TL;DR:

- Foreign currency exposure can quietly erode profit margins before your team notices, especially in daily international operations.

- Understanding and applying the appropriate currency exchange accounting framework, such as IAS 21 or ASC 830, is essential to accurately measure and report financial impacts.

Foreign currency exposure can quietly destroy margins before your team even notices. A subsidiary booking revenue in euros while reporting in dollars, a supplier invoice settled 60 days after the spot rate moved 5 percent — these are not edge cases. They are the daily reality of international operations. Currency exchange accounting is the discipline that keeps these exposures visible, measurable, and defensible. This guide breaks down the two dominant frameworks, explains where gains and losses actually land in your statements, and gives you practical strategies to reduce volatility before it hits your bottom line.

Table of Contents

- Understanding currency exchange accounting frameworks

- Core concepts: Transaction, translation, and remeasurement

- Special challenges: Hyperinflation, functional currency, and edge cases

- Hedge accounting: Minimizing volatility from FX swings

- Practical applications: Real-world FX strategies and lessons from global companies

- Why most finance teams miss the real benefits of currency exchange accounting

- How CorpHedge can help you master currency exchange accounting and FX risk management

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Framework matters | Knowing the differences between IFRS and US GAAP is critical for accurate foreign currency accounting. |

| Remeasurement and translation | Applying the correct process for each currency item reduces reporting errors and surprises. |

| Hyperinflation handling diverges | IFRS and US GAAP take very different approaches to hyperinflation—review country-specific guidance closely. |

| Hedge accounting offers real risk control | Documented hedge accounting, especially hybrid strategies, can cut FX profit volatility by over 30 percent. |

| Continuous monitoring is key | Regularly reviewing exposures and updating practices makes FX accounting a strategic asset, not just a compliance task. |

