TL;DR:

- Effective FX hedging reduces cash flow volatility by 23-45% and increases earnings stability.

- Strategies include a mix of static and dynamic approaches tailored to market regimes and company resources.

- Proper planning, regular review, and understanding of costs and risks are essential for successful currency risk management.

Currency risk is one of the most underestimated threats to corporate profitability. Finance teams that assume a simple policy or a single forward contract will protect them often discover the hard way that markets move faster than spreadsheets. Unhedged FX positions can amplify earnings volatility across reporting periods, erode margins on cross-border contracts, and distort cash flow forecasts. The good news is that companies with structured hedging programs experience 23-45% less volatility and 30-50% greater earnings stability. This guide breaks down what FX hedging is, why it matters, and how to apply it effectively.

Table of Contents

- What is FX hedging? Defining the essentials

- Core FX hedging strategies explained

- Risks, costs, and practical realities of FX hedging

- What successful FX hedging delivers: Outcomes and lessons

- Our perspective: Why standard FX hedging advice falls short

- How CorpHedge simplifies FX hedging for your business

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| FX hedging reduces volatility | Empirical studies show FX hedging cuts company cash flow volatility by up to 45 percent. |

| No strategy is one-size-fits-all | Selecting and adjusting the right FX hedging method depends on company needs and market conditions. |

| Imperfect hedges are normal | Even sophisticated FX hedging approaches leave some risks unmanaged due to costs and market limits. |

| Dynamic strategies perform best | Active, adaptable FX hedging outperforms static policies in volatile environments. |

| Expert tools ease implementation | Professional platforms streamline setup, compliance, and optimization of FX hedging programs. |

What is FX hedging? Defining the essentials

FX hedging is the practice of using financial instruments or operational strategies to protect your business cash flows and profits from adverse currency movements. Think of it as an insurance policy for your international revenue. You are not trying to profit from exchange rate moves. You are trying to neutralize their impact on your bottom line.

Two common misconceptions trip up even experienced teams. First, many assume hedging is only for large multinationals with dedicated treasury departments. In reality, any company with cross-border invoicing, foreign-denominated debt, or overseas payroll carries FX exposure worth managing. Second, some believe hedging eliminates all currency risk. It does not. Perfect hedges are rare, and it is usually impractical or expensive to eliminate every dollar of exposure.

Hedges generally fall into two broad categories:

- Financial contracts: Forwards, futures, options, and swaps that lock in or cap exchange rates for future transactions.

- Natural hedges: Matching revenues and costs in the same currency, or sourcing locally to reduce net exposure without derivatives.

Most real-world hedging programs address the bulk of exposure, not all of it. A company might hedge 70-80% of its projected foreign currency receivables over a rolling 12-month horizon, leaving a residual position unhedged to avoid over-hedging if forecasts change. This is a deliberate, professional choice, not a failure.

"Imperfect hedges are the norm. The goal is meaningful risk reduction, not mathematical perfection."

Understanding currency risk management strategies at a structural level helps you set realistic expectations before you choose any instrument. The best hedging programs start with a clear policy that defines exposure types, hedge ratios, approved instruments, and review frequency. Without that foundation, even sophisticated tools can create more confusion than clarity.

Pro Tip: Document your hedging policy before selecting instruments. A written policy forces alignment across finance, treasury, and senior leadership, and it is required for hedge accounting under IFRS 9 and ASC 815.

If you are new to the mechanics of hedging forex risk, start by mapping your exposure: which currencies, which directions, and over what time horizons. That map is the foundation of every decision that follows.

