TL;DR:

- Operational risk in currency management stems from failures in internal processes, systems, or personnel, not market movements. Proper controls, data integration, and standardizing IFRS 9 documentation are essential to mitigating these risks in multinational programs. Treating FX management as a process discipline, rather than solely a financial strategy, significantly reduces operational failures and audit issues.

Operational risk in currency management is defined as the potential for financial loss resulting from failures in internal processes, systems, or personnel involved in managing currency exposures and hedging activities, not from market movements themselves. The Basel Committee on Banking Supervision and IFRS 9 both recognize this category as distinct from market risk, yet multinational finance teams routinely conflate the two. Execution errors, fragmented data, and reconciliation breakdowns are the real culprits behind most FX losses. Understanding this distinction is the first step toward building controls that actually work. This guide is written for finance professionals and risk specialists in international companies operating across multiple currencies, ERPs, and legal entities.

What are the key operational risk sources in currency management?

Operational risk in currency management originates from the infrastructure and processes that surround FX activity, not from the rates themselves. Fragmented data across ERPs, banking portals, and treasury systems forces teams into manual consolidation, which introduces errors at every step. A multinational operating SAP in Germany, Oracle in Poland, and a regional banking portal in Sweden will rarely have a single, consistent view of its net currency exposure without deliberate integration work.

The most common operational failure points in FX management include:

- Incomplete exposure identification. Subsidiaries report exposures on different schedules, using different rate sources, which makes consolidated hedging decisions unreliable.

- Manual data keying between systems. Manual inputs at system interfaces between ERP, treasury management systems, and accounting ledgers create hedge misalignment and month-end reconciliation exceptions.

- Spreadsheet-based hedge tracking. Spreadsheets have no audit trail by default, no version control, and no automated reconciliation. They are the single most common source of operational control failures in corporate FX programs.

- Late or inconsistent data feeds. When exposure data arrives after hedge decisions are made, the hedge either over-covers or under-covers the underlying position, generating P&L volatility that has nothing to do with market rates.

- Unclear ownership. When no single person or team owns exposure identification end-to-end, gaps appear between what is hedged and what is actually exposed.

Pro Tip: Map every data handoff in your FX workflow, from ERP to treasury to accounting, and assign a named owner to each interface. Interfaces without owners are where operational risk concentrates.

The interface between systems deserves special attention. System interfaces are the highest-risk points in any currency management workflow because they combine data transformation, timing differences, and manual intervention. A single miskeyed trade reference at the ERP-to-treasury interface can cascade into a hedge ineffectiveness finding at quarter-end. For companies expanding into new markets, such as Poland or Sweden, adding another ERP instance or banking relationship multiplies these interface risks proportionally.

How does IFRS 9 hedge accounting influence operational risk?

IFRS 9 is not just an accounting standard. It is an operational framework that imposes specific process requirements on every hedge a company designates. IFRS 9 requires formal hedge designation and contemporaneous documentation at inception, meaning the documentation must exist before or at the time the hedge is entered, not reconstructed afterward. This single requirement has significant operational implications for how treasury and accounting teams coordinate.

The operational requirements IFRS 9 places on finance teams break down into four sequential steps:

- Hedge designation. At inception, the team must formally document the hedging relationship, the risk management objective, the hedged item, the hedging instrument, and the expected sources of ineffectiveness. This is not a one-time exercise. Each new hedge requires its own designation package.

- Effectiveness assessment design. Documentation must specify hedge effectiveness methods and expected ineffectiveness sources upfront. Teams must decide whether to use a qualitative assessment, a dollar-offset method, or a regression analysis, and that choice must be applied consistently.

- Ongoing effectiveness testing. Effectiveness assessment under IFRS 9 is continuous, not periodic. Inconsistent application of effectiveness methods raises operational risk because auditors will test whether the methodology applied at each reporting date matches the designated approach.

- Workflow integration. Separating hedge accounting from FX execution workflows leads to inconsistent rate sources, mismatched exposure data, and weak governance. The accounting team and the treasury team must work from the same data set in real time.

Pro Tip: Build your IFRS 9 designation templates directly into your hedge approval workflow. If a hedge cannot be approved without a completed designation package, you eliminate the most common audit finding before it occurs.

The practical lesson here is that IFRS 9 compliance is an operational discipline, not an accounting afterthought. Companies that treat hedge documentation as a back-office task consistently face audit findings, restatements, and increased scrutiny from external auditors. For firms with entities in multiple jurisdictions, including newer markets like Poland and Sweden, maintaining consistent documentation standards across legal entities adds another layer of operational complexity.

