TL;DR:

- Natural hedging is an operational strategy that reduces currency exposure by aligning foreign currency inflows with outflows without using financial derivatives. It provides cost-effective, ongoing protection but rarely eliminates all residual risk, making it essential to monitor and complement with financial hedging. Combining natural and financial hedges offers the most effective approach for managing currency and environmental risks in global business.

Natural hedging is one of the most misunderstood concepts in corporate risk management. Many finance teams assume that once a natural hedge is in place, currency risk disappears. It does not. What is natural hedging, exactly? It is an operational strategy that structurally reduces currency exposure by aligning foreign currency inflows with outflows, rather than relying on financial derivatives. Recent research confirms that financial derivatives often have limited effectiveness in reducing overall risk, making natural hedging a foundational, if underappreciated, pillar of sound risk management.

Table of Contents

- Key takeaways

- What is natural hedging and how does it work

- Benefits and limitations of natural hedging strategies

- Natural hedging vs financial hedging: when to use each

- Emerging applications: natural capital as a hedging tool

- Implementing natural hedging strategies in practice

- My perspective on natural hedging's strategic value

- How Corphedge supports your hedging strategy

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Natural hedging is structural | It works by embedding currency offsets into business operations, not through financial instruments. |

| It reduces but does not eliminate risk | Natural hedging lowers exposure significantly but rarely covers the full residual risk. |

| Best used alongside financial hedging | Combining both approaches produces more effective protection than relying on either alone. |

| Evolving beyond currency risk | Institutions now use natural capital assets to hedge carbon price volatility and regulatory risk. |

| Implementation requires monitoring | Natural hedges must be reviewed as business conditions, supply chains, and regulations shift. |

What is natural hedging and how does it work

At its core, natural hedging is an approach where a company structures its operations so that foreign currency revenues and costs offset each other, reducing net exposure without using a derivative contract. Think of a European manufacturer that sells goods priced in USD and sources raw materials also priced in USD. A weaker euro hurts revenue when converted back, but it equally reduces the real cost of those USD-denominated inputs. The exposures cancel, at least partially.

Research shows that operational and financial structural changes form the core mechanisms of natural hedging. These include foreign direct investments, issuing foreign currency debt, and attracting investors from the target currency region. Each of these creates a structural counterweight to currency exposure rather than a contract-based hedge.

Practical examples of natural hedging in global business include:

- Currency matching: A US-based exporter receiving euros opens a euro-denominated account and pays euro-invoiced suppliers from that account, reducing repatriation risk.

- Localized production: A company builds a manufacturing facility in its primary export market, incurring local labor and supply costs that naturally offset local revenue.

- Foreign currency debt: Borrowing in the same currency as overseas revenue creates a natural liability that offsets the asset exposure.

- Negatively correlated assets: Pairing investments in assets whose values move inversely to currency risk, so losses in one position are dampened by gains in another.

What distinguishes this from financial hedging strategies is that natural hedging is embedded in how the business operates. It does not require a contract with a bank or a premium payment. The protection is structural and ongoing.

Pro Tip: Map your foreign currency cash flows by currency pair before designing any hedging strategy. You cannot find a natural hedge you have not identified first.

Benefits and limitations of natural hedging strategies

The benefits of natural hedging are real and well-documented. A 2024 longitudinal study confirms that natural hedging continuously reduces cash flow volatility and positively impacts firm value over time, well beyond initial implementation. For multinationals operating across multiple currency zones, that sustained stability matters significantly.

The core advantages are worth spelling out clearly:

- Cost efficiency: Natural hedging reduces the need for derivatives and complex financial instruments, lowering transaction costs and counterparty risk.

- Persistent protection: Unlike a forward contract that expires, a well-designed natural hedge works as long as the operational structure is maintained.

- Balance sheet resilience: Structural offsets contribute to more predictable cash flows, which improves planning accuracy and investor confidence.

- Reduced dependency on markets: Natural hedges do not require liquid derivative markets in every currency pair, which matters in emerging markets where instruments are scarce or expensive.

That said, the limitations are equally important to understand. Natural hedging rarely achieves a perfect offset. Timing mismatches between inflows and outflows, differences in contract size, and shifts in business volume all leave residual exposure.

The airline industry illustrates this complexity well. Proxy hedges like Brent crude futures do not always protect fully against jet fuel price volatility, and the effectiveness varies considerably between US, European, and Asian carriers due to liquidity differences and commodity price correlations. A similar challenge applies to currency natural hedges when trade volumes shift seasonally or geographically.

Pro Tip: Do not assume that a natural hedge built around last year's revenue mix still works this year. Revalidate the offset structure every quarter, especially if you have entered new markets.

The risk management for international companies literature consistently warns that over-reliance on natural hedging without monitoring leaves firms exposed to basis risk. The hedge exists in theory but drifts from reality over time.

