TL;DR:

- Accounting and compliance services encompass financial recordkeeping, reporting, tax, and regulatory adherence functions essential for lawful business operations. They include bookkeeping, statutory accounts, tax compliance, auditing, and regulatory reporting, with added complexity for cross-border markets like Poland and Sweden. Proper management of these services mitigates risks such as financial misstatement, penalties, and reputational damage, especially as regulatory and technological requirements evolve.

Accounting and compliance services are defined as the integrated set of financial recordkeeping, reporting, tax, and regulatory adherence functions that businesses must maintain to operate lawfully and accurately. For any company operating in the UK, EU, or internationally, these services cover everything from statutory bookkeeping under UK GAAP or IFRS to tax planning and compliance obligations with HMRC, through to financial auditing services and internal control programs. Regulatory bodies including HMRC, the SEC, and the Financial Reporting Council set the standards that make these functions non-negotiable. Getting them right protects your business from penalties, reputational damage, and financial misstatement.

What core services do accounting and compliance include?

Accounting and compliance services span a wider range of functions than most business owners initially expect. The industry term "compliance accounting" captures the overlap between financial accuracy and regulatory adherence, but the practical scope goes well beyond filing a tax return on time.

The main components every business needs to understand:

- Bookkeeping and recordkeeping. UK companies must maintain adequate accounting records at all times, not just at year-end. This means tracking every transaction, invoice, and payroll entry in a format that supports statutory reporting.

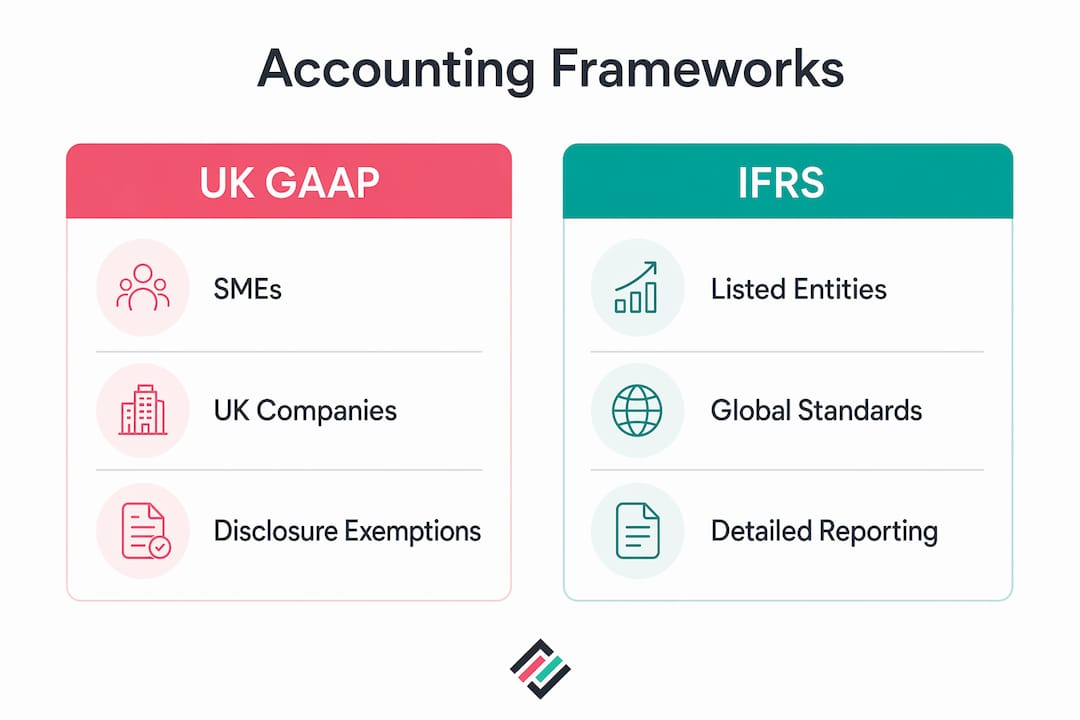

- Statutory accounting. Annual accounts must be prepared under UK GAAP or IFRS, depending on company size and structure. Statutory accounting frameworks also determine whether a company qualifies for disclosure exemptions, which can reduce reporting burden significantly.

- Tax planning and compliance. This covers corporation tax, VAT, payroll taxes, and cross-border tax obligations. Effective tax planning and compliance means structuring transactions to minimize liability within the law while meeting every filing deadline.

- Financial auditing services. Audit and assurance services provide independent verification that financial statements present a true and fair view. Audit triggers depend on company size, ownership structure, and sector-specific rules.

- Compliance accounting services. These include anti-money laundering (AML) controls, internal policy documentation, and regulatory reporting to bodies like Companies House and HMRC.

For businesses expanding into markets like Poland and Sweden, the compliance layer multiplies. Each jurisdiction adds its own statutory filing requirements, local GAAP considerations, and tax registration obligations on top of home-country rules.