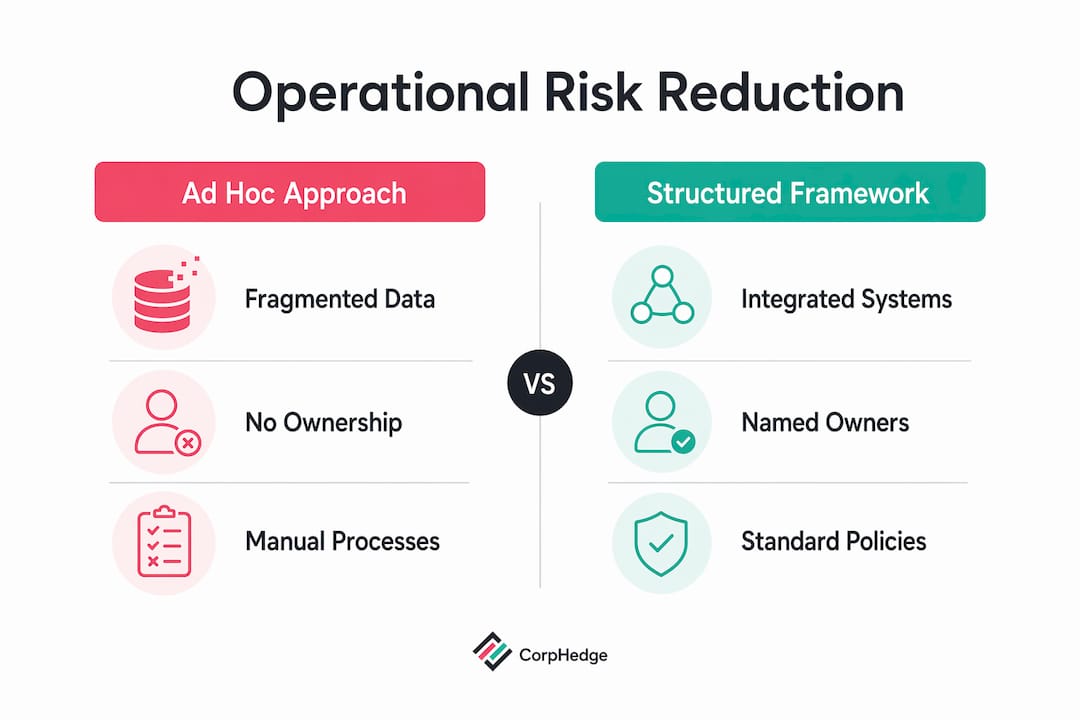

What frameworks reduce operational risk in currency management?

Effective currency risk management requires a standardized FX lifecycle framework that covers every stage from exposure identification to hedge settlement. The table below compares an ad hoc approach against a structured operational framework across the dimensions that matter most.

| Dimension | Ad hoc approach | Structured framework |

|---|---|---|

| Exposure identification | Subsidiary-driven, inconsistent timing | Centralized, scheduled, standardized templates |

| Rate sources | Multiple, unreconciled | Single approved source per currency pair |

| Hedge designation | Informal, often retroactive | Formal, contemporaneous, templated |

| Effectiveness testing | Periodic, method varies | Continuous, fixed methodology, documented |

| System integration | Manual consolidation via spreadsheet | Automated feeds between ERP, TMS, and accounting |

| Audit readiness | Reconstructed on request | Embedded, real-time audit trail |

A standardized FX lifecycle with explicit ownership at each stage is the single most effective operational risk control available to multinational finance teams. The comparison above makes the gap visible. Ad hoc programs generate operational risk at every stage. Structured programs convert those risk points into controls.

The practical elements of a working framework include:

- A written FX risk policy that defines hedging objectives, approved instruments, hedge ratios, and review frequency.

- Named ownership for each stage of the FX lifecycle, from the subsidiary finance manager who identifies exposures to the treasury analyst who executes hedges to the controller who performs effectiveness testing.

- Integrated data architecture that connects ERP systems, treasury management platforms, and accounting ledgers without manual rekeying.

- A single approved rate source per currency pair, applied consistently across all entities and reporting periods.

- Regular operational performance reviews that track metrics like hedge coverage ratios, reconciliation exceptions, and documentation completion rates.

For companies managing currency risk across global operations, the governance layer is as important as the technology. Automation reduces errors, but clear accountability prevents the process gaps that automation cannot catch.

What operational pitfalls cause FX risk management failures?

Many FX problems attributed to adverse rates are actually operational execution failures related to fragmented data and manual processes. This is the most underappreciated insight in corporate FX management. Before blaming the market, finance teams should audit their own workflows.

The most damaging operational pitfalls in practice are:

- Fragmented exposure views. When exposure data lives in multiple systems without automated consolidation, hedges are sized against incomplete information. The result is systematic over-hedging or under-hedging that creates P&L volatility regardless of market conditions.

- Late data causing misaligned decisions. Exposure reports that arrive two days after the hedge decision window create a structural mismatch between what was hedged and what is actually exposed. This is a process failure, not a forecasting failure.