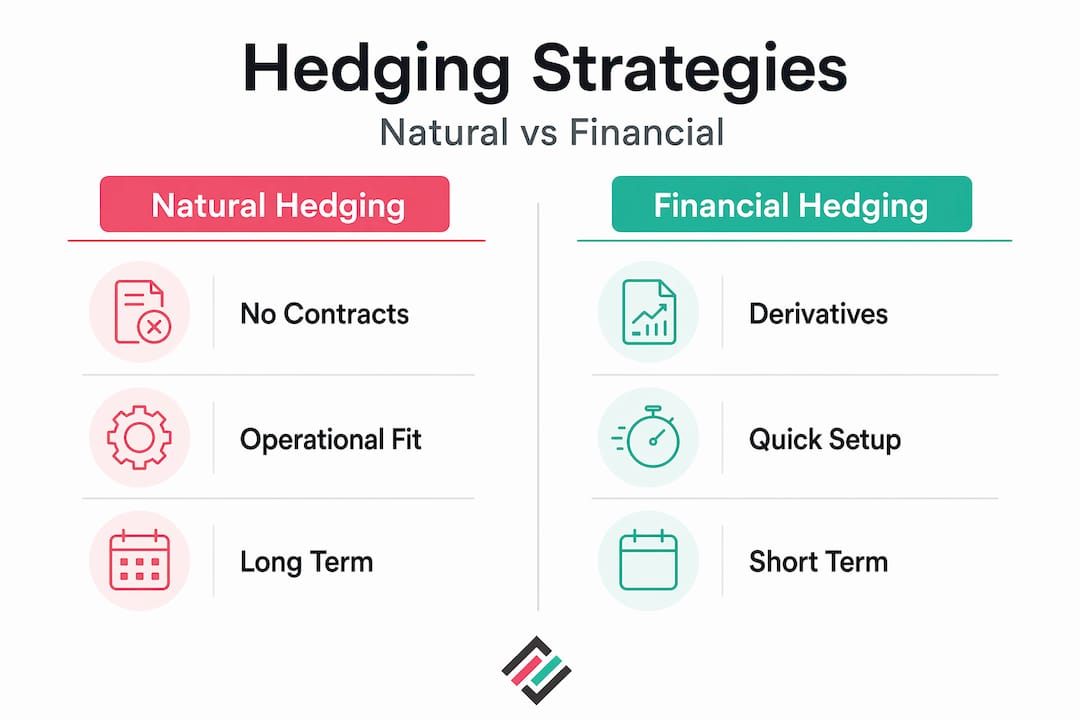

Natural hedging vs financial hedging: when to use each

Understanding natural hedging vs financial hedging requires clarity on what each approach actually delivers. Financial hedging uses instruments such as currency forwards, options, and swaps to lock in exchange rates or cap downside risk on specific transactions. Natural hedging, by contrast, does not involve a contract. It restructures exposure at source.

The table below captures the core differences:

| Feature | Natural hedging | Financial hedging |

|---|---|---|

| Mechanism | Operational and structural alignment | Derivative contracts |

| Cost | Minimal ongoing cost | Premiums, spreads, and counterparty fees |

| Flexibility | Low to moderate | High (can be sized precisely) |

| Duration | Ongoing while structure holds | Contract-specific |

| Precision | Approximate offset | Can be near-exact |

| Residual risk | Often present | Depends on instrument and design |

| Market dependency | Low | Requires liquid derivative markets |

Research confirms that natural hedging acts as substitute or complement to financial hedging depending on the flexibility and number of underlying transactions. When natural hedges are inflexible and structurally locked in, they tend to substitute for derivatives. When they require complex adjustments, they work best alongside financial instruments.

Case studies from major multinationals confirm that combining financial derivatives with natural hedges produces more effective currency risk mitigation than relying solely on one approach. The practical implication is clear: natural hedging should be your first line of structural defense, with financial instruments layered on top to manage residual and transactional exposure. Corphedge's value at risk hedging tools are designed specifically to quantify what remains after natural hedges are in place, so financial instruments can be sized accurately rather than speculatively.

Emerging applications: natural capital as a hedging tool

Natural hedging is expanding beyond currency and commodity risk. Institutions are increasingly looking at how nature-related assets can serve as hedges against a completely different type of financial risk: carbon price volatility.

Natural capital investments such as forestry and peatland restoration are being used to hedge against regulatory carbon pricing shifts. As carbon markets mature and mandatory pricing regimes expand across Europe and beyond, the value of verified carbon sinks in a portfolio correlates inversely with carbon cost exposure in operations. The logic mirrors currency natural hedging. You are matching an exposure with an asset that moves in the opposite direction.

For financial professionals managing portfolios in the EU, Poland, and Sweden, where carbon regulations and ESG reporting requirements are tightening, this trend carries direct relevance:

- Forestry assets generate measurable carbon credits that offset future compliance costs.

- Peatland restoration aligns with biodiversity regulation and provides verifiable natural capital values.