Understanding currency exchange accounting frameworks

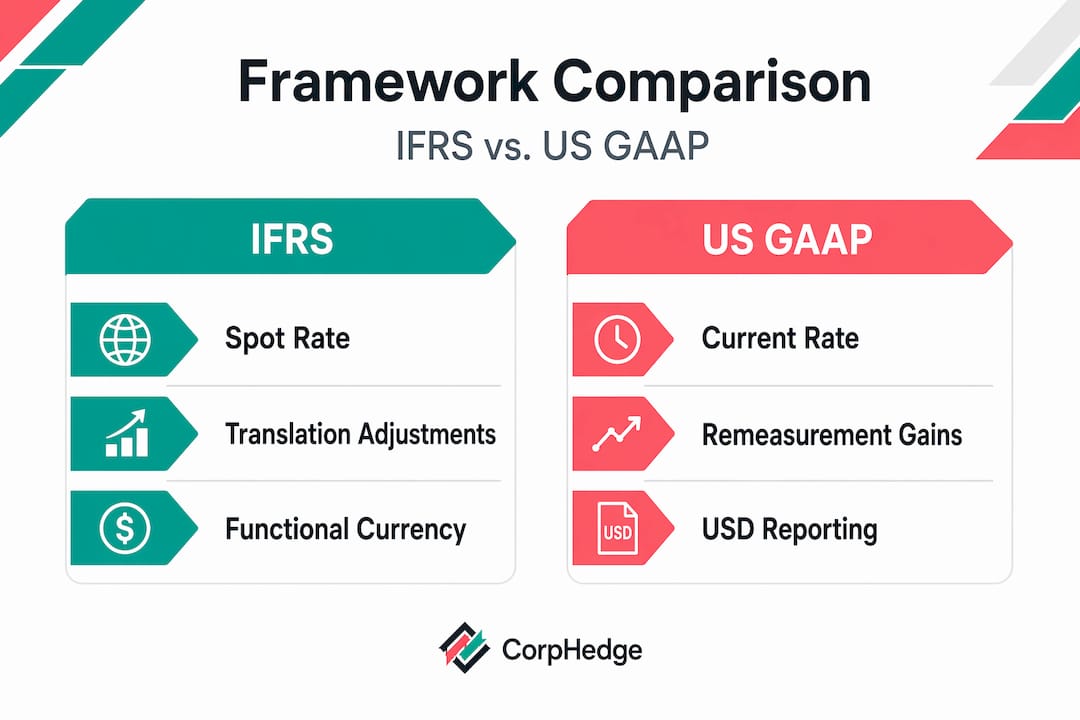

The first question most finance teams get wrong is not "how do we record this?" but "which framework governs us, and what does it actually require?" Two standards dominate global practice: IAS 21 under IFRS and ASC 830 under US GAAP. They share a common goal but diverge in ways that materially affect reported earnings.

Under IAS 21, foreign currency transactions are recorded at the spot rate on the transaction date. Unsettled monetary items are retranslated at the closing rate, with differences flowing to profit or loss. For foreign operations, assets and liabilities are translated at the closing rate, income and expenses at average or transaction rates, and translation differences go to other comprehensive income (OCI).

Under ASC 830, remeasurement applies to transactions in a non-functional currency: monetary items use the current rate with gains and losses hitting net income directly, while non-monetary items stay at historical rates. Translation for foreign entities follows the current rate method for the balance sheet, with the adjustment captured in OCI.

| Feature | IAS 21 (IFRS) | ASC 830 (US GAAP) |

|---|---|---|

| Transaction recording | Spot rate at transaction date | Spot rate at transaction date |

| Unsettled monetary items | Closing rate, P&L | Current rate, P&L |

| Non-monetary items | Historical rate | Historical rate |

| Translation adjustment | OCI | OCI |

| Remeasurement gains/losses | P&L | P&L |

| Hyperinflation treatment | IAS 29 restatement | Remeasure to USD |

The practical differences matter most when you operate across frameworks. A European parent with a US subsidiary must understand IFRS vs US GAAP divergences to avoid misclassifying translation adjustments as earnings. Pairing your accounting framework with solid currency management strategies is the only way to keep both compliance and risk management aligned.

Pro Tip: Document your functional currency determination judgment in writing, including the factors considered and the data reviewed. Auditors increasingly scrutinize this, and a well-documented rationale prevents restatements.

Core concepts: Transaction, translation, and remeasurement

These three processes sound interchangeable. They are not, and confusing them is one of the most common sources of misstated financials in multinational reporting.

Transaction recording captures a foreign currency event at the spot rate on the date it occurs. Remeasurement then adjusts monetary balances when the functional currency differs from the transaction currency, with gains and losses recognized immediately in profit or loss. Translation converts an entire foreign subsidiary's financials into the parent's reporting currency, with differences parked in OCI rather than earnings.

Here is how a standard sequence works in practice:

- A US manufacturer sells goods to a German buyer for €500,000. The invoice is recorded at the EUR/USD spot rate on the sale date.

- At quarter-end, the receivable is remeasured at the closing rate. If the euro weakened, a remeasurement loss hits the income statement.

- When the German subsidiary's full financials are translated into USD for consolidation, the translation adjustment goes to OCI, not earnings.

The IFRS vs US GAAP comparison shows that while both standards route translation adjustments to OCI, remeasurement gains and losses under US GAAP hit the income statement directly. IFRS draws a cleaner line between transaction and translation effects. Hyperinflation handling diverges even further, which we cover in the next section.

Two pitfalls appear repeatedly in practice. First, teams double-count by recording both a remeasurement gain and a translation adjustment on the same balance. Second, non-monetary items like inventory or fixed assets are incorrectly remeasured at current rates instead of historical rates. Using forex derivatives tools alongside your accounting process helps flag these mismatches before close. Building this into your strategic risk management framework turns a reactive process into a proactive one.

Pro Tip: During high-volatility periods, use actual transaction-date rates rather than monthly averages. A 3 percent intra-month swing can materially distort reported results if you rely on averages.

