TL;DR:

- Measuring FX risk exposure involves quantifying currency fluctuations' impact on a company's financials across international markets. Accurate identification requires separating transaction, translation, and economic exposures and using comprehensive data from multiple systems. Combining VaR and EaR metrics within a structured framework enables effective risk management and strategic decision-making.

Measuring FX risk exposure is the process of quantifying the potential financial impact that currency rate fluctuations can have on a company's cash flows, earnings, and balance sheet across international operations. For corporate treasury teams managing multi-currency positions in markets from the U.S. to Poland and Sweden, this process relies on structured frameworks built around metrics like Value at Risk (VaR) and Earnings at Risk (EaR). Getting it right is not optional. Currency volatility can erode margins faster than most operational risks, and the difference between a well-measured exposure and a rough estimate is often the difference between a hedged position and an unpleasant earnings surprise.

What are the different types of FX exposure and why does it matter to separate them?

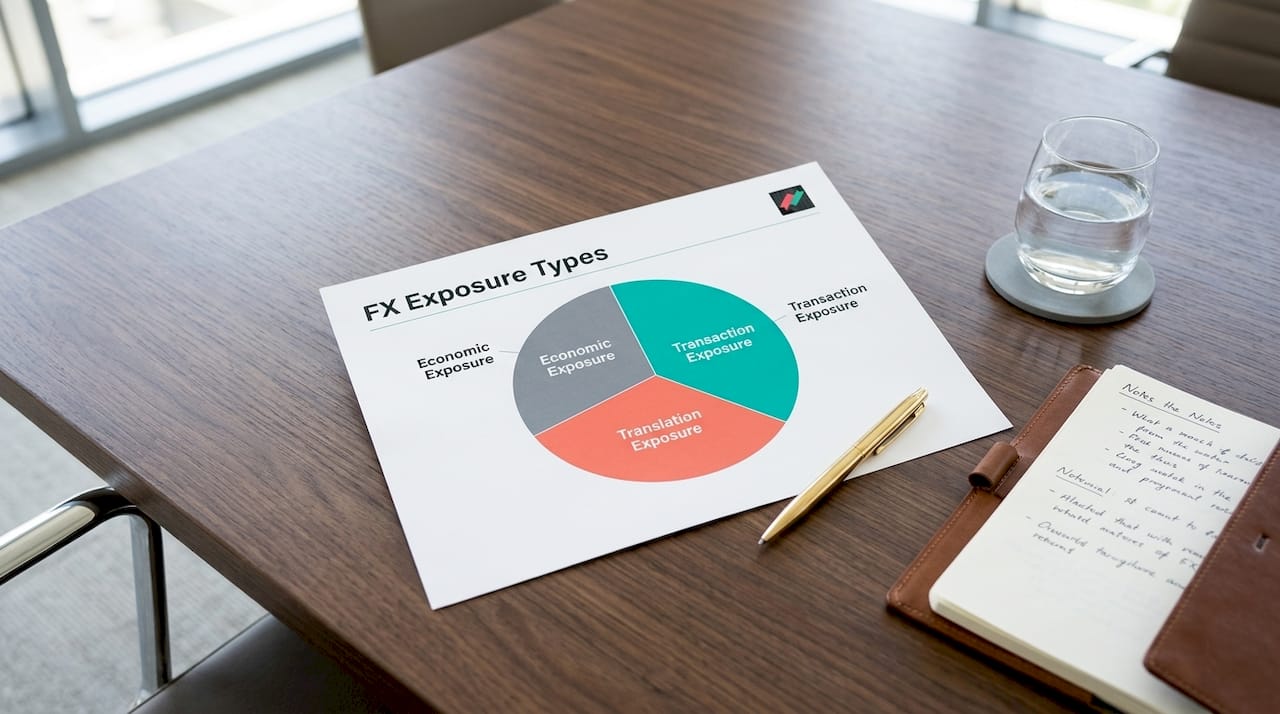

Foreign exchange risk, formally called currency exposure in treasury practice, splits into three distinct categories: transaction exposure, translation exposure, and economic exposure. Each requires different data sources, measurement methods, and hedging responses. Conflating these types leads directly to measurement errors and hedges that protect the wrong thing.

Transaction exposure covers cash flows that are already contracted in a foreign currency. A U.S. manufacturer invoicing a German buyer in euros faces transaction exposure from the moment the invoice is issued until payment clears. This is the most straightforward type to identify and the most commonly hedged using forward contracts or options.

Translation exposure arises when a parent company consolidates the financial statements of foreign subsidiaries. A Swedish subsidiary reporting in SEK creates a translation exposure for a U.S. parent when the SEK/USD rate moves between reporting periods. This does not affect cash directly, but it does affect reported earnings per share and book equity, which matters to investors and analysts.

