TL;DR:

- Exchange rate risk erodes company margins due to currency fluctuations affecting international transactions.

- Managing FX risk involves mapping exposures, using hedging instruments, and establishing clear policies.

- Effective governance, portfolio approach, and real-time analytics are essential for successful risk mitigation.

When Volkswagen reported a €1.5 billion currency-related earnings hit in a single fiscal year, it wasn't a trading loss or an operational failure — it was exchange rate risk doing what it always does: quietly eroding margins until the damage is impossible to ignore. Exchange rate risk, also known as foreign exchange risk or currency risk, is the potential for financial loss due to fluctuations in currency exchange rates affecting international transactions, investments, or financial reporting. For corporate finance teams and risk managers at international companies, this isn't a peripheral concern. It sits at the center of every cross-border deal, every foreign subsidiary, and every multi-currency earnings report. This article defines exchange rate risk precisely, breaks down its three main types, quantifies its business impact, and outlines proven mitigation strategies.

Table of Contents

- What is exchange rate risk?

- Types of exchange rate risk

- How exchange rate risk impacts business performance

- Proven strategies to mitigate exchange rate risk

- A hard-earned perspective on exchange rate risk management

- Unlock streamlined FX risk management for your organization

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Clear risk definition | Exchange rate risk is the threat of loss from currency movements in international transactions. |

| Know the risk types | Understand transaction, translation, and economic risk to protect profits and reporting. |

| Industry exposure varies | Manufacturing firms face greater exchange rate sensitivity than service firms. |

| Effective mitigation | Robust risk management uses diversified hedges, analytics, and flexible policies. |

| Business impact is major | Unmanaged currency risk can erode margins, volatility, and competitiveness. |

What is exchange rate risk?

At its core, exchange rate risk is the exposure your company faces when the value of one currency changes relative to another, and that change affects your financial outcomes. According to Investopedia, exchange rate risk is "the potential for financial loss due to fluctuations in currency rates affecting international transactions, investments, or reporting." But limiting this to "potential loss" understates the full picture.

Exchange rate risk is a two-sided coin: yes, an adverse currency move can shrink your margins, but a favorable one that you failed to lock in is also a missed opportunity your competitors may have captured.

This matters because many corporate finance teams frame FX risk exclusively as a downside threat. In practice, a company that over-hedges during a favorable currency trend can leave significant revenue on the table while a less cautious rival reaps the benefit. True risk management accounts for both directions.

Why does this matter more now than ever? International business volumes have grown dramatically, and companies in sectors from automotive to pharmaceuticals routinely operate in 20 or more currency jurisdictions. Every contract denominated in a foreign currency, every overseas acquisition, and every royalty payment received in a non-functional currency creates exposure.

Typical corporate exchange rate exposures include:

- Contracts and receivables denominated in foreign currencies where payment is deferred

- Cross-border investments and acquisitions with assets held in non-home currencies

- Intercompany loans where principal and interest translate at fluctuating rates

- Financial reporting obligations requiring consolidation of foreign subsidiary results

- Commodity purchases priced in USD by companies reporting in other currencies

Understanding which of these exposures your organization carries is the first step. For a structured breakdown of each category, FX risk types explained offers a detailed framework that maps exposure categories to business functions.

One misconception worth dispelling: exchange rate risk is not simply the volatility of a currency pair on a given day. It is the interaction between that volatility and your company's specific financial positions. A company with zero cross-border transactions faces zero exchange rate risk, regardless of how volatile markets are. The risk is always relative to your exposure.

