TL;DR:

- Currency risk can significantly damage margins, cash flow, and competitive positioning if unmanaged.

- Managing FX exposure involves identifying transaction, translation, and economic risks, with a focus on transaction and translation.

- Effective FX management requires tailored strategies, strong governance, and integration with business operations.

Currency risk is one of the most underestimated threats on a corporate balance sheet. Many senior finance teams assume that size, diversification, or operating in "stable" currency pairs provides natural insulation from FX shocks. It does not. In fact, FX derivatives reduce cash-flow variance by 8 to 12% for highly exposed firms, which means unhedged companies are absorbing volatility they could systematically eliminate. This guide breaks down what leading finance teams actually do, why structured FX management is non-negotiable, and how to build a framework that protects both profitability and forecasting accuracy.

Table of Contents

- What is FX exposure and why does it matter?

- Common methodologies for managing FX exposure

- Strategic trade-offs: How much hedging is right?

- Governance and best practices in FX risk management

- Our perspective: Why a tailored approach to FX exposure truly matters

- Take your FX risk management to the next level with CorpHedge

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| FX management cuts risk | Active FX exposure management can reduce cash-flow variance and volatility. |

| Strategy fit trumps size | Tailoring your approach to business needs is more effective than copying generic practices. |

| Governance is critical | A robust policy, clear accountability, and regular reviews are key to FX risk success. |

| Method mix matters | Combining natural and financial hedges offers resilience and cost control. |

What is FX exposure and why does it matter?

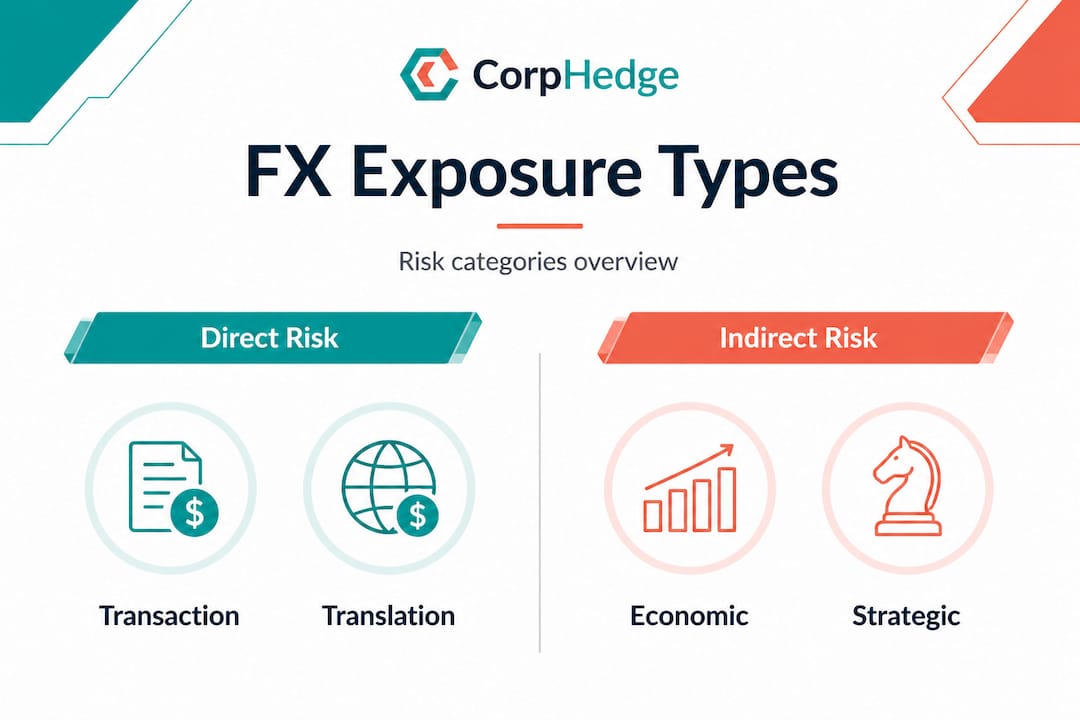

FX exposure is not a single, monolithic risk. It comes in three distinct forms, and misidentifying which one you face is one of the most common and costly mistakes in corporate treasury.