Economic exposure is the hardest to measure. It reflects how exchange rate shifts alter a company's long-term competitive position. A Polish manufacturer competing against German rivals faces economic exposure if the PLN strengthens, because its cost base rises relative to euro-zone competitors even without a single foreign-currency invoice. This type requires scenario modeling over multi-year horizons, not just spot rate sensitivity.

- Transaction exposure: contractual, short-term, directly hedgeable

- Translation exposure: accounting-driven, affects reported financials, partially hedgeable

- Economic exposure: strategic, long-term, requires scenario analysis and business model review

Cross-functional data integration from ERP systems, FP&A models, and accounting platforms is critical for accurate exposure identification across all three types. Treasury teams that rely only on treasury management system data typically miss economic and translation exposures entirely.

Pro Tip: Build a currency exposure register that tags each exposure by type, business unit, and currency pair. This single document prevents the most common measurement failure: treating all FX risk as one number.

Which methodologies quantify FX risk exposure most effectively?

The most reliable approach to FX exposure analysis combines a net multi-currency exposure map with two complementary quantitative metrics: Value at Risk and Earnings at Risk. Neither metric alone tells the full story, but together they cover both the treasury and executive views of currency risk.

Building a net multi-currency exposure map

Start by aggregating all foreign-currency cash flows, balance sheet items, and forecast revenues by currency pair. Net long and short positions within each currency before calculating risk. A company with $10M in EUR receivables and $6M in EUR payables carries a net $4M EUR long position. That net figure is the input to every subsequent calculation.

Applying VaR and EaR to quantify risk

- Calculate Value at Risk (VaR). VaR quantifies the worst expected loss over a defined time horizon at a given confidence level. A one-month 95% VaR of $2.4M means losses would not exceed $2.4M in 95 out of 100 months. This gives treasury a concrete risk budget and a ceiling for hedging decisions.

- Calculate Earnings at Risk (EaR). EaR translates the same currency exposure into potential reported earnings impact over a business planning horizon, typically one fiscal year. Where VaR speaks to treasury, EaR frames currency risk in the earnings language that boards and CFOs actually use.

- Run sensitivity analyses. Stress-test net positions against 1%, 5%, and 10% rate moves for each major currency pair. A 5% EUR/USD move on a $4M net EUR position produces a $200,000 earnings swing. That figure, expressed as a percentage of operating income, immediately communicates materiality to non-treasury stakeholders.

- Integrate both metrics for governance. Using VaR and EaR together prevents the common miscommunication where treasury reports a comfortable risk position while the CFO is surprised by an earnings miss driven by the same exposure.

| Metric | Time horizon | Primary audience | Key output |

|---|---|---|---|

| Value at Risk (VaR) | Days to one month | Treasury, risk committee | Worst-case loss at confidence level |

| Earnings at Risk (EaR) | One fiscal year | CFO, board, FP&A | Earnings impact range from FX moves |

| Sensitivity analysis | Spot rate scenarios | All stakeholders | P&L impact per percentage rate move |

Pro Tip: When presenting to the board, lead with EaR expressed as a percentage of EBITDA. A $2.4M VaR figure is abstract. "Currency moves could reduce EBITDA by 4%" is a decision-forcing number.

Sophisticated treasury operations extend beyond these first-order measures. Fully robust measurement frameworks incorporate second-order sensitivity (gamma exposure) and tail risk metrics like Conditional Value at Risk (CVaR), which captures the expected loss beyond the VaR threshold. Most corporate treasury teams do not need gamma modeling, but multinationals with large options books or complex structured hedges do.

How do regulatory frameworks affect FX risk measurement?

Regulatory requirements add a layer of precision to FX exposure measurement that goes beyond internal management accounting. Under Basel III and the PRA's consultation framework, regulated financial institutions must calculate the FX sensitivity of net positions including foreign-currency credit risk risk-weighted assets (RWAs). This is not just a compliance exercise. It forces a level of measurement rigor that corporate treasury teams can learn from.

The PRA's framework for capitalizing FX positions introduces the concept of a maximum risk position, determined by combining FX delta sensitivity with foreign-currency credit risk RWAs. Firms can use alternative methods with PRA approval, but the default formula is designed to minimize the impact of FX rate moves on the capital ratio. For non-bank corporates, the lesson is structural: your exposure measurement should account for how currency moves affect not just cash flows but also balance sheet ratios and credit metrics.

Key regulatory and advanced measurement considerations include:

- FX delta measures the rate of change in portfolio value relative to a unit change in the spot rate. It is the foundation of any net risk position calculation.