How do businesses manage risks related to accounting and compliance?

Financial crime risk sits at the center of compliance accounting for any firm handling client money or providing tax services. HMRC's 2025 National Risk Assessment classifies accountancy service providers as high risk for money laundering, specifically because services like payroll processing, insolvency work, and trust administration can be misused by bad actors. This classification means accounting firms and their clients both carry elevated scrutiny.

Practical risk management in this space relies on four interconnected controls:

- Risk assessments. HMRC's AML guidance requires accounting firms to conduct thorough risk assessments covering client types, service types, and geographic exposure. A payroll client operating across multiple jurisdictions carries a different risk profile than a domestic sole trader.

- Internal controls over financial reporting (ICFR). The COSO framework, as detailed in KPMG's 2026 ICFR handbook, provides the most widely adopted structure for designing and testing these controls. Effective ICFR is not a one-time setup. It requires continuous monitoring and updating as business processes change.

- Cybersecurity controls. AI-driven automation in accounting systems introduces new attack surfaces. Internal control programs must now account for data integrity risks from automated journal entries and AI-assisted reconciliations.

- Policies, controls, and procedures (PCPs). Written PCPs that are actually followed, tested, and updated are the difference between a firm that passes regulatory review and one that faces sanctions.

Pro Tip: Map your compliance controls to specific risk scenarios rather than generic categories. A control labeled "review unusual transactions" is far less defensible than one that specifies the transaction type, the review frequency, and the named role responsible.

For businesses using accounting services for FX risk, currency exposure adds another compliance dimension. Foreign exchange gains and losses must be reported accurately, and the controls around FX positions need to integrate with your broader ICFR program.

What are the registration requirements for tax advisers in 2026?

HMRC's updated registration rules for tax advisers represent one of the most significant compliance changes for accounting service providers in 2026. Any individual or firm providing paid tax services or representing clients before HMRC must now register for an agent services account. The phased rollout follows a specific sequence:

- May 18, 2026. The first registration deadline applies to tax advisers providing the broadest range of services, including income tax, corporation tax, and VAT representation. Registration is mandatory from this date, replacing all former paper-based procedures.

- Later in 2026. Certain service categories have phased deadlines extending through the remainder of the year. Advisers providing only specific, limited services may qualify for a later registration window, but this exception is narrow and must be confirmed against HMRC's published guidance.

- Ongoing obligations. Once registered, advisers must maintain their account details, update client authorizations, and interact with HMRC exclusively through the agent services account for covered services.

- Consequences of non-registration. Failure to register results in the loss of ability to interact with HMRC on behalf of clients, plus potential financial sanctions. For firms whose revenue depends on HMRC representation, this is an existential compliance risk.

Businesses that outsource their tax compliance to external advisers need to verify their provider's registration status before May 18, 2026. An unregistered adviser cannot legally act on your behalf, which means your filings and correspondence with HMRC could be delayed or rejected.

How do statutory accounting requirements shape your compliance obligations?

Accounting compliance extends well beyond number preparation. The choice of accounting framework, the scope of required disclosures, and the audit threshold all interact to determine how much compliance work your business actually carries.

The table below compares the key statutory accounting considerations for UK companies:

| Factor | UK GAAP (FRS 102) | IFRS |

|---|---|---|

| Typical applicability | UK-incorporated companies, SMEs | Listed companies, multinationals |

| Disclosure exemptions | Available for qualifying small companies | More limited exemption options |

| Audit requirement | Size-based thresholds apply | Mandatory for listed entities |

| Financial reporting compliance | Companies House filing required | Additional SEC/FCA filing may apply |

| True and fair view standard | Required under Companies Act 2006 | Required under IAS 1 |

The audit threshold question deserves specific attention. Most UK companies qualify for audit exemption if they meet at least two of three criteria: turnover below £10.2 million, balance sheet total below £5.1 million, and fewer than 50 employees. However, group companies, regulated entities, and businesses with certain investor agreements often lose this exemption regardless of size. Financial auditing services become mandatory in those cases, not optional.

For businesses filing under IFRS, the SEC's expectations add another layer. SEC staff scrutinize MD&A disclosures closely, requiring quantified explanations for year-over-year changes and proper reconciliation of any non-GAAP metrics presented. A company can have technically compliant financial statements and still receive SEC comment letters if the narrative sections lack sufficient specificity.

How are AI and regulatory changes reshaping compliance services?

The compliance function is under pressure from two directions simultaneously: regulators are raising their expectations for disclosure quality, and technology is changing how financial data gets produced and controlled.

On the regulatory side, a proposed SEC rule would allow eligible companies to file semiannual reports using Form 10-S instead of quarterly reports. This shift would reduce reporting frequency but increase the depth and scrutiny applied to each filing. Companies that adopt semiannual reporting will need stronger internal controls to compensate for the longer gap between public disclosures.

