TL;DR:

- Foreign exchange fluctuations gradually erode international business margins, often going unaddressed until losses appear. Implementing a structured FX policy, operational natural hedges, layered financial instruments, and active governance helps prevent costly currency losses. Companies that discipline exposure management and leverage automation like Corphedge significantly reduce earnings volatility and hedge costs.

Foreign exchange fluctuations quietly erode margins for international businesses every quarter, yet most companies only formalize their response after a significant loss has already appeared on the income statement. If your business invoices in multiple currencies, sources materials abroad, or operates subsidiaries across borders, the question is not whether currency movements will affect you. It's how much damage you'll allow before you act. This guide covers how to avoid forex losses for business through a structured sequence: building a formal policy, applying operational controls, deploying financial instruments, and sustaining active governance.

Table of Contents

- Key takeaways

- How to avoid forex losses for business with a formal FX policy

- Operational strategies to reduce gross exposure

- Financial instruments and layered hedging techniques

- Active governance and monitoring to prevent drift

- What I've learned from watching companies get this wrong

- How Corphedge helps you execute this in practice

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Start with a formal FX policy | Document ownership, hedge ratios, and approval thresholds before trading any financial instruments. |

| Use operational hedges first | Align revenues and costs in the same currency to reduce gross exposure before spending on financial hedges. |

| Layer and roll financial hedges | Stagger forward contracts and options over 12 to 36 months to reduce timing risk and earnings volatility. |

| Net exposures across entities | Consolidate subsidiary exposures before hedging to avoid paying twice to cover offsetting positions. |

| Govern actively, not reactively | Assign clear ownership, track exposures regularly, and never adjust hedge ratios based on directional market views. |

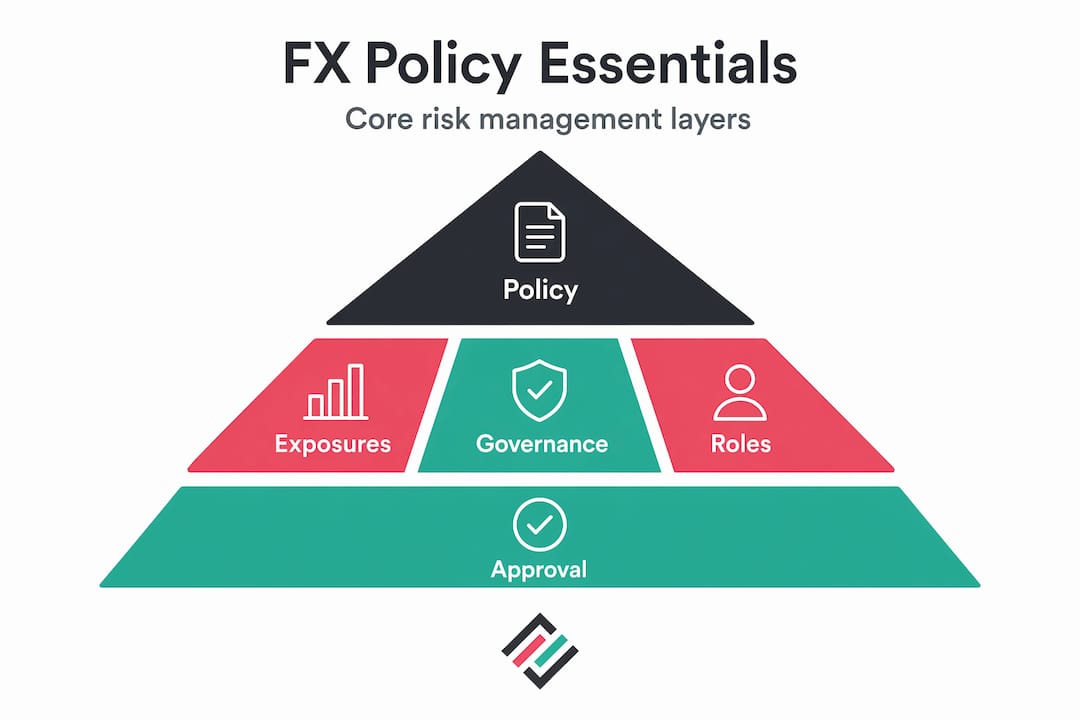

How to avoid forex losses for business with a formal FX policy

Most treasury teams underestimate how much unstructured decision-making costs them in FX. Before your company executes a single hedge, you need a written policy that defines who can authorize what, under what conditions, and with what limits. This is not an administrative exercise. It is the difference between a defensible risk management program and speculative trading dressed up as hedging.

A well-structured FX policy should document three things above all else. First, it must classify the types of FX exposure your business carries. Transaction exposure covers cash flows from known payables and receivables in foreign currencies. Translation exposure relates to consolidating overseas subsidiary financials. Economic exposure is the longer-term effect currency moves have on your competitive position, pricing power, and future revenues. Each type requires a different management approach, and conflating them leads to mispriced protection.