- CVaR (Conditional VaR) captures the average loss in the worst-case tail beyond the VaR confidence level, giving a more conservative risk estimate for stress scenarios.

- Credit vs. non-credit RWA attribution matters for banks but also informs how corporates should think about currency-denominated debt and its interaction with FX exposure.

- Gamma exposure becomes relevant when a company holds FX options, because the delta of an option changes as the spot rate moves, creating non-linear risk.

"The maximum risk position for regulatory capital can be determined using FX delta sensitivity combined with foreign-currency credit risk RWAs, balancing complexity and precision." — Bank of England, PRA Consultation Paper, 2023

Corporate treasury teams expanding into regulated markets, including Poland and Sweden where local regulatory environments add currency-specific reporting requirements, need to align their measurement frameworks with both internal governance and external compliance standards from the outset.

What practical steps should treasury teams follow for accurate FX exposure measurement?

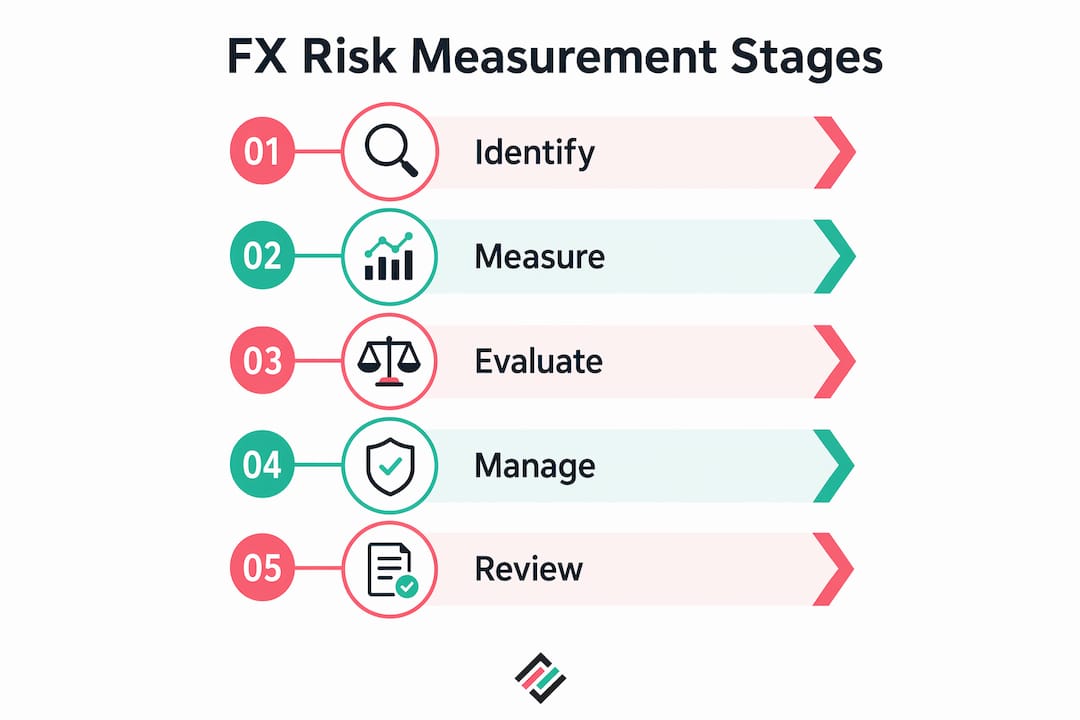

A structured four-stage framework covers the full cycle of FX risk measurement and management: identify exposures, measure with appropriate metrics, evaluate and select hedging instruments, then manage and review on an ongoing basis. Each stage has specific operational requirements that determine whether the framework produces reliable numbers or misleading ones.

Stage 1: Identify and map all exposures

Gather data from every system that touches foreign currency: ERP platforms, treasury management systems, accounts receivable and payable ledgers, and FP&A forecast models. Assign ownership by currency pair and business unit. Companies operating in multiple markets, including emerging markets like Poland where PLN volatility can be significant, need granular data at the entity level, not just consolidated group figures.

Stage 2: Measure with consistent data

Fragmented data systems and inconsistent exchange rate sources are the leading cause of measurement failure in corporate treasury. Budget rates, spot rates, and closing rates serve different purposes, but using them interchangeably in the same exposure model produces numbers that cannot be reconciled. Establish a single source of truth for exchange rate data, whether that is a Bloomberg feed, a Reuters data service, or a treasury platform with integrated rate management.