On the technology side, internal controls must evolve continuously to manage risks from AI and automation in financial reporting. When an AI system generates journal entries or flags reconciliation exceptions, the control question shifts from "did a human review this?" to "is the AI model itself reliable, and how do we test that?" KPMG's ICFR guidance specifically calls out the need to map controls to end-to-end workflows, including all technological dependencies, rather than relying on clean finance policies alone.

SEC's focus on narrative disclosures and non-GAAP reconciliation reflects a broader shift toward investor-focused compliance. Regulators no longer accept technically accurate numbers paired with vague explanations. The certification language in annual reports now receives the same scrutiny as the financial statements themselves.

Pro Tip: If your business uses AI tools for any part of the financial close process, document the model's logic, its data inputs, and the human review steps explicitly in your ICFR documentation. Auditors and regulators will ask for this evidence, and retrofitting it after the fact is far more expensive than building it in from the start.

For businesses managing cross-border operations, currency risk governance intersects directly with financial reporting compliance. FX positions that are not properly hedged and disclosed create both accounting misstatement risk and regulatory exposure. The 2026 risk reporting checklist from Corphedge provides a structured starting point for finance executives integrating FX controls into their broader compliance programs.

Key takeaways

Effective accounting and compliance services require businesses to integrate statutory reporting, tax obligations, internal controls, and regulatory registration into a single, continuously updated compliance program.

| Point | Details |

|---|---|

| Registration deadline matters | Tax advisers must register with HMRC's agent services account by May 18, 2026, or lose client representation rights. |

| Framework choice drives obligations | Selecting UK GAAP versus IFRS determines disclosure requirements, audit triggers, and exemption eligibility. |

| AML risk is classified as high | HMRC designates accountancy service providers as high risk, requiring documented risk assessments and active controls. |

| AI changes control design | Automated financial processes require controls mapped to model logic and data inputs, not just human review steps. |

| Narrative quality is now scrutinized | SEC comment letters target MD&A language and non-GAAP reconciliations, not just the numbers in financial statements. |

Why compliance systems fail more often than compliance rules

The most common failure I see in accounting and compliance programs is not ignorance of the rules. It is treating compliance as a static checklist rather than a living system. A business will spend significant resources getting compliant in year one, then let the documentation drift while the actual processes change around it. By year three, the controls on paper bear little resemblance to what the team actually does.

The COSO framework and HMRC's AML guidance both assume that controls are tested and updated regularly. In practice, most small and mid-sized businesses test their controls once, at setup, and then revisit them only when something goes wrong. That gap is where regulatory risk accumulates.

The technology shift makes this worse. When a business adopts a new ERP module or an AI-assisted reconciliation tool, the control environment changes immediately. The compliance documentation rarely keeps pace. I have seen companies receive audit findings not because their controls were wrong, but because their documented controls described a process that no longer existed.

The businesses that manage this well treat their compliance program the way a good finance team treats a cash flow forecast: reviewed regularly, updated when assumptions change, and owned by a named individual with authority to act. That discipline is harder to build than any specific technical knowledge, but it is the actual differentiator between businesses that stay compliant and those that do not.

— Bartas

How Corphedge supports financial control and compliance management

Corphedge is built for businesses that need to manage financial risk with the same rigor they apply to their compliance obligations. For companies operating across currencies, the platform provides real-time visibility into FX positions, value-at-risk hedging strategies, and integration with platforms like Corpay to keep currency exposure within documented control limits. As businesses in Poland and Sweden face both local statutory requirements and cross-border FX exposure, Corphedge gives finance teams the tools to address both simultaneously. Explore the full platform features to see how FX risk management integrates with your accounting and compliance framework.

FAQ

What are compliance services in accounting?

Compliance services in accounting cover the processes businesses use to meet legal and regulatory financial obligations, including tax filing, statutory reporting, AML controls, and audit requirements. They extend beyond accurate bookkeeping to include risk assessment, framework selection, and ongoing regulatory registration.

When must tax advisers register with HMRC in 2026?

Tax advisers providing paid services or representing clients before HMRC must register for an agent services account starting May 18, 2026, with phased deadlines for some service categories extending through the rest of the year.

What is the difference between UK GAAP and IFRS for compliance purposes?

UK GAAP (FRS 102) applies primarily to UK-incorporated companies and SMEs, offering more disclosure exemptions for smaller entities. IFRS applies to listed companies and multinationals, with stricter disclosure requirements and fewer exemption options.

How does AI affect internal controls over financial reporting?

AI-driven automation in financial processes requires businesses to map controls to model logic, data inputs, and human review steps explicitly. KPMG's ICFR guidance identifies cybersecurity and AI as emerging risks that existing control frameworks must address directly.

What happens if an accounting firm fails to register with HMRC?

Unregistered firms lose the legal ability to interact with HMRC on behalf of clients and face potential financial sanctions. Businesses that rely on external advisers for tax compliance should verify their provider's registration status before the May 2026 deadline.