- Changing effectiveness methods without controls. Switching from a qualitative to a quantitative effectiveness assessment mid-year without updating the designation documentation is a governance failure that auditors will flag. Consistency in effectiveness methods is a hard IFRS 9 requirement, not a best practice.

- No embedded audit trail. When hedge approvals, rate confirmations, and effectiveness test results exist only in email threads or spreadsheets, reconstructing an audit trail at year-end is expensive and unreliable.

The most common audit finding in corporate hedge accounting programs is not that hedges were ineffective. It is that the documentation to prove effectiveness was incomplete or inconsistent. Fix the process, and the audit finding disappears.

For teams working to build governance into FX workflows, the practical fix is to treat every hedge as a transaction that requires a complete, timestamped record from designation through settlement. Partner-level remittance operations face similar operational execution risks when fragmented infrastructure causes delays and mismatches in cross-border payment workflows.

Key takeaways

Operational risk in currency management is controlled through process standardization, integrated data systems, and consistent IFRS 9 documentation, not through better market timing.

| Point | Details |

|---|---|

| Operational vs. market risk | FX losses from process failures are distinct from market risk and require different controls. |

| System interfaces are highest risk | Manual data handoffs between ERP, treasury, and accounting create the most reconciliation failures. |

| IFRS 9 is an operational discipline | Hedge designation and effectiveness testing must be embedded in workflows, not handled retroactively. |

| Standardized lifecycle reduces errors | Explicit ownership and fixed procedures at each FX lifecycle stage are the most effective controls. |

| Audit trail must be real-time | Reconstructed documentation consistently fails audits. Embed timestamped records from inception. |

Why operational risk is still the most underestimated problem in FX management

After working with multinational finance teams across industries, the pattern I see most consistently is this: companies invest heavily in hedging strategy and almost nothing in the operational infrastructure that makes that strategy executable. They hire experienced treasury professionals, select sophisticated instruments, and then run the entire program through a combination of spreadsheets and email approvals. The strategy is sound. The execution is fragile.

The integration of hedge accounting and operational workflows is the area I find most underestimated. Finance teams treat IFRS 9 documentation as an accounting task that happens after the hedge is executed. That sequencing is exactly backwards. When documentation is an afterthought, it is inconsistent. When it is inconsistent, auditors find control weaknesses. When auditors find control weaknesses, the entire hedging program comes under scrutiny, regardless of how well the hedges actually performed.

Technology helps, but it does not solve a governance problem on its own. I have seen companies implement treasury management systems and still produce reconciliation exceptions every month because the data governance around those systems was never defined. The tool is only as good as the process it automates. For companies expanding into new markets like Poland or Sweden, the temptation is to replicate existing workflows in the new entity. The smarter move is to use the expansion as a forcing function to standardize and document the workflow properly before it scales.

The firms that manage operational risk well share one characteristic: they treat FX management as a process discipline, not just a financial one. They define ownership, document procedures, integrate systems, and review performance metrics regularly. That discipline is what separates programs that hold up under audit from those that do not.

— Bartas

How Corphedge addresses operational risk in FX management

Finance teams that have identified operational gaps in their currency management programs need more than a policy document. They need infrastructure that makes the right process the default process.

Corphedge is built specifically for multinational corporates managing complex FX exposures across multiple entities and systems. The platform consolidates exposure data from ERPs and banking systems into a single real-time view, eliminating the manual consolidation that creates most operational errors. Automated IFRS 9 hedge accounting workflows handle designation documentation and effectiveness testing with embedded audit trails, so your program is audit-ready at every point in the hedge lifecycle. For teams ready to see how integrated FX risk management works in practice, the Corphedge demo tour walks through the full operational workflow.

FAQ

What is operational risk in currency management?

Operational risk in currency management is the risk of financial loss from failures in internal processes, systems, or personnel involved in managing FX exposures and hedges. It is distinct from market risk, which arises from exchange rate movements.

How does IFRS 9 increase operational risk for treasury teams?

IFRS 9 requires contemporaneous hedge designation documentation and consistent effectiveness testing methodology. Inconsistent application or retroactive documentation raises audit and governance risk, making hedge accounting an operational discipline as much as an accounting one.

What are the most common operational failures in FX management?

The most common failures are fragmented exposure data across multiple systems, manual data entry at system interfaces, spreadsheet-based hedge tracking without audit trails, and late exposure reporting that misaligns hedges with underlying positions.

How can multinational companies reduce operational risk in FX programs?

Standardizing the FX lifecycle with named ownership at each stage, integrating ERP and treasury systems to eliminate manual rekeying, and embedding IFRS 9 documentation into hedge approval workflows are the three highest-impact controls available.

Why do many FX losses get blamed on rates when they are actually operational failures?

When exposure data is fragmented or late, hedges are sized incorrectly, producing P&L volatility that looks like a market outcome but is actually a process failure. Auditing the operational workflow before attributing losses to market conditions is the correct diagnostic sequence.