Stage 3: Evaluate and hedge

Apply VaR and EaR outputs to determine hedge ratios. A 75% hedge ratio on a $4M EUR exposure means covering $3M with forward contracts or options. The hedging decision should be driven by the measurement output, not by a fixed policy percentage that ignores current market conditions.

Stage 4: Manage, report, and review

Regular reporting on hedge coverage ratios and EaR supports audit readiness and strategic alignment. KPIs should include hedge effectiveness ratios, realized vs. forecast FX impact on earnings, and exposure coverage by currency pair. Policy reassessment at least annually, or after significant market events, keeps the framework calibrated to actual business conditions.

Pro Tip: Set up a real-time currency exposure dashboard that pulls from ERP and treasury systems daily. Stale exposure data is worse than no data, because it creates false confidence in hedge positions that no longer reflect actual risk.

Key takeaways

Accurate FX risk measurement requires separating exposure types, applying both VaR and EaR, and maintaining a single source of truth for exchange rate data across all business systems.

| Point | Details |

|---|---|

| Separate exposure types | Transaction, translation, and economic exposures require distinct data sources and measurement methods. |

| Use VaR and EaR together | VaR serves treasury risk budgeting; EaR communicates earnings impact to boards and CFOs. |

| Build a net exposure map | Aggregate and net all foreign-currency positions before applying any quantitative metric. |

| Standardize rate data | A single exchange rate source eliminates the reconciliation failures that undermine measurement accuracy. |

| Review and govern continuously | Hedge effectiveness testing and KPI monitoring keep measurement frameworks aligned with actual exposure. |

Why most treasury teams are measuring FX risk wrong

After working with treasury teams across multiple industries and geographies, the pattern I see most often is not a lack of tools. It is a failure of scope. Teams measure what is easy to see: open invoices, known payables, booked hedges. They miss the economic exposure sitting in their pricing models and the translation exposure accumulating in their Swedish or Polish subsidiary balance sheets.

The second failure is metric monoculture. A team that reports only VaR to its board is speaking a language the board does not fully understand. A team that reports only EaR to its risk committee is hiding the tail risk that VaR captures. The dual-metric approach is not theoretical best practice. It is the only way to have honest conversations at both the treasury and executive level simultaneously.

The regulatory environment is also moving faster than most corporate frameworks. The PRA's 2023 consultation on FX capitalization is a signal that regulators expect more precision in how firms attribute and measure currency risk, including the interaction between FX positions and credit risk RWAs. Corporate treasury teams that treat this as a banking problem are missing the direction of travel.

My practical recommendation: start with the exposure map. Every other measurement decision flows from knowing exactly what you own, in which currency, and at what maturity. Without that foundation, VaR and EaR are calculations applied to incomplete inputs, and incomplete inputs produce confident-looking numbers that are wrong.

— Bartas

How Corphedge helps treasury teams measure and manage FX exposure

Corphedge is built specifically for corporate treasury teams that need to move from exposure identification to active risk management without building a custom analytics stack. The platform provides real-time visibility into multi-currency positions, integrates VaR-based hedging strategies directly into the decision workflow, and supports the kind of cross-currency exposure mapping described throughout this article.

For treasury teams in Poland, Sweden, and other markets where currency volatility directly affects competitiveness, Corphedge delivers the measurement infrastructure that makes hedging decisions defensible and auditable. The platform connects exposure data to hedge execution, closing the gap between knowing your risk and acting on it. Explore the full FX risk management platform to see how Corphedge supports every stage of the measurement and management cycle.

FAQ

What is FX risk exposure measurement?

FX risk exposure measurement is the process of quantifying how currency rate changes affect a company's cash flows, earnings, and balance sheet. It uses metrics like VaR, EaR, and sensitivity analysis applied to net foreign-currency positions.

What are the three types of FX exposure?

The three types are transaction exposure (contracted cash flows in foreign currency), translation exposure (consolidation of foreign subsidiary financials), and economic exposure (long-term competitive impact of rate changes). Each requires separate measurement and management approaches.

How is Value at Risk used in FX risk measurement?

VaR calculates the maximum expected loss on a currency position over a defined period at a given confidence level. A one-month 95% VaR of $2.4M means losses will not exceed that figure in 95 out of 100 months, giving treasury a concrete risk budget.

Why do treasury teams need both VaR and EaR?

VaR quantifies worst-case loss for treasury risk management, while EaR translates the same exposure into earnings impact language that boards and CFOs use. Using both prevents miscommunication between treasury and executive stakeholders about the same underlying risk.

What causes FX exposure measurement to fail in practice?

The most common failures are fragmented data systems, inconsistent exchange rate sources across budgeting and actuals, and failure to separate transaction, translation, and economic exposures. A single source of truth for exposure data and a structured four-stage framework address all three problems.