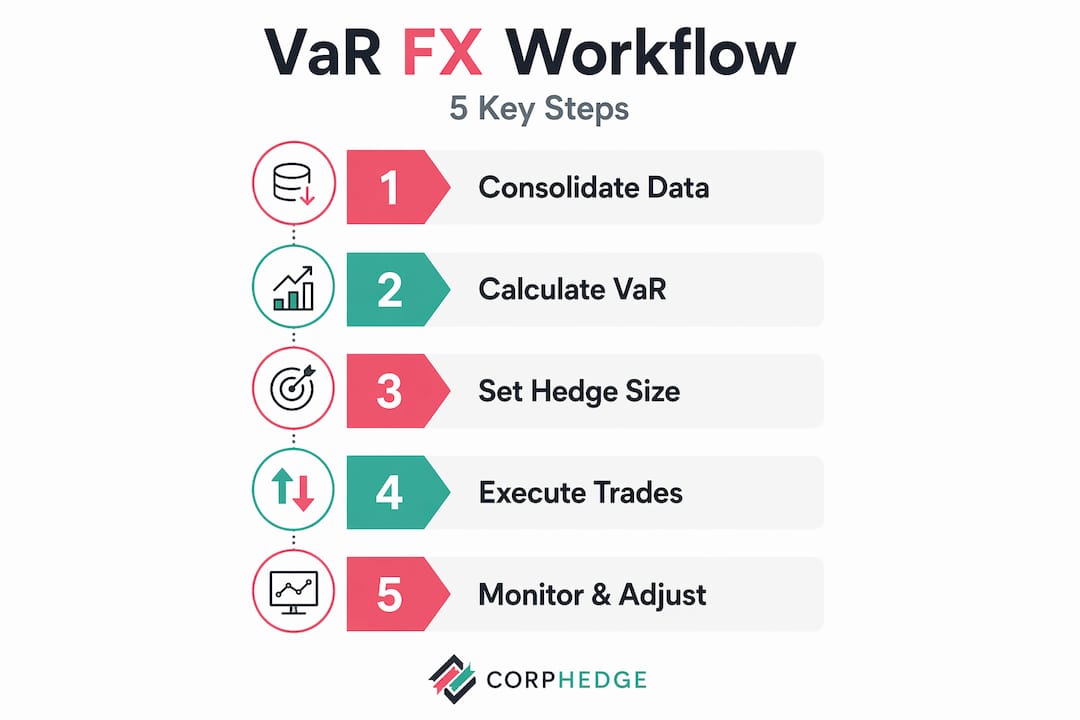

A practical VaR hedging workflow for managing FX exposure

Knowing the theory is one thing. Having a repeatable workflow that translates VaR into daily treasury decisions is another. A practical workflow includes defining net exposure, computing VaR over short horizons (daily or weekly), and translating this into hedge sizing and operational rules.

Here is how that process works in practice:

- Define net FX exposure by currency pair. Aggregate all receivables, payables, and financial instrument positions. Net USD receivables against USD payables before computing VaR. Gross exposure overstates risk and leads to over-hedging.

- Select time horizon and confidence level. For operational hedging, one-day or one-week VaR at 95% confidence works well. For budget hedging tied to annual forecasts, a monthly or quarterly horizon at 99% may be more appropriate.

- Run VaR calculation using your chosen method. Apply it at the portfolio level, not currency by currency. Correlation effects between pairs can meaningfully reduce aggregate VaR below the sum of individual VaR figures.

- Translate VaR into hedge limits. A VaR of $1.2M at 95% weekly confidence tells you the unhedged book could lose $1.2M in a normal week. Set the hedge ratio to bring that exposure within your board-approved risk tolerance.

- Set escalation thresholds. When VaR breaches predefined limits due to market movement or new exposures, trigger an automatic review. This is where VaR becomes a governance tool, not just a reporting metric.

- Review and rebalance. Recompute VaR whenever significant new exposures arise or market volatility shifts materially. Static hedge programs that ignore VaR drift are a common failure mode.

Pro Tip: Build your practical FX risk workflow around a single source of truth for net exposure. The most common operational failure in VaR hedging is not a modeling error. It is treasury working from a different exposure number than accounting. Solve that first.

The value at risk workflow that connects VaR outputs to hedge execution must account for instrument settlement timing. A three-month forward booked today hedges a specific future cash flow, not just a static exposure number. Misaligning timing creates phantom coverage that only shows up as a loss during realization.