Special challenges: Hyperinflation, functional currency, and edge cases

Standard rules hold until the economic environment breaks them. Hyperinflationary economies and ambiguous functional currency situations are where even experienced teams lose ground.

Under IFRS, IAS 29 requires restating financials using a general price index before translation. Under ASC 830, US GAAP takes a different path: the entity remeasures directly into USD as the functional currency, pushing gains and losses into the income statement. Recent IAS 21 amendments address a specific edge case where a non-hyperinflationary functional currency entity presents in a hyperinflationary reporting currency. All amounts, including comparatives, must be translated at the closing rate. This is a meaningful departure from standard translation treatment.

The divergence between standards creates real volatility. In hyperinflationary economies, IFRS restatement and US GAAP remeasurement produce materially different equity balances and earnings figures, complicating cross-border comparisons and investor communications.

Red flags that edge case guidance may apply:

- Your entity operates in a country with cumulative three-year inflation exceeding 100 percent

- The functional currency determination is contested between local and parent management

- Significant intercompany transactions exist between entities with different functional currencies

- A recent acquisition brought in subsidiaries with undocumented historical rates for non-monetary assets

- Your reporting currency differs from your functional currency in a high-inflation market

Proactive documentation and a clear process for managing currency fluctuations are non-negotiable when any of these flags appear.

"The functional currency is not always obvious. When a subsidiary sources inputs locally but invoices in USD, reasonable people can disagree — and auditors will push back without documented evidence."

Hedge accounting: Minimizing volatility from FX swings

Accurate reporting is necessary. Reducing the volatility you are reporting is better. Hedge accounting under IFRS 9 and ASC 815 lets you align the timing of gains and losses on hedging instruments with the exposures they cover, smoothing out the swings that would otherwise hit your income statement.

IFRS 9 hedge accounting replaced IAS 39 with a principle-based model. Effectiveness is assessed on an economic relationship basis rather than the rigid 80 to 125 percent test. Hedge types include fair value hedges, cash flow hedges, and net investment hedges. Critically, IFRS 9 allows a broader range of hedged items and groups than US GAAP, giving finance teams more flexibility to align accounting with actual risk management activity.

Common instruments and when to use them:

- Forward contracts: Best for fixed, known exposures like confirmed purchase orders. Lock in the rate and eliminate uncertainty.

- Options: Useful when exposure is probable but not certain. You pay a premium but retain upside if rates move favorably.

- Cross-currency swaps: Suited for long-term debt denominated in foreign currencies. Converts both principal and interest into the functional currency.

Hybrid hedging strategies combining forwards, options, swaps, and operational hedges reduce volatility by 30 to 40 percent. Dynamic monitoring is the critical variable. A hedge that was effective at inception can drift out of alignment as exposures change, and failing to update your hedge ratios is one of the most common causes of hedge discontinuation.

Explore mitigating FX risk through layered instruments, review hedging best practices for 2026 conditions, and consider how reducing earnings volatility through accounting-aligned hedging changes how your results read to investors.

Pro Tip: Under IFRS 9, you can voluntarily discontinue a hedge relationship without restating prior periods. Use this strategically when your risk profile changes, but document the rationale before you act, not after.

Practical applications: Real-world FX strategies and lessons from global companies

Theory only takes you so far. The most instructive data comes from companies that have already absorbed the lessons you are trying to avoid.

Empirical research on Chinese multinationals shows that manufacturing-sector companies carry significantly higher FX exposure than their US counterparts, but also demonstrate stronger hedging effectiveness. Forward contracts reduce short-term FX risk by approximately 1 percent for every 1 percent increase in derivatives usage. The implication: hedging works, but scale and consistency matter.

Rolling out a multi-layer hedging program:

- Map all currency exposures by entity, currency pair, and time horizon.

- Classify exposures as transactional, translational, or economic.