Transaction exposure arises when a company has contractual cash flows in a foreign currency, such as a receivable from a European customer or a payables obligation to an Asian supplier. Until those flows are settled, your company is exposed to rate movements that could increase costs or shrink revenues in your home currency. This is the most immediate form of exposure and typically the easiest to hedge.

Translation exposure (sometimes called accounting exposure) occurs when a multinational consolidates financial statements. Subsidiaries reporting in local currencies create balance sheet and income statement effects when converted to the parent's reporting currency. A strong dollar, for example, can significantly reduce the reported revenue of a U.S. parent with substantial euro zone operations, even if the underlying business performed well.

Economic exposure is the most subtle and the hardest to manage. It reflects how currency shifts alter a company's long-term competitive position. If a competitor's home currency weakens, they can undercut your pricing in shared markets. As BIS research confirms, corporates should focus primarily on transaction and translation exposure, since economic exposure is notoriously difficult to hedge through financial instruments alone.

Why does any of this actually matter? Consider a mid-size manufacturer selling into Latin America with USD-denominated contracts. A 10% depreciation in the Brazilian real, the Mexican peso, or the Colombian peso can erode the entire margin on those sales almost overnight. No operational efficiency improvement will compensate that fast. The effects are real, immediate, and highly damaging if left unmanaged.

The main risks of unmanaged FX exposure include:

- Margin erosion from adverse rate moves between contract signing and payment

- Cash flow volatility that disrupts working capital planning and supplier payments

- Forecasting uncertainty that undermines budgeting and board-level reporting

- Balance sheet distortion from translation adjustments that affect credit ratios

- Competitive disadvantage if currency-exposed costs rise while a competitor's do not

Understanding the FX risk types you face is the essential first step. Without that clarity, any hedging you do is essentially guesswork.

Common methodologies for managing FX exposure

Once you understand your exposure profile, the next question is how to address it. There is no universal answer. The right approach depends on your business model, the currencies involved, your liquidity position, and your organization's risk appetite.

Here is a practical comparison of the most widely used methodologies, drawing from recognized corporate FX frameworks:

| Method | Best suited for | Key advantage | Main limitation |

|---|---|---|---|

| Natural hedging | Firms with matched inflows/outflows | Zero instrument cost | Requires operational restructuring |

| Forward contracts | Known, fixed future cash flows | Full price certainty | No upside if rates move favorably |

| FX options | Uncertain exposure size or timing | Flexibility and upside protection | Premium cost can be significant |

| Cross-currency swaps | Long-term liabilities in foreign currency | Converts debt profile cleanly | Complexity and counterparty risk |

| Dynamic hedging | Volatile or unpredictable exposure | Adapts to changing conditions | Requires robust systems and expertise |

Natural hedging involves structuring business operations so that foreign currency revenues and costs offset each other organically. A U.S. company that earns euros and also sources materials from Europe is naturally hedging part of its euro exposure. This approach costs nothing in terms of financial instrument premiums, which makes it a highly attractive first option.

Forward contracts lock in an exchange rate for a future transaction. If you know you will receive 5 million euros in 90 days, a forward allows you to fix the conversion rate today. The certainty is valuable for budgeting, but you also forgo any gain if the euro strengthens before settlement.

FX options give you the right but not the obligation to exchange currency at a predetermined rate. They are particularly useful when your exposure is uncertain in size or timing, such as when you are bidding on international contracts that may or may not be awarded. The downside is premium cost.

Cross-currency swaps are primarily used to manage long-duration exposures, such as when a company issues debt in a foreign currency to access cheaper credit and then swaps the obligation back to its home currency for accounting and cash flow management purposes.