Types of exchange rate risk

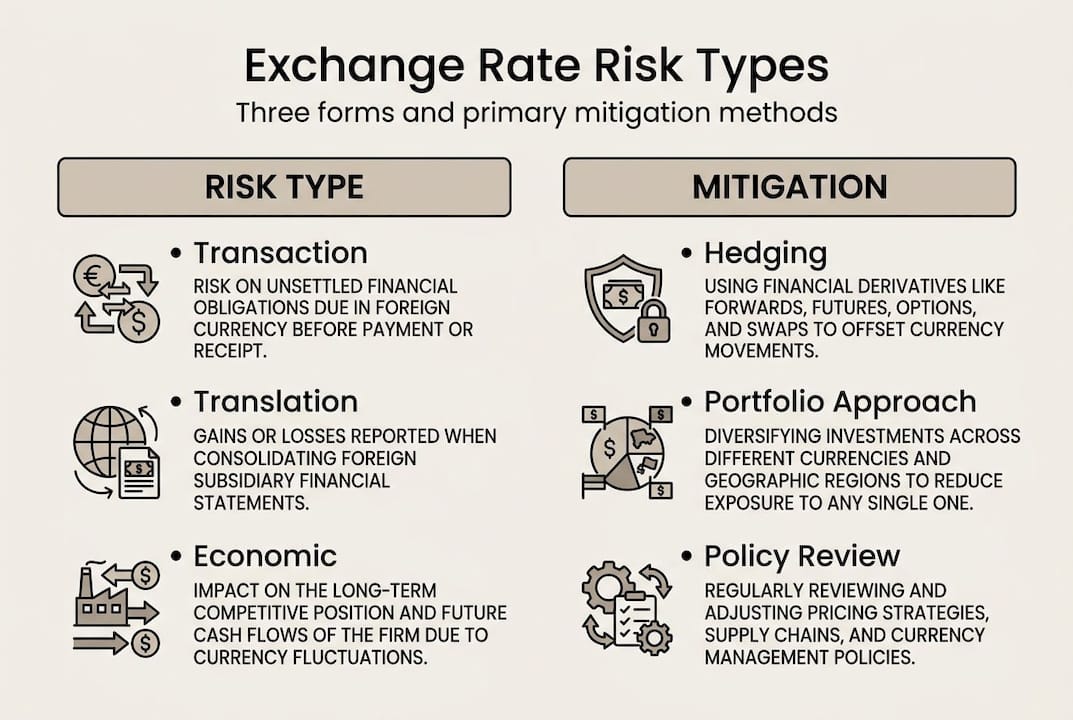

With a definition set, it's essential to break down the major forms exchange rate risk takes within organizations. Three primary types exist: transaction risk, translation risk, and economic risk. Each operates differently and demands a distinct management response.

Transaction risk arises when a company enters into a commercial agreement in a foreign currency and the exchange rate shifts before settlement. If you invoice a European client in euros today and collect payment in 90 days, any euro depreciation against your home currency reduces what you actually receive. This is a direct cash flow impact.

Translation risk (also called accounting risk) occurs when a parent company consolidates the financial statements of foreign subsidiaries. Assets, liabilities, revenues, and expenses reported in local currencies must be translated at current exchange rates, creating gains or losses on the balance sheet. Critically, these are often paper entries — they do not affect operating cash flows, but they do affect reported earnings per share and book value.

Economic risk (also called operating risk) is the most strategic of the three. It refers to the long-term impact of persistent currency shifts on a company's competitive position. If your production costs are in euros but your main competitor manufactures in Japanese yen, a sustained yen depreciation improves their price competitiveness even if you have no direct yen exposure.

Manufacturing enterprises show higher sensitivity to exchange rate risk than service-oriented ones, largely because their cost structures are geographically fixed while revenue can span many currency zones. Service companies often have more flexibility to adjust pricing or shift delivery locations.

| Risk type | Cash flow impact | Reporting impact | Time horizon | Most common hedge |

|---|---|---|---|---|

| Transaction | Direct | Yes | Short term | Forwards, options |

| Translation | Indirect | Yes | Periodic | Balance sheet hedges |

| Economic | Structural | Long term | Multi-year | Natural hedges, diversification |

For more on how these types and exposures map to specific instruments and business models, the distinctions between transaction and economic risk are especially relevant for companies evaluating long-term market entry decisions.

How exchange rate risk impacts business performance

These categories of risk play out not just on balance sheets, but in every facet of business results. The financial consequences of unmanaged exchange rate risk are well-documented and quantifiable.

Research across emerging and developed markets consistently shows that firms using structured FX hedging and forecasting report higher return on assets (ROA), greater financial stability, and reduced earnings volatility compared to unhedged peers. In emerging markets, where currency swings can be severe and sudden, the performance gap between hedged and unhedged firms widens considerably.

Here is how this plays out in practice:

| Metric | Unhedged company | Hedged company | Typical improvement |

|---|---|---|---|

| Earnings volatility | High | Low to moderate | 30 to 50% reduction |

| ROA consistency | Variable | Stable | Measurable YOY improvement |

| Balance sheet FX impact | Significant | Managed | Reduced translation variance |

| Forecasting accuracy | Poor | Improved | Better guidance reliability |

The impact is not limited to large multinationals. Mid-size companies with even 20% of revenues in foreign currencies can see quarterly earnings swing materially based purely on rate movements, making FX volatility a board-level issue, not just a treasury function.

Pro Tip: Build a currency sensitivity model that shows your earnings before interest and taxes (EBIT) impact for every 1% move in your top three currency pairs. This single tool turns abstract FX risk into a number your CFO and board can act on, and it forms the basis for a defensible hedging policy.