- Select instruments matched to each exposure type and duration.

- Document hedge relationships and effectiveness methodology before execution.

- Set a quarterly review cadence to adjust hedge ratios as exposures shift.

- Integrate FX data into your management reporting so leadership sees exposure in real time.

The most common mistake is overreliance on a single instrument. A company that only uses forward contracts is fully protected on rate but exposed to opportunity cost when rates move favorably. Diversifying FX trading across instrument types and time horizons is the same logic applied to hedging programs.

For sector-specific guidance, review transaction hedging strategies and the top risk management strategies that consistently outperform single-tool approaches.

Why most finance teams miss the real benefits of currency exchange accounting

Here is the uncomfortable truth: most finance teams treat currency exchange accounting as a compliance exercise and stop there. They book the gains and losses, file the disclosures, and move on. The companies that actually protect their margins do something different. They use the accounting output as a signal, not a conclusion.

The data in your translation adjustments and remeasurement lines tells you where your economic exposure is concentrated. Ignoring that signal because "it goes to OCI anyway" is how companies absorb losses that were entirely predictable. The OCI balance is not a parking lot. It is a deferred income statement entry waiting for a triggering event.

Corporate inertia is the second problem. FX strategies get set during budget season and rarely revisited until a quarterly surprise forces a conversation. Currency markets do not respect annual planning cycles. A hedge program designed for 2025 conditions may be actively harmful in mid-2026 if you have not reviewed your exposure map.

The teams that consistently outperform build FX risk culture across functions, not just in treasury. Sales teams that price contracts in foreign currencies without treasury input create exposures that no hedge program can fully offset. Procurement teams that lock in supplier contracts denominated in volatile currencies without escalating to finance are doing the same. Review FX risk management tips built for CFOs who want to move beyond reactive reporting.

True mastery of foreign exchange accounting is not about perfect bookkeeping. It is about using what the books tell you to make better decisions faster than your exposure can move against you.

How CorpHedge can help you master currency exchange accounting and FX risk management

If the frameworks, hedge accounting rules, and real-time exposure monitoring described in this article feel like a lot to manage manually, that is because they are. Most finance teams are running sophisticated FX programs on spreadsheets and quarterly check-ins, which is exactly where the gaps appear.

CorpHedge gives international finance teams a single platform to track live FX exposure, model hedge scenarios using value at risk hedging, and align accounting treatment with actual risk management activity. The platform connects directly to your existing workflows, so your treasury and accounting functions are working from the same data. Take a look at the full product tour to see how the tools work in practice, or explore the complete list of FX exposure management features to find what fits your current setup. The gap between compliance and control is smaller than you think when you have the right infrastructure.

Frequently asked questions

What is the difference between translation and remeasurement in currency accounting?

Translation converts a foreign entity's full financial statements into the parent's reporting currency, with differences going to OCI. Remeasurement adjusts non-functional currency balances into the functional currency and hits profit or loss directly under both standards.

How do you choose the functional currency for an entity?

The functional currency reflects the primary economic environment where the entity operates and generates cash. IAS 21 requires judgment when indicators conflict, and that judgment must be documented to withstand audit scrutiny.

What are the main challenges of accounting in hyperinflationary economies?

IFRS restates financials using a general price index under IAS 29, while US GAAP remeasures into USD, pushing gains and losses into the income statement and producing materially different equity balances across frameworks.

How can hedge accounting reduce the impact of currency swings?

Hedge accounting aligns the timing of gains and losses on hedging instruments with the underlying exposures. IFRS 9's principle-based model covers fair value, cash flow, and net investment hedges, reducing reported income statement volatility when applied correctly.

What is a practical first step to start managing FX risk in global operations?

Map your exposures by currency pair and time horizon, then match instruments to each exposure type. Hybrid hedging programs combining forwards, options, and swaps consistently reduce volatility by 30 to 40 percent compared to single-instrument approaches.