Pro Tip: Before reaching for financial instruments, audit your natural hedging opportunities first. Matching foreign currency costs to revenues, invoicing in your home currency where you have pricing power, or shifting production to reduce cross-currency procurement costs can meaningfully reduce gross exposure. Every unit of exposure eliminated naturally is one less unit to hedge with financial instruments, and that directly reduces your hedging costs.

For organizations ready to move beyond the basics, advanced FX hedging strategies including dynamic hedge ratio adjustment and overlay programs can provide additional precision. A step-by-step grounding in proven steps for currency risk will also help you sequence your approach correctly.

Strategic trade-offs: How much hedging is right?

This is where the conversation gets genuinely nuanced, and where many corporate finance teams either under-act or over-engineer their programs.

The empirical case for hedging is strong. Research shows that currency hedging added roughly 2.5% in annual return and reduced volatility by approximately 3% over a decade for EAFE equity portfolios. For cash-intensive operating companies, the argument is even more compelling, since FX derivatives reduce cash-flow variance significantly in highly exposed industries.

But not every firm should hedge everything. Consider this data comparison across a 10-year horizon for international equity portfolios:

| Metric | Hedged portfolio | Unhedged portfolio |

|---|---|---|

| Annualized return | ~2.5% higher | Lower due to FX drag |

| Volatility | ~3% lower | Higher from currency noise |

| Downside in crisis years | Meaningfully cushioned | Full FX impact absorbed |

| Cost impact | Hedging costs deducted | No direct instrument cost |

However, JPMorgan's FX hedging framework raises a legitimately contrarian point:

"When asset volatility significantly exceeds FX volatility, the incremental benefit of hedging diminishes; some academics argue that currency movements mean-revert over long horizons, reducing the risk reduction benefit of permanent hedges for long-horizon investors."

For corporate finance professionals, the key takeaway is not to dismiss hedging but to size it correctly. A company with 80% of revenues in its home currency and only 20% in foreign markets may find that a 100% hedge ratio on foreign receivables is disproportionate to the actual balance sheet risk. Conversely, an exporter with 60% of revenues in foreign currencies who operates on thin margins cannot afford to leave any material exposure unhedged.

To determine your optimal hedge ratio, work through these steps:

- Quantify total gross exposure by currency pair, maturity, and business unit.

- Identify natural offsets already embedded in your operating model.

- Assess your risk appetite in terms of acceptable variance in reported earnings and cash flow.

- Model the cost of different hedge ratios, including instrument premiums and administrative overhead.

- Review currency risk governance requirements and align hedge ratios with your board-approved policy.

- Set a review cadence to adjust the ratio as business conditions, market volatility, and competitive dynamics evolve.

The goal is not zero FX impact. That is often too expensive and operationally inflexible. The goal is a predictable, manageable impact that your business can plan around.

Governance and best practices in FX risk management

Even the most technically sophisticated hedge program will underdeliver if the governance around it is weak. This is where the gap between large multinationals and mid-market companies is often largest, not in access to instruments, but in the rigor of policy, oversight, and execution.

Expert guidance consistently emphasizes a clear hierarchy: prioritize natural hedges first because they are cheaper, then layer in financial instruments only for residual exposure. Dynamic strategies that adjust in response to volatility can add value, but they require robust systems and governance infrastructure to function correctly. Without that foundation, dynamic hedging creates operational risk as fast as it reduces market risk.

Key governance requirements for any serious FX risk program include:

- A written FX policy approved at board or CFO level, covering which exposures to hedge, which instruments are permitted, and who has authority to execute

- Defined hedge ratios and limits by currency, tenor, and instrument type

- Clear segregation of duties between those who identify exposure, those who authorize trades, and those who report results

- Regular measurement and reporting, at minimum monthly, with real-time dashboards for high-volatility environments

- Annual policy review with a formal process for updating the policy in response to business changes, market structure shifts, or regulatory developments

Common pitfalls that undermine otherwise well-designed programs include:

- Over-hedging, where hedge positions are larger than the underlying exposure they are meant to protect

- Using complex instruments without adequate internal expertise or system support to manage them properly

- Poor communication between treasury, accounting, and business unit leaders, leading to misaligned expectations about what hedging does and does not accomplish

- Treating FX management as a treasury-only function rather than integrating it with commercial strategy and pricing decisions

Pro Tip: Build flexibility into your hedge policy from the start. Markets change faster than most annual policy cycles can accommodate. A policy that requires escalation to the board for any deviation will paralyze your treasury team during the exact moments when fast action matters most. Define pre-approved adjustment ranges so your team can respond without bureaucratic delay.