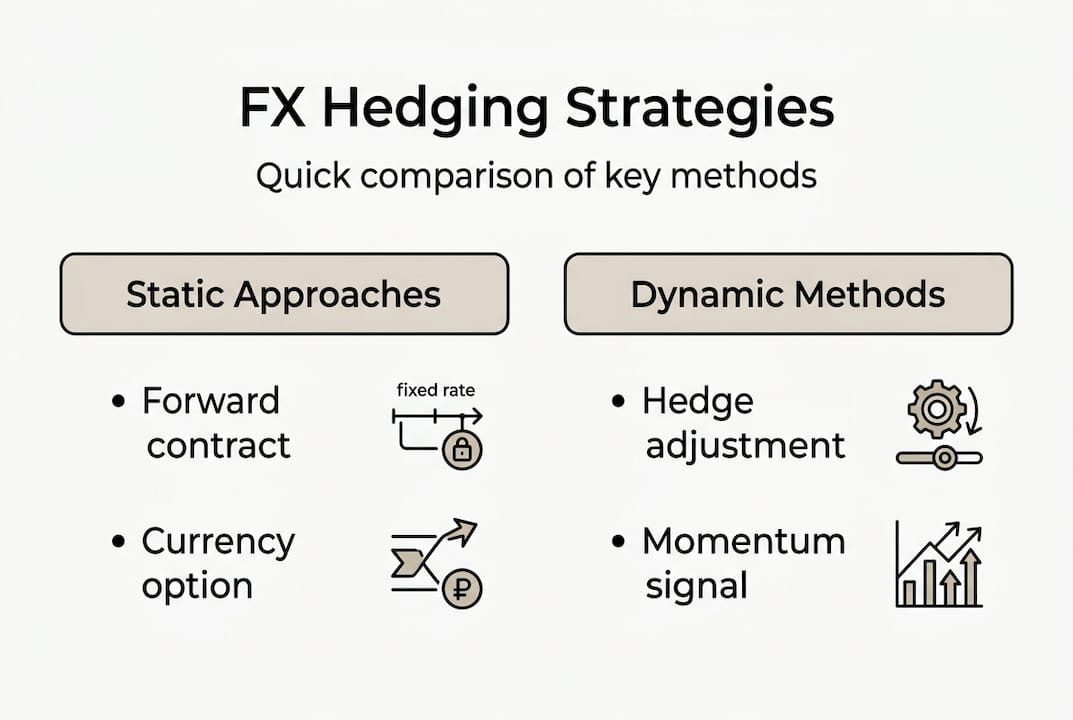

Core FX hedging strategies explained

With a solid definition in hand, let's break down the practical strategies professionals use to manage FX risk. The choice of instrument is not just a technical decision. It reflects your company's risk appetite, cash flow predictability, and operational capacity.

Comparison of core FX hedging instruments

| Instrument | Best for | Key advantage | Key limitation |

|---|---|---|---|

| Forward contracts | Known future cash flows | Certainty of rate | No upside if rate moves favorably |

| Futures | Standardized, liquid exposures | Exchange-traded, transparent | Basis risk, margin requirements |

| Options | Uncertain exposure size | Flexibility, upside preserved | Premium cost |

| Swaps | Long-term debt or recurring flows | Tailored structure | Counterparty risk, complexity |

| Natural hedge | Operational alignment | No instrument cost | Limited applicability |

Choosing the right strategy depends on three factors:

- Currency volatility: High-volatility pairs (e.g., emerging market currencies) often justify options despite their cost, since the range of outcomes is wide.

- Exposure profile: Highly predictable cash flows suit forwards. Variable or contingent exposures suit options.

- Management resources: Dynamic strategies require active monitoring. If your team lacks bandwidth, simpler instruments with longer tenors may be more practical.

Static hedging locks in a hedge ratio at the start of a period and leaves it unchanged. It is simple and cheap to administer, but it can underperform when market conditions shift significantly. Advanced methodologies include dynamic hedging, correlation hedging, structured products, natural hedging, and regime-switching models that adjust coverage as volatility regimes change.

"The best strategy is the one your team can actually execute consistently, not the most sophisticated one on paper."

For companies exploring best practices in FX hedging, the practical answer is often a layered approach: a core static hedge for the high-confidence portion of exposure, with dynamic overlays for the uncertain tail. This mirrors how institutional investors manage fixed income duration. It is also worth noting that currency volatility prevention methods extend beyond derivatives into pricing strategy, contract structuring, and supplier negotiation. Even hedging in crypto markets has borrowed these layered frameworks, which shows how broadly applicable the core logic is.

Risks, costs, and practical realities of FX hedging

Knowing the choices is only half the battle. Let's examine what actually happens when companies implement FX hedging.

The first reality is that risk cannot be fully eliminated. Basis risk, the difference between the hedge instrument's price movement and the actual exposure, can be meaningful. Basis risk in FX futures can reach 5.9%, swaps carry measurable counterparty credit risk (with credit valuation adjustment, or CVA, reaching €15.6M in some cases), and hedge accounting involves additional compliance requirements that many teams underestimate.

The second reality is cost. Hedging is not free.

- Transaction costs: Bid-ask spreads on forwards and options, brokerage fees on futures.

- Carry costs: The interest rate differential between two currencies, which can make forward rates significantly different from spot rates.

- Value at Risk (VaR): Capital that must be reserved or reported against open derivative positions.

- Opportunity cost: If you lock in a rate and the market moves in your favor, you do not benefit.

Typical cost ranges by instrument

| Instrument | Estimated cost range | Primary cost driver |

|---|---|---|

| Forward contract | 0.1-0.5% of notional | Bid-ask spread, credit line |

| FX option (vanilla) | 0.5-2.5% of notional | Volatility, tenor |

| Cross-currency swap | 0.2-1.0% of notional | CVA, structuring |

| Natural hedge | Near zero direct cost | Operational complexity |

Regulatory hurdles add another layer. In the US, retail direct hedging (simultaneously holding long and short positions in the same currency pair) is banned under CFTC rules. Requirements differ by jurisdiction, so your legal and compliance teams must be involved before any program goes live. Documentation for hedge accounting under IFRS 9 or ASC 815 requires formal designation, effectiveness testing, and ongoing reporting.