- These assets can be included in consolidated risk frameworks alongside currency and commodity exposures.

The broader implication is that "natural hedging" is no longer just an operational finance concept. It is becoming a strategic lens for managing regulatory, environmental, and financial risks simultaneously. Finance teams that recognize this early will be better positioned as ESG-linked risk frameworks become standard reporting requirements.

Implementing natural hedging strategies in practice

Designing and maintaining effective natural hedges requires a structured approach. Here is a practical framework that works for multinational companies across industries:

-

Identify and map all currency exposures. Break down revenues, costs, debt, and investments by currency. Segment by business unit and geography so the picture is granular, not aggregate.

-

Quantify existing natural offsets. Calculate the degree to which current operations already naturally offset currency exposure. Many firms discover they have more natural hedging in place than they realized, or that it is poorly distributed across currency pairs.

-

Assess the structural options. Evaluate whether operational changes such as local sourcing, invoicing currency adjustments, or facility location can improve the natural offset without sacrificing business efficiency.

-

Design the residual hedge. Once natural hedges are optimized, quantify the remaining exposure using a risk measure such as value at risk. This residual position is what financial instruments should cover.

-

Integrate and monitor continuously. Natural hedges shift as business volumes, product mixes, and supply chains change. Build a monitoring cadence so the hedge remains aligned with actual exposure. Corphedge's FX exposure management tools give real-time visibility into currency positions, which is exactly what this step requires.

-

Review annually at minimum. Currency correlations, market structure, and business strategy all evolve. An annual review ensures the hedging architecture remains relevant.

Pro Tip: When entering new markets such as Poland or Sweden, build the natural hedge analysis into the market entry model itself. Currency risk is far cheaper to manage structurally at entry than to retrofit with derivatives after operations are established.

Effective forex risk management for CFOs consistently points to the combination of rigorous exposure mapping and operational design as the foundation of durable hedging programs. The tools come after the structure, not before.

My perspective on natural hedging's strategic value

I have spent years watching finance teams treat natural hedging as a secondary consideration, something to acknowledge in a risk policy and then ignore in favor of derivative contracts. That instinct is understandable but costly.

In my experience, the most effective hedging programs I have seen are those where the CFO and the chief operations officer are genuinely aligned on currency risk. The natural hedge is an operational decision dressed in finance language. When manufacturing footprint, supplier selection, and invoicing currency are all designed with currency exposure in mind, the derivatives overlay becomes smaller, cheaper, and easier to manage.

The trap I see most often is treating natural hedges as static. A company localizes production in a market, declares the hedge in place, and moves on. Three years later, the local cost structure has changed, or revenue from that market has grown disproportionately, and the offset no longer holds. The hedge exists on paper. The exposure is real.

What I find genuinely exciting right now is the expansion of natural hedging logic into environmental risk. Institutions that are building carbon credit portfolios as a hedge against future carbon pricing are applying the same structural thinking that has always underpinned operational currency hedging. The concept scales. It just requires finance teams willing to think beyond traditional instrument categories.

My advice: treat natural and financial hedging as a single integrated system. Design the structure first, then size the instruments to fill the gaps. That sequence changes everything.

— Bartas

How Corphedge supports your hedging strategy

Natural hedging is your structural foundation. But even the best-designed operational hedge leaves residual exposure, and that is where technology makes the difference.

Corphedge is built for exactly this moment in your risk management process. The platform gives finance teams real-time visibility into FX positions, so you can see precisely what your natural hedges are covering and what they are not. The value at risk hedging module lets you size financial instruments against actual residual risk rather than guessing. For companies expanding into markets like Poland and Sweden, where currency volatility and regulatory requirements are both evolving, Corphedge provides the exposure monitoring and strategy execution tools needed to stay ahead. Explore the full platform capabilities and see how it complements the natural hedging strategies you already have in place.

FAQ

What is natural hedging in simple terms?

Natural hedging is when a company structures its operations so that foreign currency revenues and costs offset each other, reducing net currency exposure without using financial derivatives.

How does natural hedging work in practice?

It works by aligning cash flows in the same currency. For example, a company that earns USD revenue and also pays USD-denominated supplier invoices has a natural hedge because gains and losses from exchange rate moves partially cancel each other.

What are the main benefits of natural hedging?

The main benefits include lower transaction costs compared to financial derivatives, more stable cash flows over time, and reduced dependency on liquid derivative markets, particularly in emerging currency pairs.

Is natural hedging effective on its own?

Natural hedging is effective but rarely complete. Research confirms it continuously reduces cash flow volatility, but most companies need to complement it with financial instruments to cover residual and transactional exposures.

What is the difference between natural and financial hedging?

Natural hedging uses operational and structural changes to reduce currency exposure, while financial hedging uses contracts like forwards, options, and swaps. Combining both approaches typically produces the most effective risk mitigation for multinational firms.