TL;DR:

- Banking reconciliation services systematically match internal cash records against bank statements to ensure financial accuracy across global operations. Automation and clear controls enhance efficiency, while outsourcing can address capacity challenges and improve audit readiness, especially in multilingual, multi-currency environments. Emphasizing exception management as a control tool enables continuous process improvement and stronger financial governance.

Banking reconciliation services are defined as the systematic process of matching a company's internal cash ledger records against bank statements to identify and resolve every discrepancy before financial periods close. For international finance teams managing accounts across multiple currencies and jurisdictions, this process is not optional. It is the foundation of accurate financial reporting, fraud prevention, and audit readiness. Tools like Oracle Fusion and QuickBooks embed reconciliation modules directly into the accounting workflow, while outsourced providers such as Acelerar and Assivo offer dedicated account reconciliation solutions with defined service levels. Getting this process right determines whether your month-end close takes two days or two weeks.

What are banking reconciliation services and how do they work?

Banking reconciliation services cover the full cycle of comparing your internal cash records to bank statements, classifying every difference, and posting correcting entries until both balances agree. The industry standard term for this practice is bank reconciliation, and it sits at the core of any credible financial close process. AccountingTools describes the process as accessing bank statements, matching uncleared checks and deposits in transit, adjusting entries, and investigating variances until balances align. That description sounds simple. In a multinational with dozens of bank accounts across Poland, Sweden, and Southeast Asia, the complexity multiplies fast.

The goal is always the same: the adjusted bank balance must equal the adjusted book balance, with zero difference. Xenett's reconciliation guide classifies differences into two categories: timing differences (checks that have not cleared, deposits in transit) and errors (data entry mistakes, duplicate postings, or bank errors). Timing differences resolve themselves in the next period. Errors require immediate correction. Knowing which category you are dealing with is the first diagnostic skill every reconciliation analyst needs.

The benefits extend beyond accuracy. A completed reconciliation with full documentation supports external auditors, satisfies SOX testing requirements, and gives treasury teams a reliable cash position for FX hedging decisions. For companies managing FX risk across currencies, an unreconciled cash ledger introduces a second layer of uncertainty on top of exchange rate volatility.

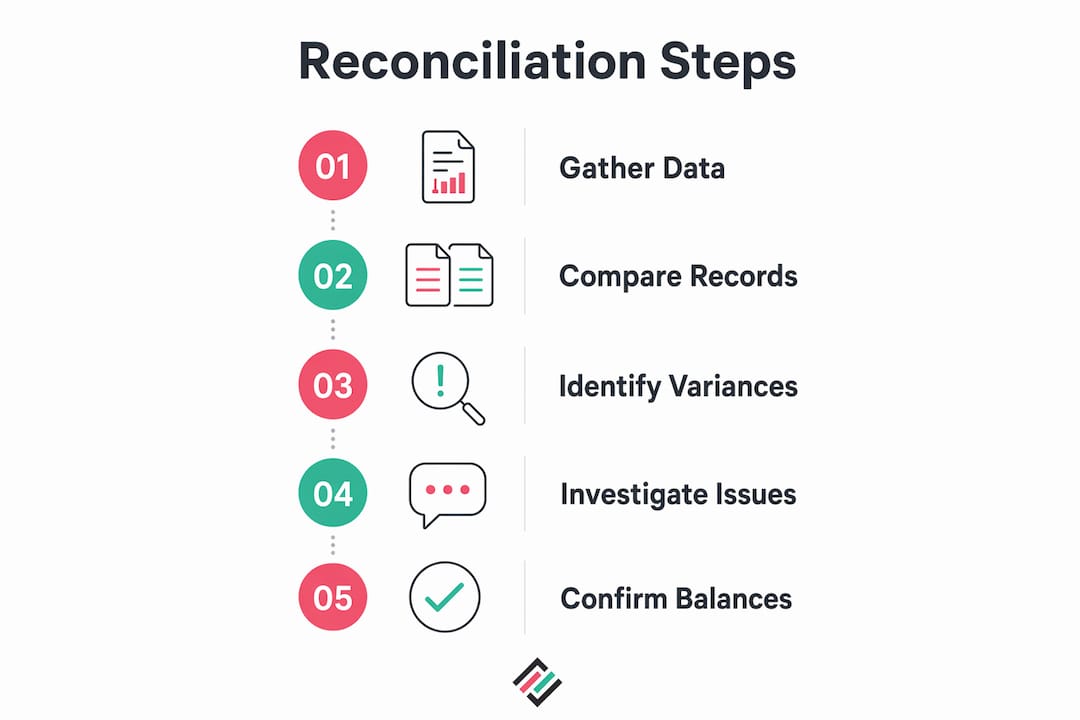

What is the bank reconciliation process step by step?