For a closer look at the relationship between currency volatility and profits, the data consistently points to proactive risk management as a structural competitive advantage rather than a cost center.

Proven strategies to mitigate exchange rate risk

Knowing the business stakes, let's turn to how leading companies protect profitability from currency volatility. Effective mitigation is not a single action — it is a layered program that combines measurement, instruments, policy, and governance.

Here is a practical sequence:

- Map your exposures. Identify every currency pair in which you have material receivables, payables, assets, or forecast revenues. Segment them by type: transaction, translation, or economic.

- Quantify risk. Use Value at Risk (VaR) or scenario analysis to estimate potential losses under adverse but plausible rate moves. This creates a fact base for decisions.

- Select hedging instruments. Hedging methodologies include forward contracts, options, futures, currency swaps, and natural hedging. Each carries different cost and flexibility profiles.

- Set a hedging policy. Define coverage ratios, tenor limits, and instrument preferences. Document the policy so execution is consistent regardless of who runs treasury.

- Monitor and adjust. Markets change. A hedge that was appropriate six months ago may be over- or under-sized today. Regular review keeps your program calibrated.

On instrument selection, multi-instrument portfolios with dynamic measurement outperform single-instrument approaches. Over-reliance on forwards, while common, leaves companies exposed to nonlinear risks that options can address more effectively.

Regarding policy design, three broad approaches exist: full hedging (low risk, lower upside), selective hedging (moderate risk and reward), and casual hedging (high risk, high variability). A 50% hedge ratio is often described as the "least regret" position — it captures some benefit from favorable moves while limiting downside — but it must be grounded in a documented policy rationale, not intuition.

Pro Tip: Review your hedging strategies overview at least quarterly and after significant market events. A static hedge book built for last year's volatility environment is not suitable for today's markets. Pair this with risk analytics in FX to make policy adjustments data-driven rather than reactive.

A hard-earned perspective on exchange rate risk management

Here is an uncomfortable truth that practical experience confirms repeatedly: most exchange rate risk programs fail not because of bad instruments, but because of bad governance. Companies implement a forward contract program, check the "hedging" box, and move on. Then a sustained currency trend exposes the gaps — nonlinear exposures that forwards cannot address, translation risks that were never mapped, economic risks that only surface when a competitor's cost structure shifts permanently.

The over-reliance on forwards while ignoring nonlinear risks is one of the most frequently cited weaknesses in corporate FX programs. This is not a technical failure — it is a governance failure. Senior leadership needs to understand what the hedging program can and cannot do, and treasury teams need the authority and tools to adapt.

The companies that manage exchange rate risk most effectively treat it as a portfolio problem, not a transaction problem. They build layered policies, use scenario planning to stress-test assumptions, and embed FX risk awareness into strategic planning, pricing decisions, and capital allocation. For teams ready to build that kind of program, currency risk strategy for 2026 provides a current framework for where policy design is heading.

Unlock streamlined FX risk management for your organization

The frameworks covered here — exposure mapping, instrument selection, policy governance — require reliable data, real-time visibility, and analytics that scale with your portfolio.

CorpHedge is built specifically for corporate finance and risk management teams that need more than a spreadsheet. The platform delivers automated FX exposure tracking, Value at Risk analytics, and flexible FX Exposure Management features that support both strategic and tactical hedging decisions. Whether you are managing a single currency pair or a multi-regional portfolio, the Foreign Exchange Risk Management Solutions at CorpHedge give your team the tools to move from reactive to proactive. Explore the full capability set at CorpHedge and see how leading treasury teams are operationalizing exactly the strategies covered in this article.

Frequently asked questions

What is the simplest definition of exchange rate risk?

Exchange rate risk is the potential for loss or gain caused by changes in currency exchange rates that affect the value of cross-border transactions, investments, or financial holdings.

What are the three types of exchange rate risk?

The three primary types are transaction risk, which hits cash flows directly; translation risk, which affects accounting consolidation; and economic risk, which shapes long-term competitive positioning.

Why is exchange rate risk important for international companies?

Because it directly affects profits, reported earnings, and strategic competitiveness — firms using structured FX hedging consistently report stronger ROA and reduced earnings volatility compared to unhedged peers.

What is the difference between transaction and translation risk?

Transaction risk creates real cash flow differences when foreign currency payments settle at rates different from when they were agreed; translation risk is an accounting restatement that affects reported figures without changing actual cash.

What is the most effective way to hedge exchange rate risk?

A multi-instrument portfolio with dynamic measurement — combining forwards, options, and regular policy reviews — outperforms any single-instrument approach and is the standard recommended by research and leading practitioners.