Operational consistency in forex risk settings also matters when managing multiple currency pairs under a single VaR framework.

Choosing and calibrating VaR models for varying hedging horizons

Short-horizon VaR models work reasonably well. The problems compound as you extend the time horizon. Classical VaR methods perform poorly for one-year ahead exchange rate forecasts, but alternative approaches using data decay greatly enhance accuracy.

Why does performance degrade? Because VaR models trained on recent history implicitly assume the recent past predicts the near future. Over a one-day or one-week horizon, that assumption is defensible. Over 12 months, currency regime changes, central bank pivots, and structural macro shifts make it unreliable.

Model comparison by hedging horizon:

| Horizon | Recommended method | Key calibration consideration |

|---|---|---|

| 1 day | Historical simulation | Use 250-day rolling window |

| 1 week | Variance-covariance | Update volatilities weekly |

| 1 month | Monte Carlo | Include stochastic vol inputs |

| 1 quarter | Decay-weighted historical | Higher weight on recent 60 days |

| 1 year | Regime-aware simulation | Incorporate macro scenario overlays |

Decay-weighted data, also called exponentially weighted moving average (EWMA) VaR, assigns higher weight to more recent price observations. This approach responds faster to volatility regime shifts, which is exactly what long-horizon FX risk models need to remain useful.

Pro Tip: For advanced forex risk strategies tied to annual budget cycles, consider running parallel VaR models at multiple decay parameters and reporting the range rather than a single figure. It is a simple way to communicate model uncertainty to senior leadership without needing to explain the math.

Model degradation is a real governance problem. A VaR model calibrated in 2023 and never revisited will produce increasingly unreliable hedge sizing as market conditions evolve. Schedule model reviews quarterly at minimum, and trigger an immediate review whenever a major currency pair moves beyond a three-standard-deviation event.

Limitations of VaR in hedging and the rise of expected shortfall

VaR is not a complete risk measure. It never was. The limitation is structural, not a calibration problem you can fix.

"VaR tells you very little about what happens when things go badly," which is precisely why reliance on Expected Shortfall to capture tail severity has grown significantly under modern regulatory frameworks.

Here is exactly what VaR does not tell you:

- How bad the bad days actually are. VaR says losses will exceed $X with 5% probability. It says nothing about whether the excess is $50,000 or $5,000,000.

- What happens in fat-tail markets. Currency markets are not normally distributed. Black swan events, geopolitical shocks, and sudden liquidity crises appear far more frequently than a normal distribution predicts.

- Whether your hedge instruments remain liquid. A VaR model calibrated on normal market conditions does not account for bid-ask spread blowouts during stress periods, when executing hedges becomes expensive or impossible.

- Procyclicality effects. VaR-based capital requirements can shrink during calm periods and spike during crises, forcing hedge unwinds at exactly the wrong moment.

Expected Shortfall (ES), sometimes called Conditional VaR or CVaR, addresses the first two limitations directly. ES asks: given that we have already exceeded the VaR threshold, what is the average loss? If 95% VaR is $500,000 and the average loss in the worst 5% of scenarios is $1.8M, ES is $1.8M. That is a very different risk signal.

The Basel Committee's Fundamental Review of the Trading Book (FRTB) regulations formally replaced VaR with ES as the primary market risk measure for regulatory capital. For internationally active firms, that regulatory shift is already shaping how smart forex risk management teams structure their internal risk frameworks. Even if you are not a bank, aligning with ES-based thinking improves your internal governance.

Best practices and governance for effective VaR-based FX hedging

The most underappreciated source of VaR hedging failure is not the model. It is operational and governance breakdown. Hedge cashflows and P&L must align precisely with model risk factors to avoid false coverage impressions.

Operational best practices for VaR-based FX hedging:

- Match hedge instruments to modeled risk factors. If your VaR model uses spot FX as the risk driver, a cross-currency swap with basis risk components may not provide the coverage your model claims.

- Net receivables and payables before hedging. Hedging gross flows creates unnecessary costs and distorts your effective VaR coverage. Treasury and accounts receivable teams must share exposure data in real time.

- Recalculate VaR on a daily basis. Static weekly or monthly VaR reporting is inadequate for active FX books. Currency volatility can shift materially in 24 hours.

- Build hedge governance around model updates. When you update VaR calibration, review existing hedge positions for continuing relevance. A hedge sized against last quarter's VaR may be over- or under-sized today.

- Treat hedging as a continuous program, not a series of trades. Individual forward contracts should fit within a portfolio-level VaR framework. Booking trades in isolation produces a patchwork that looks hedged on paper but carries significant net exposure.