Exploring FX risk management basics alongside currency fluctuation best practices can help your team build a governance framework that is both rigorous and practical.

Our perspective: Why a tailored approach to FX exposure truly matters

Here is what most generic guidance misses: the failure mode in corporate FX management is rarely a lack of knowledge about instruments. It is the assumption that a hedging template that works for one company automatically transfers to another.

We have seen large multinationals with sophisticated treasury teams systematically over-hedge because their policies were written to satisfy auditors, not to reflect actual business risk. We have also seen mid-market exporters leave enormous margin risk unmanaged because they assumed hedging was only for big companies with big teams. Both are expensive mistakes born from the same root cause: a program that is not designed for the specific business it serves.

The cultural and communication dimension is almost entirely missing from textbook treatments of FX risk. A hedge program is only as effective as the business unit managers who understand what it does and provide accurate forecasting inputs to treasury. If your commercial team does not understand why the FX hedging line item appears in their P&L, or if they change deal terms without notifying treasury, your hedge book quickly becomes disconnected from reality. This happens constantly, in companies of every size.

Dynamic adjustment also offers more upside than most firms realize, but only when it is grounded in a clear view of actual business conditions. A treasury team that adjusts hedge ratios mechanically based on volatility signals without consulting the underlying commercial pipeline is just adding complexity without adding value.

The firms that consistently outperform on FX management are those that treat global currency management strategies as a cross-functional discipline, not a treasury silo. They connect hedge decisions to pricing strategy, customer contract terms, and operational footprint decisions. That integration is what separates programs that protect value from programs that just generate reports.

"A tailored FX strategy, aligned to the specific exposure profile and commercial realities of the business, consistently outperforms any off-the-shelf template, regardless of how sophisticated that template appears."

Take your FX risk management to the next level with CorpHedge

Applying these principles at scale requires more than spreadsheets and manual tracking. The complexity of real-time exposure monitoring, dynamic hedge ratio management, and policy enforcement demands purpose-built infrastructure.

CorpHedge gives corporate finance teams the tools to model risk, monitor live currency positions, and enforce hedge policy with precision. The platform's hedging based on value at risk capabilities allow you to size hedge programs relative to your actual risk budget, not just rule-of-thumb percentages. If you want to see exactly how the platform addresses the governance, execution, and monitoring challenges covered in this article, explore the full FX exposure management features or walk through the FX risk management solutions to see it in action.

Frequently asked questions

What are the main benefits of managing FX exposure?

Managing FX exposure reduces cash flow volatility and protects profitability, with empirical data showing that FX derivatives reduce cash-flow variance by 8 to 12% for highly exposed firms.

Is full hedging always the best approach for corporations?

Not always. Academic research argues that full hedging can be suboptimal when hedging costs are high or when currencies tend to mean-revert over longer horizons, making partial or selective hedging the smarter choice for many firms.

How do natural hedges compare to financial instruments for FX risk?

Natural hedges cost nothing to implement in terms of instrument premiums and should be the first priority, but they require operational changes and provide limited flexibility compared to financial instruments that can be sized and timed precisely.

How often should FX risk policies be reviewed?

FX risk policies should be reviewed formally at least once per year, and additionally whenever there are significant shifts in market volatility, business structure, or the company's exposure profile.

What's the most common mistake in managing FX exposure?

Over-hedging and deploying dynamic strategies without adequate governance or system support are the most frequent and costly errors, often creating operational risk that outweighs the market risk being managed.