Second, a governance-first FX policy defines ownership and execution roles precisely, setting approval thresholds and avoiding hedge ratio adjustments driven by market views. This point matters more than most finance teams acknowledge. If your treasury desk is allowed to increase or decrease hedge ratios based on where they think the euro is heading, that is no longer hedging. As Cambridge Currencies' 2026 framework explicitly states, adjusting ratios on directional views becomes trading, not policy, and it fundamentally undermines your risk governance.

Third, your policy needs a scheduled review, ideally annual with board involvement, to align hedge guidelines with current business realities. Currency exposures shift as your revenue mix, supplier base, and geographic footprint change.

Pro Tip: Include a specific clause in your FX policy that prohibits entering derivative positions beyond documented underlying exposures. This single safeguard prevents well-intentioned treasury teams from drifting into speculation without realizing it.

- Categorize exposures by type (transaction, translation, economic) before setting hedge targets

- Set minimum and maximum hedge ratios for each exposure category, not a single blanket ratio

- Define who can approve trades above certain notional thresholds

- Schedule annual policy reviews with CFO and board sign-off

- Prohibit adjustments to ratios based on market sentiment or rate forecasts

Operational strategies to reduce gross exposure

The most cost-effective way to minimize currency exchange losses is to reduce the amount of exposure that needs hedging in the first place. This is what practitioners call natural hedging, and it is often underused because it requires cross-functional coordination rather than a treasury transaction.

The core principle is straightforward. When revenues in a given currency are matched by costs in the same currency, the net exposure is smaller, and the hedging cost drops accordingly. A European manufacturer selling in U.S. dollars can reduce its USD exposure significantly by sourcing raw materials or components from U.S.-based suppliers, paying in dollars. The cash flows offset each other naturally without any financial instrument involved. Combining natural hedges with forward contracts reduces conversion needs and locks in rates for future residual flows.

Operational planning, including payment timing and supply chain alignment, often drives the greatest reduction in FX loss risk before any financial hedge is placed. This insight from SLB's energy sector analysis applies equally to manufacturing, technology, and professional services.

Here is a practical sequence for building operational FX discipline:

- Map all currency inflows and outflows at the entity level, including anticipated cash flows from contracts not yet settled.

- Identify natural offsets where revenues and costs already share a currency, and document the residual net exposure that actually requires hedging.

- Net exposures across subsidiaries before hedging gross positions. Netting across entities before buying hedges leads to more efficient coverage than hedging each subsidiary's gross position independently.

- Use lead and lag strategies to adjust the timing of payments and receipts. When your functional currency is strengthening, accelerating payments in foreign currency locks in a better rate. When it is weakening, delaying receivables collection in a strong foreign currency captures more value.

- Open multi-currency accounts in your primary trading currencies to hold foreign currency balances and deploy them without immediate conversion.

Pro Tip: Before approaching your bank or FX platform for hedges, run a full netting analysis across all entities. You may find that 30 to 40 percent of what you thought needed hedging is already internally offset, which directly reduces your total cost of hedging.

The limitation of natural hedges is that they cannot be applied perfectly. Residual net exposure will always remain. That is exactly what financial instruments are designed to address.

Financial instruments and layered hedging techniques

Once you have reduced your gross exposure through operational controls, the remaining net exposure needs structured financial hedging. Three instruments dominate corporate FX programs: forward contracts, FX options, and cross-currency swaps.

| Instrument | Best use case | Key trade-off |

|---|---|---|

| Forward contract | Known, fixed future cash flows | Locks rate but eliminates upside if rates move favorably |

| FX option | Uncertain or variable exposures | Protects downside while preserving upside, but costs a premium |

| Cross-currency swap | Long-term debt or financing in foreign currency | Efficient for large, long-duration exposures |

Forward contracts are the most widely used tool for businesses that want to trade forex without losing money on rate timing. You agree on a rate today for settlement at a future date, removing price uncertainty for that specific cash flow. The limitation is that if the spot rate moves in your favor, you cannot benefit from it. Your rate is fixed.

FX options solve this problem by giving you the right, but not the obligation, to exchange at a pre-agreed rate. FX options should be matched to company risk tolerance and commercial realities rather than treated as a one-size solution. The upfront premium is a real cost, and as Fifth Third Bank notes, accounting for FX options can increase short-term reporting volatility because the premium is expensed upfront. You need internal stakeholder communication prepared for this before you execute.

The most mature corporate programs use layered, rolling hedges rather than one-off transactions. The optimal tenor for FX hedging programs is typically 12 to 36 months, with many companies adding tiers quarterly. Layered and rolling hedges reduce earnings volatility and timing risk compared to a single 100% hedge executed at one point in time. By spreading execution across multiple dates, you average into rates rather than gambling on a single transaction.

Hybrid approaches combining natural and financial hedges reduce both costs and volatility better than relying on either method alone. The data from Corphedge's research shows meaningful reductions in FX beta and hedging costs when both layers are applied together, which directly supports your profitability objectives.