A disciplined bank reconciliation process follows a repeatable sequence. Skipping steps creates the kind of unresolved exceptions that accumulate into audit findings.

- Pull the bank statement and the cash general ledger. Access the bank statement for the period and export the corresponding cash account transactions from your accounting system. Both documents must cover the same date range exactly.

- Match cleared transactions. Compare each bank transaction to its corresponding ledger entry. Mark every item that appears on both sides as matched. Most automated reconciliation software handles this step using rule-based matching algorithms.

- Identify and classify reconciling items. Unmatched items fall into three buckets: timing differences (outstanding checks, deposits in transit), errors (wrong amounts, duplicates), and bank-only items (fees, interest income, NSF charges).

- Post bank-only items to the ledger. Bank fees, interest earned, and returned check charges appear on the bank statement but not in your books until you post them. These entries must be recorded before the reconciliation can close.

- Adjust both balances and confirm zero difference. Calculate the adjusted bank balance and the adjusted book balance. If they match, the reconciliation is complete. If they do not, investigate the remaining gap before proceeding.

- Save documentation and lock the accounting period. Attach the reconciliation workpaper, the bank statement, and any supporting evidence. Lock the period in your accounting system to prevent retroactive changes.

Pro Tip: Never lock a period with an unresolved variance, even an immaterial one. Document the variance, note your investigation steps, and get a supervisor sign-off before locking. Auditors treat unexplained variances as control deficiencies regardless of dollar amount.

What tools and technology enhance banking reconciliation for multinational companies?

Automated reconciliation software has changed the economics of the bank reconciliation process. What once required a full day of manual matching now takes minutes for the matched portion, leaving analysts to focus on genuine exceptions.

The core technology stack for a multinational finance team typically includes:

- Automated bank feed integration that pulls transaction data directly from banking portals in real time, eliminating manual statement downloads and the transcription errors that come with them.

- Intelligent matching algorithms that learn from historical transaction patterns. Oracle Fusion's auto-reconciliation module achieves over 96% automatic matching of statement lines, with remaining exceptions clustered by root cause for targeted resolution. That figure means a team reconciling 10,000 transactions per month manually reviews fewer than 400.

- Multi-currency and multi-account support that handles exchange rate conversions and consolidates positions across accounts in Poland, Sweden, the U.S., and any other jurisdiction without requiring separate reconciliation files.

- Audit trail generation that timestamps every match, exception, and correction with user metadata, satisfying both internal review requirements and external audit sampling.

The table below compares three common approaches to financial reconciliation services by capability:

| Capability | Manual spreadsheet | Accounting software module | Dedicated reconciliation platform |

|---|---|---|---|

| Matching speed | Hours per account | Minutes per account | Seconds per account |

| Multi-currency support | Limited | Moderate | Full |

| Audit trail | Manual documentation | Partial automation | Fully automated |

| Exception management | Ad hoc | Rule-based | AI-assisted clustering |

| SOX compliance support | High effort | Moderate | Built-in |

Pro Tip: When evaluating automated reconciliation software, ask vendors for their exception rate statistics from live client accounts, not demo environments. A platform claiming 95% auto-match on clean data may deliver 70% on your actual transaction mix.

When should international companies consider outsourcing banking reconciliation services?

Outsourcing reconciliation makes operational sense when internal headcount cannot keep pace with transaction volume, when month-end close timelines are consistently missed, or when audit findings point to control gaps in the reconciliation function. Outsourced providers like Acelerar and Assivo offer turnaround times of approximately 48 hours for monthly reconciliations, with accuracy rates cited at 99.7% and daily reconciliation options for high-volume accounts. Those service levels are difficult to replicate with a two-person accounting team during a busy close cycle.