Pro Tip: Run a cost-benefit analysis before hedging. If the cost of the hedge exceeds the expected volatility impact on your margins, a partial hedge or natural hedge may be more economically rational. Review risk management best practices to build a framework that balances protection with efficiency.

For a deeper look at reducing financial risk from FX, the key is building a policy that specifies acceptable cost thresholds alongside acceptable risk thresholds.

What successful FX hedging delivers: Outcomes and lessons

With a nuanced view on challenges, let's spotlight the positive outcomes and performance data from effective FX hedging.

The numbers are compelling. Companies with FX hedging see 23-45% less cash flow volatility and 30-50% greater earnings stability compared to unhedged peers. Dynamic strategies that adapt to market conditions add measurable value beyond static approaches.

Key outcomes from well-executed programs include:

- Smoother earnings per share (EPS): Reduced FX noise makes financial results more predictable for investors and analysts.

- Better budgeting accuracy: When you know your hedge rate, you can build budgets with confidence rather than wide scenario ranges.

- Improved credit profile: Lenders and rating agencies view stable cash flows favorably, which can reduce borrowing costs.

- Operational focus: Management spends less time reacting to currency swings and more time on core business decisions.

"The real value of hedging is not the rate you lock in. It is the planning certainty you gain."

Lessons from real-world application point to a few consistent themes. First, optimizing the hedge horizon matters more than most teams realize. Hedging 100% of a 24-month exposure is often counterproductive because forecast accuracy degrades sharply beyond 6-12 months. A rolling, layered approach, where you hedge more of the near-term exposure and less of the long-term, tends to outperform all-or-nothing strategies.

Second, adapt as volatility shifts. A strategy calibrated for a low-volatility environment can become too expensive or too thin when market regimes change. Mitigating FX volatility effectively requires periodic recalibration, not a set-and-forget mindset.

Third, accounting for currency risk properly ensures that the economic benefits of hedging are reflected in your reported financials, not obscured by mark-to-market noise on derivative positions.

Our perspective: Why standard FX hedging advice falls short

Most FX hedging guides stop at instrument selection. They tell you what a forward is, list the pros and cons of options, and send you on your way. That is useful, but it misses the most important insight: the market regime you are in determines whether your strategy works, not just the instrument you chose.

Static, set-and-forget hedging programs were designed for a world of relatively stable volatility and predictable rate trends. That world is increasingly rare. Currency markets in 2026 are shaped by geopolitical shocks, central bank divergence, and commodity price swings that can flip volatility regimes in weeks. A fixed hedge ratio calibrated in January can be dangerously wrong by March.

Dynamic and active approaches, including momentum signals, carry adjustments, and purchasing power parity overlays, consistently outperform static strategies when regimes shift. The implication is clear: treat FX hedging as a living process, not a one-time setup.

Our advice is to build in a quarterly review cadence at minimum. Use that review to assess whether your current hedge ratio, instrument mix, and horizon still fit the exposure profile and market environment. Adjust prevention methods for FX volatility proactively rather than reactively. The teams that do this consistently outperform those that revisit their hedging policy only after a painful quarter.

How CorpHedge simplifies FX hedging for your business

If your team is ready to operationalize these lessons, discover how CorpHedge makes professional FX hedging accessible.

CorpHedge is built for finance and risk management professionals who need more than a spreadsheet. The platform gives you real-time visibility into your currency positions, Value at Risk calculations, and automated strategy execution, all in one place. You can explore the full suite of FX exposure management features to see how forecasting, policy compliance, and hedge accounting support are integrated. Whether you are running a static forward program or a dynamic overlay strategy, CorpHedge helps you move from reactive to proactive currency risk management. Request a custom demo to see how it fits your specific exposure profile and reporting requirements.

Frequently asked questions

What is the difference between static and dynamic FX hedging?

Static hedging locks in a fixed hedge ratio at the start of a period and does not change it, while dynamic hedging adjusts coverage as market conditions and volatility shift. Dynamic hedging outperforms static when currency regimes change significantly.

How effective is FX hedging for reducing company risk?

Very effective when properly structured. Hedging reduces volatility by 23-45% and improves earnings stability by up to 50% compared to unhedged peers.

What are the main risks involved in FX hedging?

Basis risk in futures can reach 5.9%, swaps carry significant counterparty credit risk, and hedge accounting requires formal documentation and ongoing effectiveness testing.

Is FX hedging allowed for all companies worldwide?

Not universally. US retail direct hedging is banned under CFTC rules, and requirements differ by jurisdiction, so always verify local regulations with your legal and compliance teams before launching a program.

Can FX hedging eliminate all currency risk?

No. Perfect hedges are rare and often prohibitively expensive. Residual risks like basis risk, liquidity risk, and forecast error always remain, which is why hedge ratios below 100% are standard practice.