Active governance and monitoring to prevent drift

Having a policy and placing initial hedges is only part of the answer. Companies that manage forex volatility risks effectively treat FX governance as an ongoing operational function, not a quarterly compliance check.

Clear ownership matters. Your CFO or Head of Treasury should hold accountability for policy compliance, with a designated person tracking the currency register weekly. Without assigned ownership, exposure tracking becomes inconsistent, and hedges placed six months ago may no longer align with actual underlying transactions.

Companies with formal FX policies experience 23% less earnings volatility than those operating without one. That gap widens further when the policy is actively monitored and enforced rather than filed and forgotten.

Governance best practices for protecting your FX investments include:

- Maintain a live currency exposure register updated at least monthly, more frequently in volatile periods

- Reconcile hedge positions against actual underlying cash flows every reporting cycle

- Flag any hedge ratio deviation beyond approved bands for immediate CFO review

- Use treasury management system (TMS) reporting to automate position tracking and generate exception alerts

- Conduct post-execution reviews on completed hedges to assess whether policy was followed and where timing could be improved

The most common drift pattern in corporate FX programs is the gradual introduction of market views into hedge ratio decisions. A treasury team sees a news report, decides the dollar will weaken, and quietly reduces the hedge ratio "just this quarter." Over time, this behavior compounds into a speculative posture that your original policy explicitly prohibited. Preventing this requires both structural controls and a culture that treats FX management as risk reduction, not return generation. For international businesses in markets like Poland and Sweden, where currency volatility can be material, this discipline is not optional. It is the foundation of sustainable FX risk management.

For a deeper look at structuring these FX governance controls, reviewing advanced frameworks for profit protection is worth your time.

What I've learned from watching companies get this wrong

I've seen companies lose more in FX than they ever spent on their entire risk management budget, not because they lacked intelligence, but because they lacked structure. The losses don't announce themselves. They accumulate quietly through a dozen small decisions made without a policy to reference.

The most uncomfortable truth I've found is that the operational side is where most of the value gets left on the table. Companies rush toward forward contracts and options as if the financial hedge is the whole answer. But if you haven't mapped your exposures, netted across entities, and aligned payment timing, you are paying to hedge gross positions that could have been reduced operationally for far less cost.

I've also seen well-intentioned treasury teams gradually transform a hedging program into a directional trading book without ever formally deciding to do so. It starts with one "defensive adjustment" based on a rate outlook. Then another. The governance safeguards are what prevent this, and they only work if someone with authority actually enforces them.

The businesses that manage FX well are not necessarily the ones with the most sophisticated instruments. They are the ones with the clearest policies, the most honest exposure measurement, and the discipline to follow their own rules when the market makes it tempting not to.

— Bartas

How Corphedge helps you execute this in practice

If you've worked through the policy, operational, and governance layers described above, the next challenge is execution at scale. Manual exposure tracking, spreadsheet-based hedge scheduling, and fragmented bank relationships introduce exactly the timing and oversight gaps that cost businesses money.

Corphedge was built specifically for international businesses that need to move beyond spreadsheets. The platform's hedging based on value at risk solution quantifies your actual exposure in real time and aligns hedge execution to your documented risk tolerance, not instinct. You can monitor live currency positions, enforce policy compliance automatically, and report on hedge effectiveness without rebuilding the analysis each period. For companies operating across currencies in markets including Poland and Sweden, Corphedge offers the FX exposure management tools to keep your program disciplined, documented, and cost-efficient. Explore the product tour or walk through a live demo to see how the platform maps to your specific FX risk structure.

FAQ

What is the most effective way to avoid forex losses for business?

The most effective approach combines a formal FX risk policy, operational natural hedges to reduce gross exposure, and layered financial instruments like forward contracts and options to cover residual risk. Companies with formal FX policies experience 23% less earnings volatility than those without.

What is a natural hedge and how does it reduce currency losses?

A natural hedge occurs when a company matches revenues and costs in the same currency, reducing the net amount that needs financial hedging. For example, a company earning U.S. dollars that also pays suppliers in dollars reduces its net USD exposure without buying any derivative instrument.

How long should a corporate FX hedging program run?

Most corporate programs operate on a rolling 12 to 36 month tenor, adding new hedge tiers quarterly. This approach spreads execution across multiple rate levels, reducing the risk of locking in a single unfavorable rate for your entire exposure.

How do you prevent treasury teams from speculating instead of hedging?

Write a specific policy prohibition against adjusting hedge ratios based on market forecasts or directional rate views, and assign a senior executive to enforce it. Any deviation from approved hedge ratio bands should trigger a mandatory review rather than a discretionary decision.

What tools help businesses manage forex risk more efficiently?

Treasury management systems and purpose-built FX risk platforms automate exposure tracking, hedge scheduling, and compliance reporting. Corphedge offers real-time position monitoring and value-at-risk based hedging to help manage forex volatility risks at scale without manual overhead.