The operational benefits of outsourcing include:

- Segregation of duties between the team recording transactions and the team performing reconciliation, a control requirement under SOX that many lean finance functions struggle to maintain internally.

- Audit-ready documentation delivered as part of the service, including variance investigation notes and exception aging reports.

- Scalability across new markets. When Corphedge clients expand into Poland or Sweden, adding bank accounts to an outsourced reconciliation program is faster than hiring and training local staff.

- Defined performance metrics including accuracy rates, exception aging, and transaction-level tie-out reports that give finance leadership visibility into service quality.

The risk in outsourcing is ambiguous ownership. Etisson's analysis of international reconciliation makes clear that unclear responsibilities and deadlines cause stalled work and rework, particularly during month-end close and audit preparation. Before signing a contract, define exactly which accounts are in scope, who owns exception resolution, and what the escalation path is when a variance cannot be resolved within the service window.

Assivo's reconciliation framework adds that measurable KPIs and audit support, including transaction-level tie-outs and exception aging reports, are the differentiators that separate a capable provider from one that simply delivers a spreadsheet. Demand both before committing.

What are best practices and internal controls for audit-ready reconciliation?

Internal controls in the bank statement reconciliation process are not bureaucratic overhead. They are the mechanism by which finance leaders demonstrate to auditors, regulators, and boards that cash balances are reliable. The KPMG ICFR handbook, grounded in the COSO framework, places management's responsibility to maintain documented control operation evidence at the center of internal financial reporting compliance.

The four non-negotiable controls in any reconciliation program are:

- Segregation of duties. The person who records transactions must not be the same person who reconciles the account or approves the reconciliation. This single control eliminates the most common fraud vector in cash management.

- Timeliness. Reconciliations completed weeks after period close lose their control value. SOX-controlled environments treat late reconciliations as deficiencies. Set and enforce completion deadlines tied to the close calendar.

- Independent review. A supervisor or controller must review and approve each reconciliation before the period locks. Review is not a formality. It is the second line of defense against errors that the preparer missed.

- Audit-safe corrections. When an error is found after a period has closed, corrections must be logged as new reversing entries with requester, approver, and timestamp metadata. Deleting or modifying original records destroys the audit trail and creates SOX exposure.

"Management must ensure continuous documented evidence of control effectiveness over reconciliations to comply with COSO and SOX internal control requirements." — KPMG ICFR Handbook

Finance teams building or refreshing their risk reporting and internal control documentation should treat the reconciliation control set as a priority area, particularly when expanding into new regulatory environments like Poland or Sweden.

What common challenges occur in banking reconciliation and how do you fix them?

Even well-designed reconciliation programs produce exceptions. The difference between a high-performing team and a struggling one is how fast exceptions are resolved and whether the root causes are addressed permanently.

The most frequent problems in monthly reconciliation services are:

- Uncleared checks that remain outstanding for more than 90 days. These are often voided checks that were never removed from the outstanding list, or payments to vendors who never cashed them.

- Deposits in transit that appear in the ledger but not yet on the bank statement. These resolve in the next period if legitimate. If they persist, investigate whether the deposit was actually made.

- Mismatched amounts caused by data entry errors, rounding differences in currency conversion, or bank fees applied at the transaction level.

- Missing entries where a bank transaction has no corresponding ledger record, typically bank fees, interest, or direct debits set up outside the normal purchase order process.

The principle that separates efficient teams from manual-chasing ones is exception-driven workflow design. Rexi Finance's analysis describes effective reconciliation as a four-step exception cycle: detection, routing, investigation, and resolution, all supported by audit trails. Teams that work this way spend their time on genuine problems rather than re-examining already-matched transactions.

Oracle Fusion's exception clustering approach demonstrates the value of treating exceptions as tuning signals. When a batch of exceptions shares a single root cause, such as an amount tolerance threshold set too tightly, adjusting the matching rule eliminates the entire cluster rather than requiring individual manual resolution.

Pro Tip: Build a monthly exception log that tracks each unresolved item by age, owner, and root cause category. After three months, patterns become visible. Most recurring exceptions trace back to two or three fixable process gaps.