Operational breaks or poor data quality in VaR models can trigger margin-call cascades when hedge capital is most needed, making real-time model governance critical. This is not a hypothetical. Firms that discovered data feed failures during the 2022 EUR/USD volatility spike learned this lesson at real cost.

Pro Tip: Run a monthly "VaR audit" where you compare your model's predicted loss distribution against actual P&L over the prior 30 days. If your model predicted a 95% VaR of $400,000 but you experienced three days with losses exceeding that threshold in a single month, your model is significantly miscalibrated. This FX risk mitigation discipline pays dividends over time.

Rethinking VaR hedging: beyond a singular risk metric

Here is an uncomfortable truth most risk management frameworks avoid: VaR's widespread adoption was partly driven by its simplicity, not its accuracy. A single number that summarizes portfolio risk is enormously convenient for senior management reporting. That convenience has a cost.

VaR provides a loss threshold but tells you very little about what happens when things go badly, which is precisely why a shift toward Expected Shortfall and integrated risk approaches is not optional for serious FX risk programs.

What we consistently see in practice is that companies using VaR as their only FX risk metric tend to under-hedge during calm periods (because VaR looks small) and over-react during volatile periods (because VaR spikes suddenly). Both behaviors destroy value. The teams that manage currency risk well treat VaR as one input within a broader framework that includes ES, cash flow at risk (CFaR), scenario analysis, and qualitative macro judgment.

There is also a communication problem worth naming. When treasury teams speak VaR and business unit leaders think in budget variance, the shared understanding needed for good hedge decisions breaks down. A consistent risk language across treasury and finance, one that connects VaR figures to business outcomes like margin erosion or cash flow shortfalls, is what separates reactive hedging programs from genuinely resilient ones.

The advanced smart forex risk approaches that work in 2026 combine quantitative rigor with operational discipline and shared governance. VaR is the starting point. It should not be the finish line.

Explore CorpHedge solutions for advanced VaR-based FX risk management

The gap between understanding VaR and operationalizing it in a live FX book is where most treasury teams struggle. CorpHedge bridges that gap with purpose-built tools that integrate VaR calculations directly into hedging workflows, so your team spends less time building spreadsheets and more time making informed decisions.

VaR-based hedging solutions from CorpHedge support multi-currency exposure monitoring, automated hedge sizing aligned with your VaR thresholds, and real-time P&L tracking that flags model drift before it becomes a governance problem. Coverage spans emerging market currencies including Polish zloty and Swedish krona, which matter for international firms operating across Central and Northern Europe. Take a CorpHedge product tour to see how the platform connects exposure data, VaR analysis, and hedge execution in a single interface designed for treasury and risk teams. Explore the full FX exposure management features to find the right configuration for your organization's risk appetite and reporting requirements.

Frequently asked questions

What is Value at Risk (VaR) in currency hedging?

VaR estimates the maximum potential loss in currency exposure over a set timeframe at a specific confidence level, helping quantify risk in FX positions. It is a threshold measure, not a description of worst-case outcomes.

How does VaR help in managing foreign exchange risk?

VaR translates currency rate volatility into potential home-currency losses, enabling finance teams to set actionable risk limits and trigger hedging actions. It helps set limits and priority for FX exposure by quantifying potential losses within chosen horizons and confidence levels.

Why are classical VaR models insufficient for long-term FX risk forecasting?

Classical VaR methods perform poorly for one-year ahead exchange-rate forecasts, with alternative approaches using data decay substantially improving performance. Model assumptions about return distributions break down over longer time horizons where regime changes occur.

What are the main limitations of VaR in currency risk management?

VaR ignores tail losses beyond its confidence threshold, assumes normality that underestimates fat tails, and can produce procyclical capital demands. These structural limitations motivated the regulatory shift to Expected Shortfall under FRTB.

How can companies improve FX hedging effectiveness beyond VaR?

Using Expected Shortfall alongside VaR captures tail risk more accurately, and operational diligence with model alignment and data quality enhances hedging reliability. Integrating governance with real-time VaR recalculation ensures hedge sizing stays current with actual market conditions.

How does CorpHedge support VaR-based FX risk management?

CorpHedge offers automated tools that integrate VaR calculations with hedge sizing, exposure monitoring, and compliance aligned with regulatory standards for multiple international markets. The platform connects treasury workflows and real-time FX data in a single interface built specifically for risk management teams.