Key takeaways

Effective banking reconciliation services require a disciplined combination of process controls, automation, and clear ownership to deliver audit-ready financial accuracy across international operations.

| Point | Details |

|---|---|

| Zero-difference standard | Reconciliation is complete only when adjusted bank and book balances match exactly, with every variance documented. |

| Automation raises the floor | Platforms like Oracle Fusion achieve over 96% auto-matching, reserving analyst time for genuine exceptions. |

| Outsourcing requires defined scope | Clear ownership, deadlines, and KPIs prevent rework and protect month-end close timelines. |

| Controls must be documented | SOX and COSO require continuous evidence of control operation, not just a completed reconciliation workpaper. |

| Exceptions are tuning signals | Recurring mismatches indicate matching rule gaps. Fix the rule, not just the individual exception. |

Why exception-driven reconciliation changed how I think about financial controls

Most finance teams I have worked with treat reconciliation as a confirmation exercise. They expect it to come out clean, and when it does not, they treat exceptions as problems to eliminate as fast as possible. That framing is backwards.

Exceptions are the most valuable output of the entire reconciliation process. They tell you where your controls have gaps, where your matching rules are miscalibrated, and occasionally where someone is manipulating transactions. A reconciliation that produces zero exceptions every month without any tuning effort is not a sign of a healthy process. It is a sign that your matching rules are too loose and real discrepancies are being auto-matched away.

The teams I have seen operate at the highest level treat their exception log as a management tool. They track exception aging, categorize root causes, and review the log in monthly close meetings alongside the P&L. When an exception type disappears after a rule change, that is a measurable process improvement. When a new exception type appears, it triggers an investigation before it becomes an audit finding.

For international companies expanding into markets like Poland or Sweden, this discipline matters even more. New banking relationships, new payment rails, and new regulatory requirements all introduce exception patterns that your existing matching rules were not built to handle. Starting with an exception-driven mindset means you adapt faster and close cleaner from day one.

The outsourcing question follows the same logic. The providers worth working with are the ones who send you an exception aging report alongside the reconciliation workpaper. If a provider only tells you the reconciliation is done, ask what happened to the exceptions. The answer reveals everything about their actual process quality.

— Bartas

How Corphedge supports your reconciliation and FX risk workflow

For international finance teams, banking reconciliation does not exist in isolation. Every reconciled cash position feeds directly into FX exposure calculations, hedging decisions, and treasury reporting. Corphedge integrates FX risk management with the financial visibility your reconciliation process produces, giving you real-time currency position data alongside your reconciled cash balances.

Corphedge's platform supports Value at Risk-based hedging that connects directly to your reconciled cash and receivables positions, so your hedge ratios reflect actual exposure rather than estimated balances. For companies operating in Poland, Sweden, and other multi-currency markets, this connection between reconciliation accuracy and FX risk management is where financial precision translates into measurable cost savings. Explore the full platform features to see how Corphedge fits your reconciliation and risk workflow.

FAQ

What is the purpose of banking reconciliation services?

Banking reconciliation services match a company's internal cash records to bank statements, identifying discrepancies caused by timing differences, errors, or fraud before financial periods close. The process supports accurate financial reporting, audit readiness, and reliable cash position data for treasury decisions.

How often should bank reconciliation be performed?

High-volume accounts benefit from daily reconciliation, while most companies perform monthly reconciliation tied to the financial close calendar. SOX-controlled environments treat late or incomplete reconciliations as internal control deficiencies.

What is the difference between a timing difference and an error in reconciliation?

A timing difference is a transaction that exists on one side of the reconciliation but has not yet appeared on the other, such as an outstanding check or a deposit in transit. An error is an incorrect amount, duplicate entry, or missing transaction that requires a correcting journal entry.

When does outsourcing bank reconciliation make sense?

Outsourcing account reconciliation solutions makes sense when internal teams cannot maintain segregation of duties, when close timelines are consistently missed, or when transaction volumes exceed internal capacity. Providers should deliver defined turnaround times, accuracy metrics, and exception aging reports as part of the service.

How do automated reconciliation tools reduce manual workload?

Automated reconciliation software uses rule-based and AI-assisted matching algorithms to process the majority of transactions without human review. Oracle Fusion's auto-reconciliation achieves over 96% automatic matching, leaving analysts to focus only on genuine exceptions rather than line-by-line manual comparison.